The next company in my series of “thoughts on earnings” pieces (see Google here, Apple here and Facebook here) is Microsoft. I’ll be doing something on Amazon next, most likely. Microsoft is a complicated business, with many parts to it, so I’ll focus mostly on the things I think most people overlook, because they’re rather buried in the earnings release or even the 10-Q. This involves making some estimates, calculations and assumptions, as well as interpolation, so please understand that many of the numbers are my best guesses rather than those reported by Microsoft (I try to be clear on which is which in each case).

Long story short: for all Microsoft’s talk about Mobile and Cloud, those two categories likely generate under 10% of Microsoft’s revenue today – something I’ll return to in the conclusion at the end of this post.

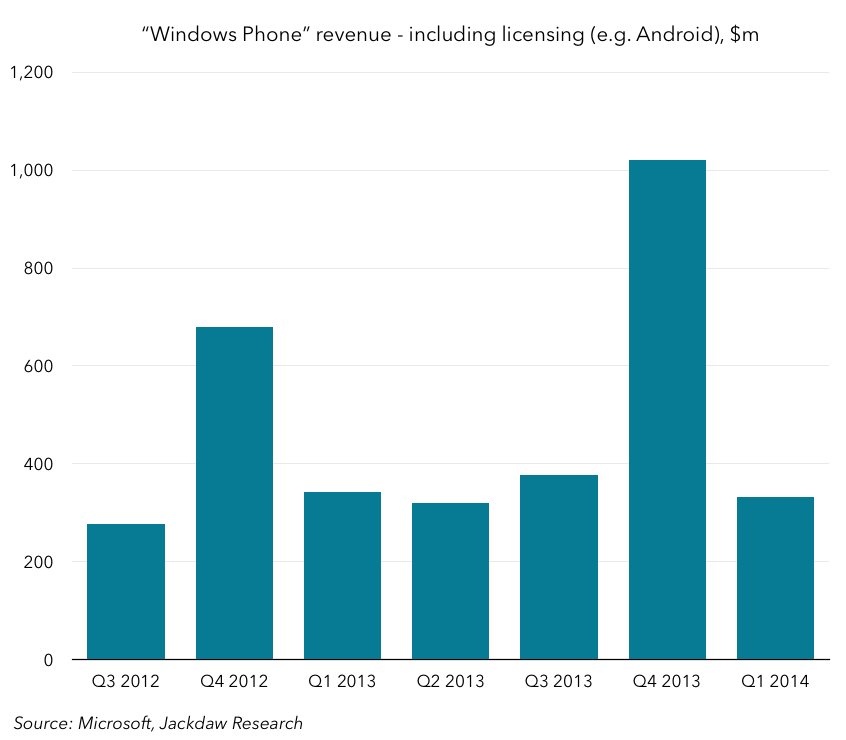

Windows Phone

First, Windows Phone. I’ve written at length before about the methodology used here, but we got another couple of quarters’ worth of solid data so I’m providing some quick numbers off the back of that.

The key thing to note here is that, other than in the fourth quarter, this number stays a little under $400 million a quarter. And it’s worth reminding everyone that this number is not just Windows Phone licensing itself but also the rest of Microsoft’s mobile licensing activity (think patents licensed to Android OEMs). As such, as Microsoft executes on its new policy of not charging OEMs for Windows for devices under 9 inches, there’s only a very small amount of revenue at risk – likely $100-200 million per quarter. And of course Nokia was paying about 90% of that anyway, so it would have become an internal transfer starting today.

The key thing to note here is that, other than in the fourth quarter, this number stays a little under $400 million a quarter. And it’s worth reminding everyone that this number is not just Windows Phone licensing itself but also the rest of Microsoft’s mobile licensing activity (think patents licensed to Android OEMs). As such, as Microsoft executes on its new policy of not charging OEMs for Windows for devices under 9 inches, there’s only a very small amount of revenue at risk – likely $100-200 million per quarter. And of course Nokia was paying about 90% of that anyway, so it would have become an internal transfer starting today.

