Amazon’s earnings are sort of the opposite of Microsoft’s: whereas Microsoft’s earnings and especially its 10-Q are packed full of little nuggets and details that you can tease out, Amazon’s earnings are about as sparse as Google’s in terms of finding interesting details. But there’s still some interesting stuff, and I’ve done my best to tease out some of the more meaningful bits below. As a reminder, this is one of a series of posts about major tech companies’ Q1 earnings – you can see them all here.

Profits and growth

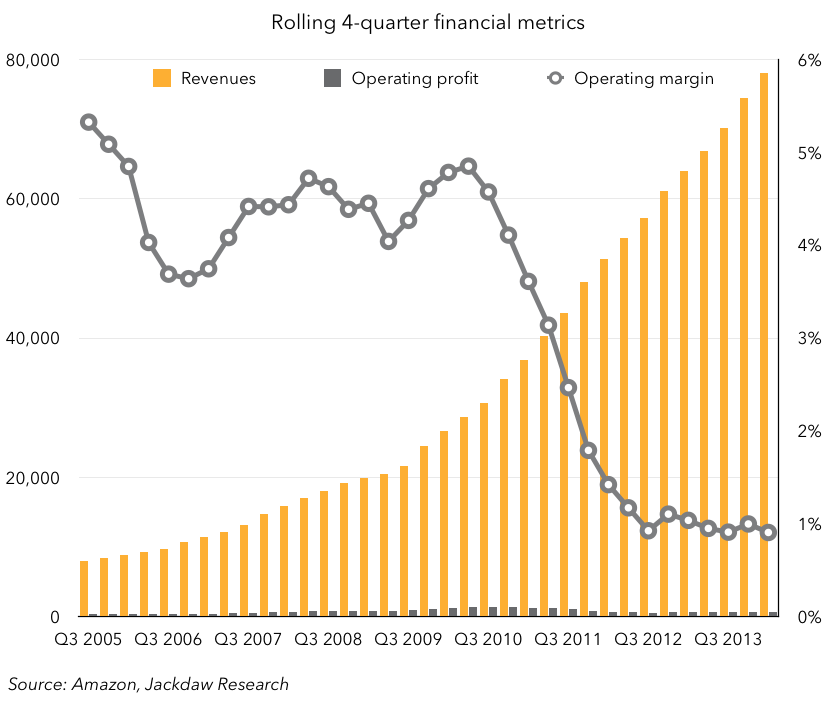

The first thing that strikes you when you look at Amazon’s results is how amazingly small its operating margins are compared to all the other leading tech companies. When you plot revenue and operating profit on the same chart, you almost can’t even see the operating profit bars because they’re so small. It wasn’t always quite this bad, though:  There was a time when Amazon regularly generated 4-6% operating margins (still low by the standards of its peers) but over the last couple of years it’s settled into a very consistent 1% operating margin over 4 quarters. On the other hand, look at that growth line – there’s no other company that grows so consistently and sharply at this scale in the tech industry. This chart perfectly captures Amazon’s current strategy: very high growth at 1% operating margins, with the low margins caused by massive investment in the infrastructure necessary to drive growth. It very much feels as though Amazon recognizes that there’s a limited window of opportunity for it to build the sort of scale and infrastructure necessary to dominate e-commerce before anyone else does, and it’s scraping by with minimal margins in order to capture as much as possible of that opportunity before it closes.

There was a time when Amazon regularly generated 4-6% operating margins (still low by the standards of its peers) but over the last couple of years it’s settled into a very consistent 1% operating margin over 4 quarters. On the other hand, look at that growth line – there’s no other company that grows so consistently and sharply at this scale in the tech industry. This chart perfectly captures Amazon’s current strategy: very high growth at 1% operating margins, with the low margins caused by massive investment in the infrastructure necessary to drive growth. It very much feels as though Amazon recognizes that there’s a limited window of opportunity for it to build the sort of scale and infrastructure necessary to dominate e-commerce before anyone else does, and it’s scraping by with minimal margins in order to capture as much as possible of that opportunity before it closes.

