This past week has seen two major news items featuring Verizon: the defeat of the FCC’s net neutrality regulations in court, which was instigated by Verizon, and the acquisition by Verizon of Intel’s Cloud TV business. So far, I haven’t seen many articles drawing a connection between the two, but in reality they’re both part of the broader picture of Verizon’s video strategy.

FiOS has been the focal point of Verizon’s video strategy

That strategy was kicked off years ago, when Verizon launched its first video services over 3G and then over its FiOS networks. Over time, those two efforts were united to some extent as a more coherent video strategy emerged, and it eventually became clear that FiOS was the focal point of Verizon’s video strategy, with mobile efforts merely appendages to that. The FiOS video offering has since grown to five million subscribers, representing just over a third of the homes where it is available. This business generates several billion dollars a year in revenue for Verizon, alongside FiOS broadband and voice services, and represents Verizon’s main video business today.

However, Verizon appears to recognize that this opportunity may be under threat from trends in the market. A recent interview with the guy who heads Verizon’s consumer and small business wireline operations, Bob Mudge, hints that the company sees the writing on the wall for traditional pay-TV services from cable and satellite companies and telcos:

The pay-TV market is shrinking. It’s a slow shrinkage…

Data connectivity is what you must have. That gives the customer more options, whether to get traditional video or to use that data pipe for over-the-top (OTT) video and other online applications.

The key point here is that Mudge recognizes that many consumers will not want to buy classic pay-TV services, and that many of their needs may be met by other options. I think he’s wrong about broadband being the key service (though it’s understandable why he’d make that argument given Verizon’s strength in this area). Consumers fundamentally want content, not connectivity. Connectivity is a means to an end, and if it’s the right combination of fast and good value, they won’t care who they get it from. The TV offering is going to be the key differentiator in the consumer space, not broadband.

That doesn’t mean Verizon is chasing the wrong goal though. In fact, over time, the FiOS TV offering has evolved into a multi-screen product, with apps and online consumption of subsets of the content, in part as a response to this shift. But it’s also gone further than that, experimenting with ways to deliver video content to people who don’t have FiOS set-top boxes. First, it ported the FiOS TV platform to popular gaming consoles and other third-party boxes like Blu-Ray players and Roku (not all of which have been released publicly). This could be used as a set-top-box replacement in FiOS homes, but it’s also clear that it could be used to penetrate homes without FiOS. Secondly, it created its joint venture with Redbox, Redbox Instant, which is entirely independent of FiOS. I doubt it’s a big money spinner in its own right, but it’s given Verizon a valuable opportunity to experiment with pure-play online delivery models and technologies, which has expanded the addressable market beyond the 15 million or so homes where FiOS TV is available.