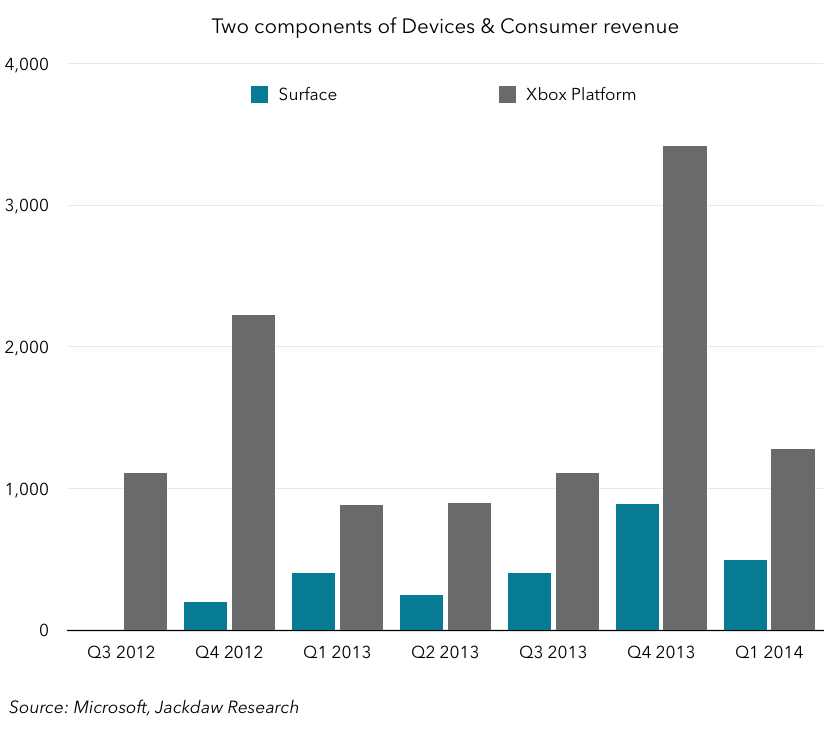

Consumer Hardware

This category is made up almost entirely of activities related to the Xbox and Surface. Luckily, Microsoft provides enough information to flesh out some of these numbers for two categories of revenue: Surface (which it has reported directly for the last four quarters) and “Xbox Platform” (i.e. a combination of Xbox sales and subscriptions). Here are my estimates for these two categories:

Xbox is extremely spiky around the fourth quarter, particularly last quarter when the Xbox One launched. But it’s so far always been above (and usually way above) revenues for the Surface. Surface revenue has also been all over the place, but it’s never crossed the billion-dollar mark yet, and actually fell significantly in Q1 from Q4 (interesting that the holiday quarter had such an impact on sales for a product that’s supposed to be productivity focused). So far, the Surface is a very small part of Microsoft’s revenues, and it therefore makes all the more sense for Microsoft to open up Office to the iPad.

