Laptop Magazine just made T-Mobile one of their “Game Changers” for 2013 for its Un-Carrier campaign. I spoke with the author of the piece on T-Mobile and emphasized some of what I perceive as the risks around the campaign, but many of my thoughts didn’t make it into the piece, so I thought I’d share them here.

The concerns I have with T-Mobile’s Un-Carrier strategy are two-fold:

- Though there are one or two truly disruptive things in T-Mobile’s new approach, much of what they’re doing boils down to discounting

- Though some of their early moves took advantage of the flexibility in accounting afforded to owners of networks, the more recent ones are taking real risks with inflexible third-party costs.

I’ll take each of these in turn.

T-Mobile is essentially starting a price war

Let’s review the various phases of T-Mobile’s Un-Carrier strategy so far:

- Phase 1:

- Removing 2-year contracts, device subsidies

- Phase 2:

- JUMP! – the ability to upgrade more frequently than every two years

- Family plans with no credit check

- Phase 3:

- Free roaming overseas

- Free calls to overseas locations.

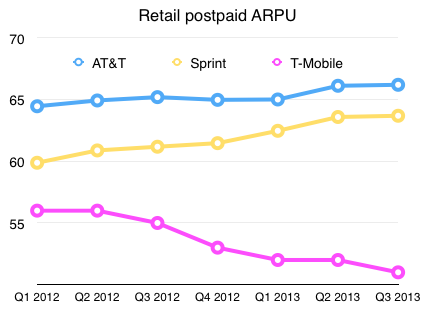

I’ve over-simplified a little but that’s the gist of each of the phases. Now, let’s look at each of those in turn. First, removing 2-year contracts and shifting to financing devices. The 2-year contract thing is a bit of a red herring – the vast majority of T-Mobile customers are still getting their device through T-Mobile, and so they’re getting locked into a contract of sorts to pay off the phone in installments, if nothing else. But the key point is that, by removing the device subsidy from the cost of the service plan itself, the price goes down significantly. Of course, you then have to add the cost of the device back in again, at say $20 per month for the iPhone. But the headline is that the price of service has fallen significantly. This is a continuation of a longer-running trend at ARPU to separate device and service costs, and is reflected in its falling postpaid ARPU:

For comparison’s sake, I’ve included two other major carriers’ equivalent ARPU figures, which can be seen to be rising rather than falling over time, as data ARPU rises slightly faster than voice ARPU is falling (Verizon no longer reports a comparable figure). The point here isn’t necessarily that T-Mobile’s falling ARPU is bad, but that it’s a reflection of the falling headline price of service, which itself is a symptom of price-based competition.

Secondly, let’s look at phase 2, which incorporated both JUMP! and family plans for those with sub-prime credit. JUMP itself isn’t technically price competition, though again the headline is that you get to do something you couldn’t do before without paying a lot of money. It’s also something of a niche appeal. The family plans for those with sub-prime credit were a total price play, on the other hand. Four lines for $100 undercuts not only T-Mobile’s own standard pricing but all other carriers’ pricing too. It may well be another factor contributing to that falling ARPU shown above.

Phase 3 was the launch of free international data roaming, free calls overseas to landlines, and cheap voice roaming charges. All three elements here are about price. Roaming and calling overseas costs a lot on other carriers, and now it doesn’t anymore on T-Mobile.

In summary, almost every element of what T-Mobile has done under its Un-Carrier strategy is a price discount of some kind. What’s so smart about all this is the way that T-Mobile has dressed up competition on price as something very different – a fundamental shift in the way it will provide services to consumers. And I think that’s because it recognizes that price wars are generally a bad idea, especially if you have competitors with much deeper pockets, and that competing on price tends to get you the worst rather than the best customers. However, that is ultimately what T-Mobile is doing here, and I believe that as it starts running out of truly disruptive things to do (I’d argue that it’s getting to that point already) it will be more and more clear that it’s purely competing on price, and long-term that’s bad for T-Mobile and bad for the rest of the industry too.

T-Mobile’s latest moves are even riskier than its first

The other major worry I have about T-Mobile’s Un-Carrier strategy is that its most recent moves are very different from its earlier ones. It’s first big announcements all involved areas in which T-Mobile itself determines the costs from an accounting perspective. And the great thing about running a network business is that it’s a massive fixed cost business with almost zero marginal cost. As such, an operator’s accounting department has great latitude in determining how to allocate large fixed costs between subscribers, between product lines and so on. This means that T-Mobile can afford to allocate lower costs to the items that it’s now charging less for, and still show a profit on them.

