Earlier this week, BlackBerry’s CEO John Chen posted a letter to customers. While he provided some sense of his strategy going forward, he unfortunately continues the tradition started by his predecessors of failing to answer the most compelling questions customers (and investors) have:

Is there any reason to believe the atrocious trend in device sales will turn around? If so, what?

Device shipments have now dropped 75% from their peak in 2011, and although it’s possible we’ll see a small blip next quarter from steep discounts on the Z10, the trend is likely to continue downward. Chen needs to explain what, if anything, will cause these same poorly-selling devices to start selling better, or allow any future devices to be more appealing to users. As of right now, there’s no evidence of either of those things, and as such we have to assume shipments will continue dropping, and with them what has historically been the largest chunk of overall revenues.

In the absence of that, is there any reason to believe service revenues won’t follow suit very soon?

Service revenues make up most of the rest of BlackBerry’s overall revenues, which is why some people seem to think it’s the most promising avenue for BlackBerry going forward. But the reality is that these service revenues are directly tied to the installed base of BlackBerry devices, each one of which generates a few dollars every month for the company. But, if device shipments go down dramatically and existing BlackBerry users churn to other platforms, this service revenue will merely lag falling hardware revenues by a few quarters but generally follow the same path. BlackBerry has already stopped reporting subscriber numbers, which started falling late last year, and had dropped from 80 million to 72 million by the time BlackBerry closed the door on that metric.

What, if anything, will fill the enormous gap in revenues left by the two major revenue streams dropping precipitously?

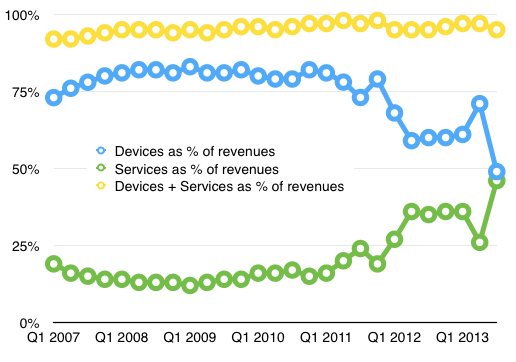

BlackBerry has historically generated between 92% and 98% of its revenues from these two revenue sources – hardware (devices) and services – see below:  As such, if they’re both going to start shrinking dramatically, what on earth can BlackBerry do to make up the difference? For starters, it will have to cut costs dramatically. The last time device shipments and revenues were at current levels (way back in 2007) cost of sales and overall operating expenses were a fraction of what they are now. Even cutting operating expenses by 50% by 2015 won’t be enough at this rate. The company has to find other sources of revenue, and it simply hasn’t shown what those are.

As such, if they’re both going to start shrinking dramatically, what on earth can BlackBerry do to make up the difference? For starters, it will have to cut costs dramatically. The last time device shipments and revenues were at current levels (way back in 2007) cost of sales and overall operating expenses were a fraction of what they are now. Even cutting operating expenses by 50% by 2015 won’t be enough at this rate. The company has to find other sources of revenue, and it simply hasn’t shown what those are.

How much revenue does BlackBerry expect to generate from its new revenue streams – MDM, BBM and M2M – and how?

The only new revenue opportunities the company has identified all have neat little three-letter abbreviations: mobile device management (MDM), BlackBerry Messenger (BBM) and Machine to Machine (M2M). But none is a big money spinner for BlackBerry today, nor will any of them generate significant revenue anytime in the next couple of years, at least in the context of historic hardware and service revenues.

The MDM licensing opportunity is worth $1.6 billion globally in 2014

MDM licensing will be around a billion dollar opportunity globally for all players this year – Gartner estimates it was worth $784 million in 2012 and will generate $1.6 billion in revenue next year. That’s not to be sniffed at, but in every quarter since 2008, bar the most recent, BlackBerry generated more than that every quarter in device revenues. And of course even if it gets off to a very good start in cross-platform device management, it can only hope to capture a fraction of the total opportunity. If device revenues are going away (as I believe they will), then it’s logical for BlackBerry to latch onto MDM, but neither it nor its customers or investors should kid themselves that it will in any way make up for the shortfall in device and service revenues. Even targeting the broader enterprise mobility space won’t provide anything like the sort of revenue opportunity BlackBerry has had in devices. BlackBerry’s new management needs to communicate just what it expects to generate in revenue from this segment, and start breaking it out in its financial reporting.

BBM generates no revenue today at all

BBM generates no revenue today, since none of the BBM products cost anything. BlackBerry has hinted that its new Channels feature and other business-oriented functionality will eventually be the source of this revenue, but it has given no sense of when it will start charging or how much revenue it expects to generate from this product. In addition, it has hinted at a social network of sorts, which is a crowded and ultra-competitive market if there ever was one, with major players such as Facebook, Twitter, LinkedIn, Microsoft and Salesforce already entrenched. LinkedIn, arguably the most successful player in the niche BlackBerry is likely to target, generates $400 million a quarter after ten years in business, which suggests the modest level of revenue BlackBerry might achieve in a few years if it’s successful from these products

M2M is a promising area overall but BlackBerry’s addressable market is tiny

M2M is like MDM in that it is growing rapidly but BlackBerry’s addressable market is tiny. The biggest opportunities in M2M are in connectivity (provided by carriers) and solutions (consulting and so on, provided by a range of players including carriers, systems integrators and specialists). The part BlackBerry will participate in – providing the OS for embedded devices in the form of QNX – is tiny in the grand scheme of things. QNX had revenue of $30-40 million per year before its acquisition by BlackBerry, and it’s unlikely that it’s more than doubled by now, meaning that it’s probably under $100 million annually today. Again, that will likely grow, but it’s not going to make a dent in the overall number for some time to come.

BlackBerry’s challenge: cut costs enough to survive at a much smaller size

The only way BlackBerry can survive, therefore, is if it can dramatically cut costs to give it enough breathing room to allow these very small, nascent product lines to generate significant revenue. I believe that’s why Fairfax wanted to take it private – that’s an ugly kind of transition that you really don’t want to be doing in public. It involves heavy losses and burning cash while you undergo the transition. Chen’s challenge will be running a public company while doing it, which won’t be fun. But as the CEO and chairman of a public company, Chen has a duty to his shareholders and customers to articulate that plan (if that’s indeed what it is) so that they can tell whether it’s working. That means specifying targets for each of these new product lines and reporting progress each quarter. BlackBerry reports earnings on the 20th of this month – I’m hoping we’ll hear more from Chen about how he plans to undergo this transition.

Pingback: BlackBerry may have to shrink its way to success - TRAIKA()

Pingback: Best Smart Phone Finds » BlackBerry may have to shrink its way to success » Page: 1 | Best Smart Phone Finds()

Pingback: BlackBerry may have to shrink its way to success | Tech Info..()

Pingback: BlackBerry may have to shrink its way to success | GforGooGLe()