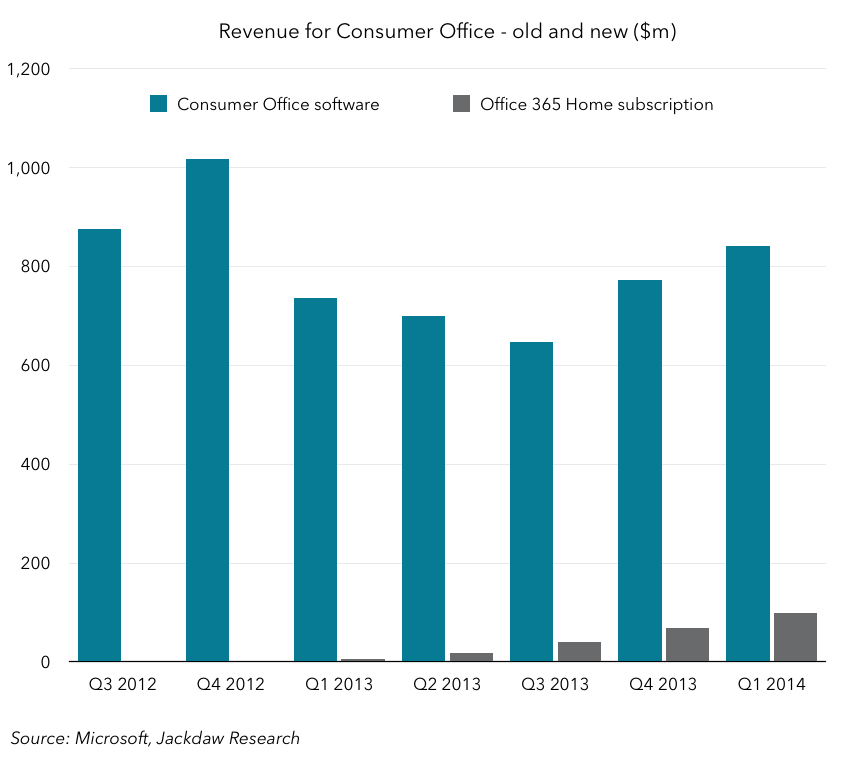

Consumer Office

Microsoft now has two flavors of Office – the classic software version, and the subscription version, Office 365. It again provides enough data on both of these that we can get a reasonably good picture of overall figures for both categories on the consumer side, as shown below:

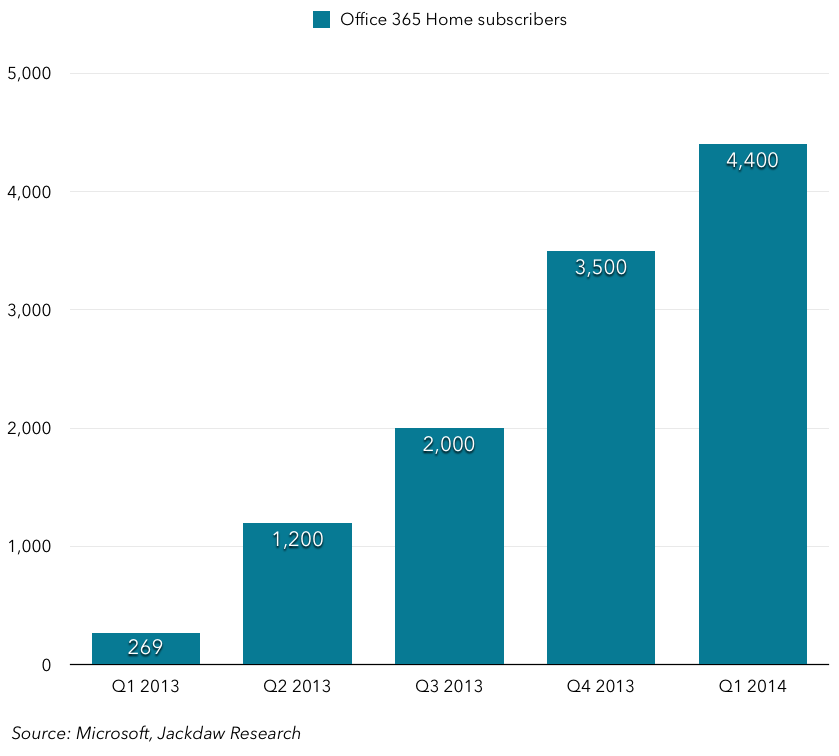

As you can see, the traditional form of Office far outsells the subscriptions. Even in this most recent quarter, Consumer Office 365 revenue was under $100 million, while traditional sales were around $850 million, so almost 10x 365 revenues. This model is undoubtedly the future, but it’s going to take a very long time for that future to become even relatively significant in Microsoft’s finances. Microsoft also directly reports the number of subscribers for Consumer Office 365 on a fairly regular basis, and they’re pretty small still:

Growth in the most recent quarter was actually slightly lower than in the previous two quarters, which is not a great sign. This coming quarter, though, we should start to see the impact (if any) of the launch of Office on the iPad. Though very popular free apps for viewing Office documents, they’ll only be really useful to Microsoft if they start to create pull-through for Office 365 subscriptions, which are offered as in-app purchases and separately. Though the apps registered in the top grossing list too, it doesn’t take many sales at $100 a pop to climb high on those charts. As such, the degree to which that 4.4m subs number goes up next quarter will be the best indicator for the success (or otherwise) of Office for iPad.