The difference with phase 3 is that all the costs at issue here are real, marginal third-party costs. I.e. the prices T-Mobile charges for international calling and roaming have to cover real, cash costs charged by overseas operators for the wholesale services (roaming and termination) which enable the service T-Mobile provides its customers. This is a very different proposition from deciding to charge a lower price for something whose cost is largely arbitrary, because charging zero for something means you lose money on every transaction. Every time a customer uses data overseas, or makes a call to a foreign country, and T-Mobile charges nothing for it, it goes deeper into the red.

This isn’t a unique problem, either – it’s the challenge with every all-you-can-eat buffet, but it’s also a problem with a long history in technology. When I was covering consumer Internet services and regulation in the early 2000s in Europe, a big issue for AOL and other providers was that they were offering flat-rate dial-up to their consumers, but paying a per-minute fee for termination to their wholesale suppliers. Anytime this situation arises, you have the same issue: you have to be very good at predicting how much your customers are going to use the service so that you can figure out what you can afford to charge them. Underestimate likely usage and you end up underwater very quickly. And of course, you can’t simply go by historical usage, because as soon as you go flat-rate or free, usage from your existing customers goes up and the heaviest users of your competitors’ services switch to your services.

In T-Mobile’s case, the problem is even more acute because it’s charging precisely zero for several of these services, specifically data roaming and calls to overseas landlines. So no matter how much customers use those, every minute is costing T-Mobile money and it’s getting no direct revenue in return. So it has to be cross-subsidized from other services. This then creates a tension between a customers’ incentives (“use this free stuff as much as I can”) and T-Mobile’s (“hope customers don’t use too much of this free stuff”). This is the opposite of Jeff Bezos’s famous strategy of trying to align customers’ incentives with Amazon’s, and that’s never a good idea.

It’s hard to be an Un-Carrier when your cost structure is a carrier’s

Ultimately, the big problem with all of T-Mobile’s moves is that they’re supposed to break the mold of what carriers do, but all the while T-Mobile is very much a carrier, with a carrier’s cost structure and business model. While you don’t have to emulate every aspect of what T-Mobile’s competitors do to be successful in this business, much of how carriers operate is driven directly by what it takes to make money when you run a network. You have to charge far more than the marginal cost of service to cover huge fixed costs, you charge more for the less price-sensitive services (such as roaming and international calling) so you can lower the prices on more price-sensitive ones, and you find ways to reduce complexity for consumers by bundling device costs partly into service costs.

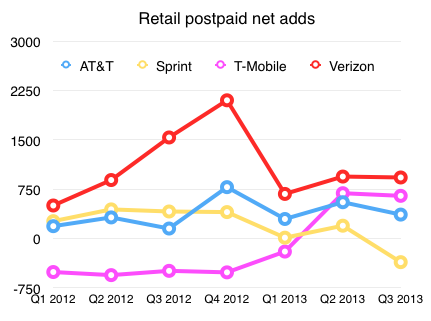

T-Mobile desperately needs to do something to turn its performance around, and the Un-Carrier strategy seems to be working so far – postpaid net adds rose dramatically into positive territory in Q2 2013 (though partly because of the launch of the iPhone on the network) and stayed almost as high in Q3, probably largely because of its Un-Carrier moves:

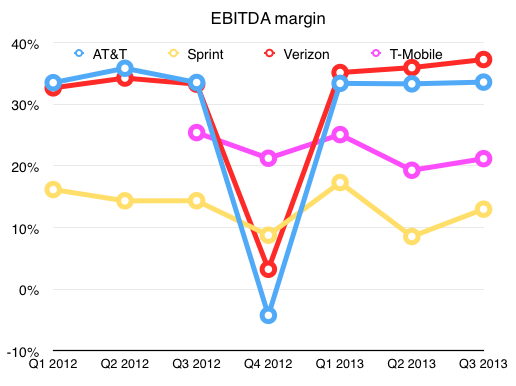

However, in order to maintain this sort of momentum, T-Mobile is going to have to keep up the sort of disruptive stuff it’s been doing, and that will mean further cutting prices, which in turn will negatively impact margins, which are already substantially lower than AT&T’s or Verizon’s (note that both AT&T and Verizon had special charges in Q4 2012 which temporarily dipped margins):

How long can T-Mobile afford to play this game for? And how long can it even keep up doing disruptive things? Even if we’re to take John Legere at his word that he’s working his way through a list of major pain-points for customers, how many items are left on that list? And how many of those can T-Mobile afford to address? In the meantime, it’s risking getting itself into a price war, and simultaneously taking on a lot of risk by charging nothing for services that incur real third-party costs. It’s great for consumers in the short term, but I’m just not convinced it’s sustainable.

Pingback: Why Sprint – T-Mobile makes sense | Beyond Devices()