Geographic trends

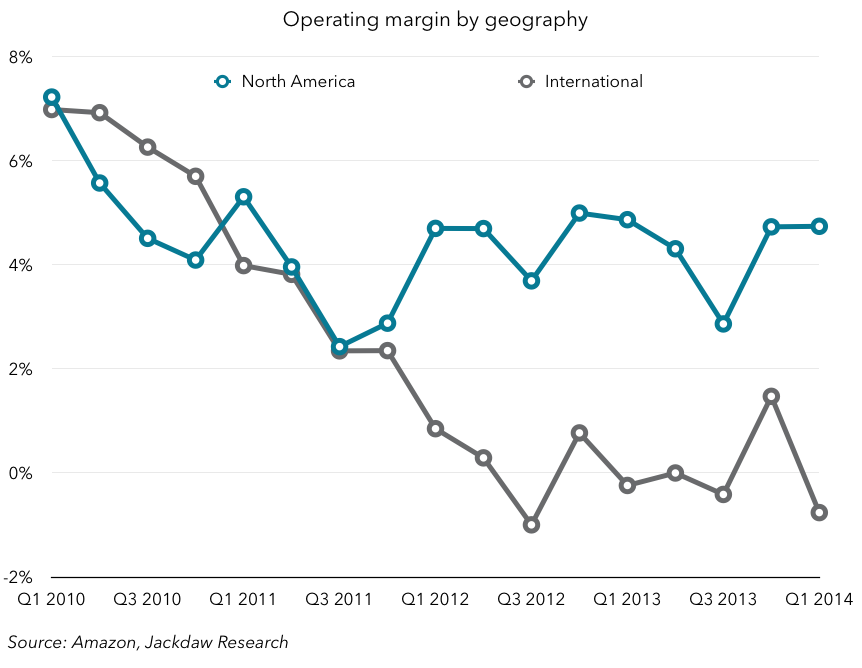

Amazon’s regional results bear this out, as there’s been a stark divergence between its domestic and overseas operations in terms of profitability:

Amazon’s North American operations are actually generating the same sort of margin the whole company used to generate, at between four and six percent most quarters. But the international operations have dived to essentially zero profits over the last couple of years as Amazon invests heavily in certain international markets. This is CFO Thomas Szkutak on the earnings call yesterday:

In terms of what you’re seeing in Q1, and you’ve been seeing this certainly for a few year period here is we’re investing very heavily in international and we’re doing that in a number of different ways. Certainly from a geographic standpoint, we continue to invest in new geographies, and Italy and Spain were certainly the most recent and you should assume that we’re investing in those geographies. We continue to invest in China and certainly that’s in investment mode.

And then also as we’ve continue to grow in international, we’ve invested in terms of capacity, both fulfillment capacity, as well as infrastructure capacity to support those. So what you saw – you will see some certainly variation over time in the period that you’re talking about. We certainly had particularly coming out of – going into late 2008 and also 2009, we had extra capacity globally. We still did continue to invest, but not near the rates that we’re investing now and that’s why you saw some results that you’ve seen. But again one of the things that you see now in international but in our total results is continue to invest very heavily into the business because of the opportunities that we are seeing.

Interestingly, though, despite all this investment, Amazon is still growing more slowly outside the US than in, in part because Amazon offers a wider range of products and services in the US. But the slower growth is remarkable because it has mean that Amazon exhibits the opposite of the usual trend with major US tech companies, which is that their international revenue quickly outweighs domestic revenue. Not so for Amazon, which flirted with almost equal revenues in North America and internationally for a long time before seeing a significant divergence between the two since 2010 when domestic growth began to accelerate but international growth grew less quickly:  The question of Amazon’s international growth is one I could spend a lot more time on, and I’ll be doing a post on it soon.

The question of Amazon’s international growth is one I could spend a lot more time on, and I’ll be doing a post on it soon.

Costs and Prime

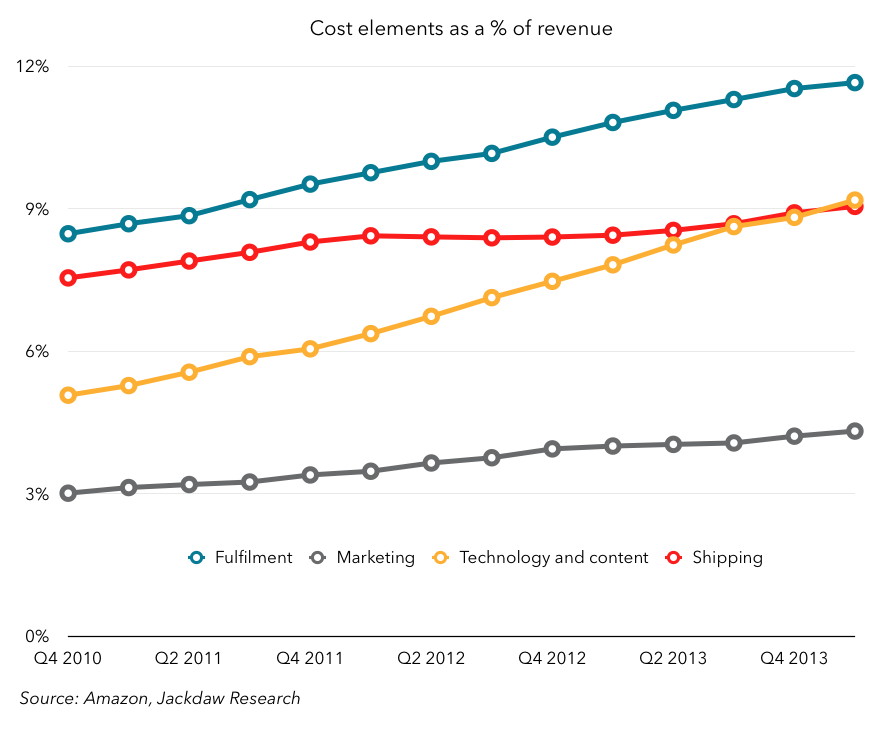

I’ve previously looked at shipping costs specifically at Amazon, because it’s one of those numbers that’s unique to Amazon, and because I wanted to back up the sense that Amazon’s justification for raising the price of Prime was misleading. I won’t re-hash all that here, but it is interesting to look at the various components of Amazon’s operating costs and how they’re increasing as a percentage of revenues (thus putting pressure on margins):