Online advertising

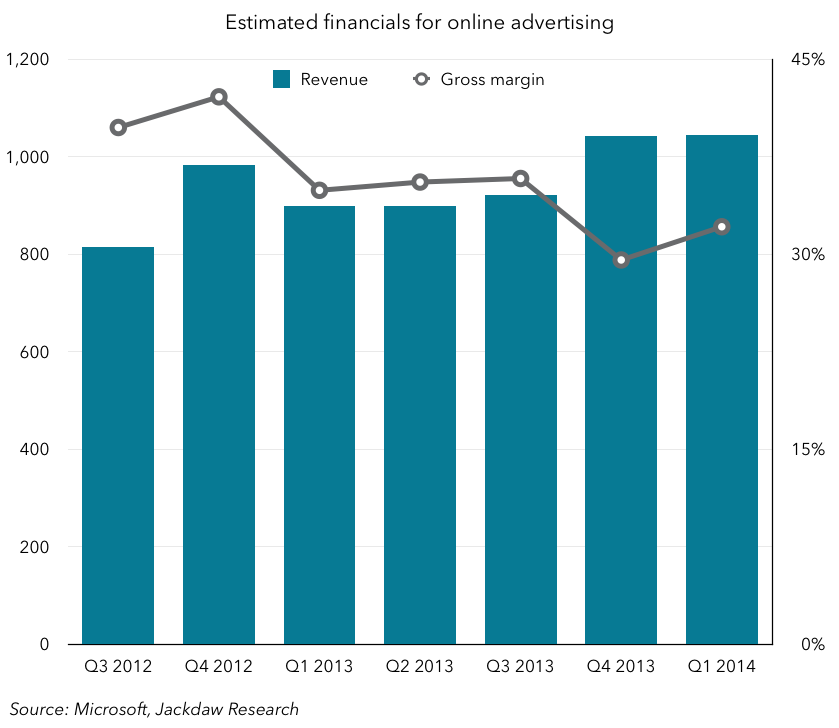

Bing is much-maligned and the frequent subject of calls for Microsoft to get out of the consumer business or at least ditch Bing. With the recent release of Cortana, I think there’s a more compelling argument than ever for Microsoft to hold onto Bing as a strategic asset (though I’ve long believed the Consumer and Enterprise businesses at Microsoft are essentially impossible to pry apart). But Bing still isn’t generating significant revenue for Microsoft, and online advertising continues to be a tiny part of its business. Here, too, Microsoft has been providing enough data points to be able to form a decent picture of revenues, and even the split between search and display advertising. But we can also put together a decent picture of gross margins for the online advertising segment. First, the overall numbers:

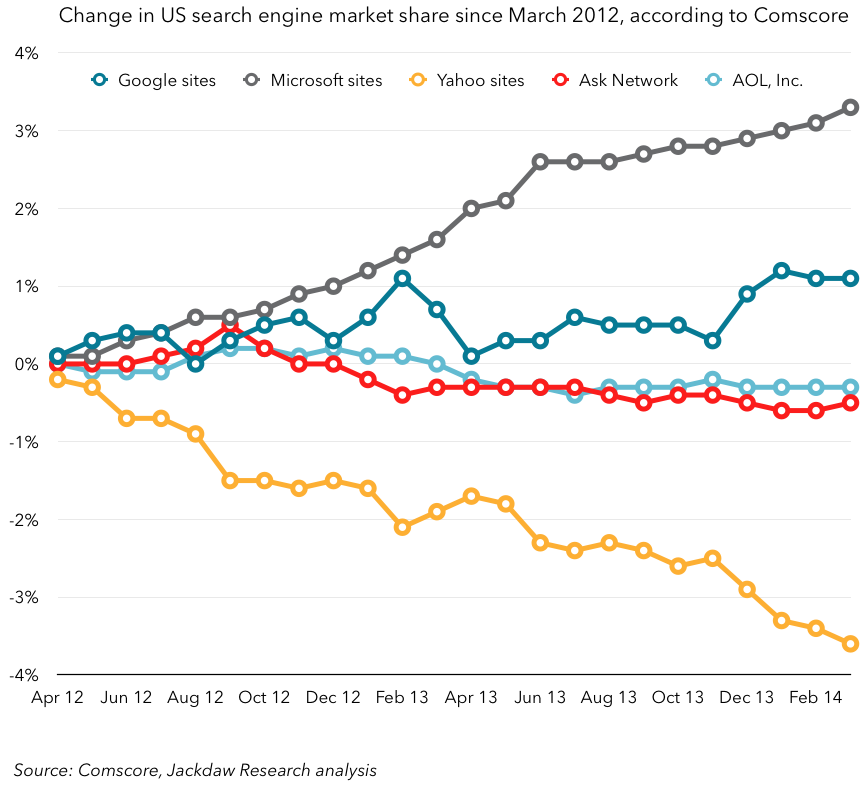

As you can see, online advertising has barely become a billion dollar a quarter business for Microsoft, and its gross margins are in the low 30s (and apparently falling). Compare that with Google’s advertising business, which generates $14 billion a quarter in revenue and gross margins in the high 50s. The major challenge is scale – this is a business that requires huge up-front and fixed costs to operate regardless of the usage, and as such the larger you are, the more profitable you can be. Microsoft trumpets its increasing share of the US market, but it’s still very small, at 18.6%, compared with Google’s 67.5%. Worst still, Microsoft really isn’t making inroads in Google’s share, but rather taking share from Yahoo, whose search results Microsoft is providing, as the chart below shows. As such, share is essentially moving from one pocket to another at Microsoft, while Google’s share has actually risen about 1% over the last two years. Those same Comscore figures show that the percentage of searches “powered by” Bing in the US has only risen from 25.9% to 27.1% over this two year period.

As you can see, online advertising has barely become a billion dollar a quarter business for Microsoft, and its gross margins are in the low 30s (and apparently falling). Compare that with Google’s advertising business, which generates $14 billion a quarter in revenue and gross margins in the high 50s. The major challenge is scale – this is a business that requires huge up-front and fixed costs to operate regardless of the usage, and as such the larger you are, the more profitable you can be. Microsoft trumpets its increasing share of the US market, but it’s still very small, at 18.6%, compared with Google’s 67.5%. Worst still, Microsoft really isn’t making inroads in Google’s share, but rather taking share from Yahoo, whose search results Microsoft is providing, as the chart below shows. As such, share is essentially moving from one pocket to another at Microsoft, while Google’s share has actually risen about 1% over the last two years. Those same Comscore figures show that the percentage of searches “powered by” Bing in the US has only risen from 25.9% to 27.1% over this two year period.

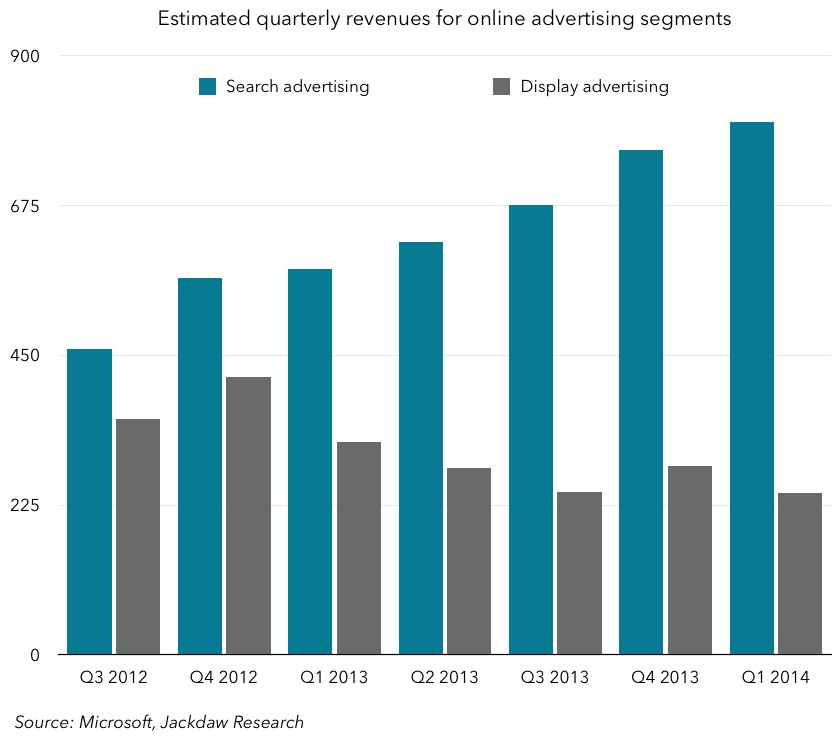

However, search advertising revenue is growing at Microsoft, and quite strongly, apparently driven by both higher revenue per search and by the growing number of searches, even as display advertising revenue falls as shown in this chart:

Given that the total number of searches in the US has stayed roughly constant over the past two years, this likely means Microsoft is growing mostly outside the US, which is both a sign that it’s extending beyond its traditional stronghold, but also that it will be more exposed to markets where ad spend is lower. Search and online advertising in general continues to be a huge challenge for Microsoft, but it is at least having some success in search, though it’s still massively sub-scale compared with Google.