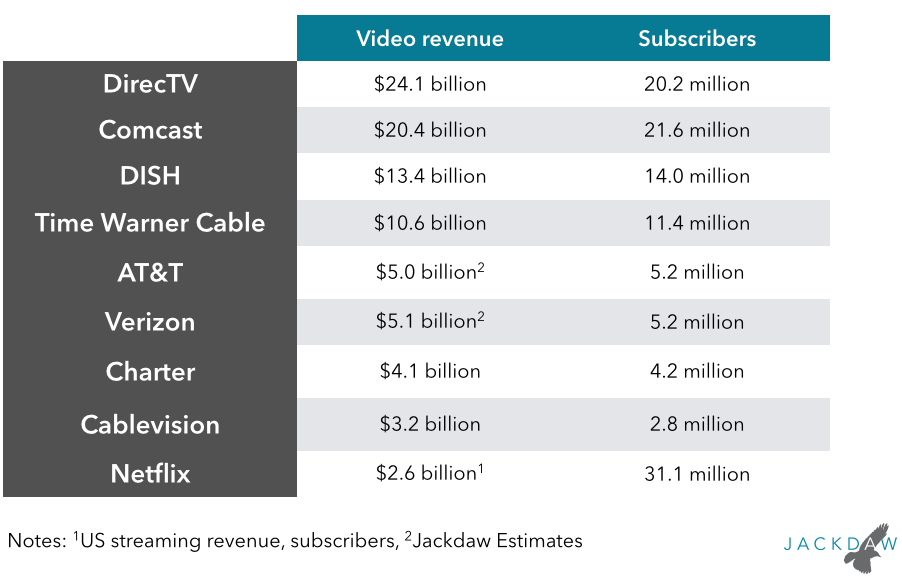

Expanding beyond Verizon’s traditional footprint is critical to growing that base of users beyond five million. Netflix, which launched streaming almost exactly seven years ago, now has more subscribers (31.1 million) in the US than any other video provider (Comcast is second with 21.6 million). It derives less than $100 per year from each subscriber, which pales in comparison with the $1000 or so that cable, satellite and telco providers generate, but Netflix already generates almost as much video revenue as Cablevision. That space is clearly growing – Hulu and Netflix alone generated almost $4 billion in revenue in the US in 2013, which is dwarfed by the $85 billion or so the major providers generated, but growing fast. (See the chart below, which is based on the twelve months to September 2013.)

Pursuing the wholesale video opportunity

However, Verizon has also been working on a completely different video revenue opportunity for a number of years, and that’s the wholesale content delivery market. It licensed technology from Velocix (subsequently acquired by Alcatel-Lucent) way back in 2009 and started providing services to third parties shortly afterwards, with HBO’s streaming service being an early example in 2010. This business has been built up much more quietly than the consumer-facing one, but it’s clearly an important strategic area for Verizon too. Verizon Digital Media Services (VDMS) is the name for this business, and it had made significant investments already by 2011.

In late 2013, this part of Verizon made two more acquisitions, of UpLynk and EdgeCast, which offer further evidence of its ambitions in this space. Both companies add critical functionality that Verizon would otherwise have had to rely on partners to deliver, and with these acquisitions it is able to boast of an end-to-end solution for ingesting, encoding, and delivering content across its network, which it showed off at CES recently.

All these activities so far have largely paralleled the activities of the major CDN providers such as Akamai and Limelight over the last several years. But there is one thing Verizon can do that the traditional CDN providers can’t: provide optimized delivery over the last mile of the network to Verizon’s nine million broadband customers. This seems like a natural extension of the services Verizon is already providing to its VDMS customers, and it would be unique in the industry. But it would have fallen foul of the FCC’s net neutrality regulations, which is why I think Verizon opposed them. I don’t think Verizon (or any of the other major US broadband providers) has any intention of blocking or degrading services, but I do think Verizon in particular would like to charge content providers for premium delivery, and the vacation of the net neutrality rules would allow them to do so. It’s important to note that, although Verizon has hinted at business models where it would charge content providers to reach consumers, it hasn’t fleshed those out, so this is speculation on my part.

Verizon’s three-part video strategy

As a result of all this, Verizon is today pursuing a three-part strategy for video services:

- Sell classic pay-TV services to as many of the 15 million households where FiOS is available as possible. It’s only sold about a third of those so far, and the number is creeping up pretty slowly, so though there’s growth left, it’s not going to be huge. Competition from cable and satellite remains fierce, so there’s incremental growth here at best. Verizon will continue to evolve the offering here to make more and more content available on more and more screens, but this will be largely a competitive differentiator rather than a source of significant revenue growth.

- Sell a range of wholesale content delivery and related services to third-party content providers like HBO. This is unbounded by the FiOS footprint or even Verizon’s overall broadband footprint, so it could grow significantly from where it is today, though it will always be a much smaller market than consumer video services.

- Sell over-the-top video services to consumers independently of the FiOS offering. This is exemplified by Redbox Instant today, but could well expand into something more. Verizon already has great relationships with all the major content providers through FiOS, and through broader licensing agreements could easily create a sort of unbundled FiOS TV offering to be sold nationwide.

All of this brings us back to the Intel Cloud TV acquisition, which could easily help with the third of these strategies, but will also be very helpful in making the core FiOS TV offering better. It’s all about accelerating the existing strategy for consumer video services, but that in turn is part of this broader strategy for video.

Pingback: snk.to/DOgj()