Given that the total number of searches in the US has stayed roughly constant over the past two years, this likely means Microsoft is growing mostly outside the US, which is both a sign that it’s extending beyond its traditional stronghold, but also that it will be more exposed to markets where ad spend is lower. Search and online advertising in general continues to be a huge challenge for Microsoft, but it is at least having some success in search, though it’s still massively sub-scale compared with Google.

Commercial Other (services)

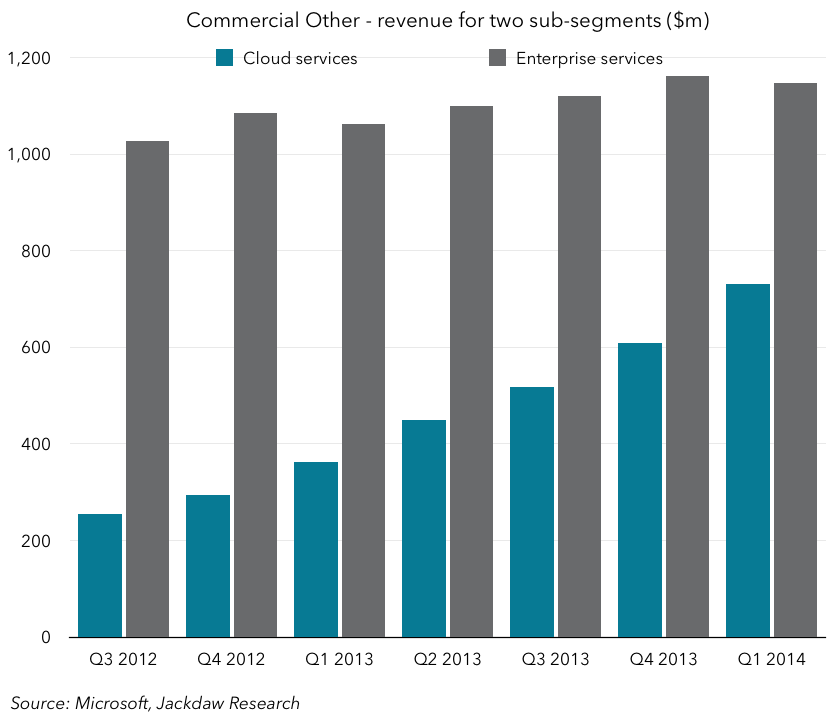

Lastly, I wanted to touch on a very different corner of Microsoft – the somewhat murky Commercial Other category, where all kinds of enterprise services lurk. Here, there are two categories where Microsoft provides enough data in its 10-Q to start to draw some conclusions about revenues – Enterprise Services and Cloud Services. From Microsoft’s description of its segments:

- “Enterprise Services [includes] Premier Support Services and Microsoft Consulting Services”

- “Cloud Services [comprises] Office 365, excluding Office 365 Home and Office 365 Personal (“Commercial Office 365”), other Microsoft Office online offerings, Dynamics CRM Online, and Microsoft Azure.”

Here’s a breakdown of those two major categories based on the available data:

Enterprise Services is now consistently over a billion dollars a quarter, and Cloud Services is ramping up much more quickly, with a run rate that should have it hitting a billion dollars a quarter before mid-2015. That’s an impressive run-rate, and important because this part of Microsoft’s business is central to its Nadella-inspired open platform approach. To the extent that cloud services are a big part of Microsoft’s future vision, the rapid growth of this category is really important.

Cloud and Mobile? Not yet

However, to the extent that Microsoft is to be a mobile-first, cloud-first company, its revenues are still very much rooted in the PC and in traditional software models. Windows and old-style Office revenue likely accounted for over 50% of revenues and over 90% of operating profits in the most recent quarter. Mobile meanwhile, accounted for about $300 million, while those Enterprise Cloud Services were just $700 million, and Office 365 likely accounted for well under a billion dollars as well. There’s a heck of a long way to go, and an enormous transformation still to take place, and there’s huge executional risk for Microsoft along the way.

Pingback: Microsoft Completes Nokia’s Acquisition: Expect A Significant Write-Off, Mitigated By A Tax Advantage | Virtual Fashion Technology()