The chart above continues to bear out the message of my previous post on this, which is that (external) shipping costs actually aren’t rising that fast, but other costs are, notably content costs, which Amazon frustratingly bundles together with technology costs. But (internal) fulfillment costs are also rising at about the same rate, likely because of the heavy investment in new fulfillment center capacity, especially overseas.

The chart above continues to bear out the message of my previous post on this, which is that (external) shipping costs actually aren’t rising that fast, but other costs are, notably content costs, which Amazon frustratingly bundles together with technology costs. But (internal) fulfillment costs are also rising at about the same rate, likely because of the heavy investment in new fulfillment center capacity, especially overseas.

Third-party sellers

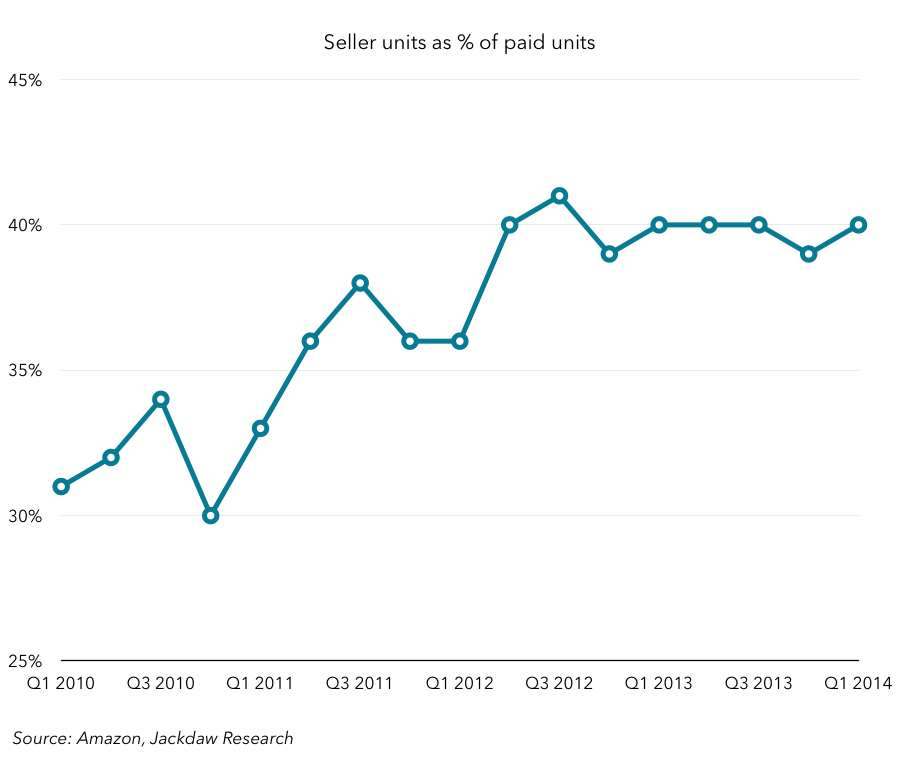

One number Amazon only provides on its earnings calls but not in any other materials is the percent of units sold which came from third-party sellers. The history of this number is shown below:

This number has both grown strongly and bounced around a lot in the past, but in the last several quarters it’s really stabilized and has stuck at either 39% or 40% for the last year. This is clearly an enormously important source of revenue for Amazon, and a major source of new items eligible for Prime over the last several years as well. Though we can’t know how much of Amazon’s revenues these third-party sellers are responsible for, it’s likely that it’s a large proportion. This is interesting in the context of Amazon’s business in China, for a couple of reasons. Firstly, it’s clear that Amazon sees third-party fulfillment as an important part of its business there too – again, from the earnings call:

This number has both grown strongly and bounced around a lot in the past, but in the last several quarters it’s really stabilized and has stuck at either 39% or 40% for the last year. This is clearly an enormously important source of revenue for Amazon, and a major source of new items eligible for Prime over the last several years as well. Though we can’t know how much of Amazon’s revenues these third-party sellers are responsible for, it’s likely that it’s a large proportion. This is interesting in the context of Amazon’s business in China, for a couple of reasons. Firstly, it’s clear that Amazon sees third-party fulfillment as an important part of its business there too – again, from the earnings call:

China is a big investment. In all of our geographies, not just international, we’re investing behalf of customers in terms of lowering prices. And so, that’s having an impact, volume is having an impact. We continue to invest in fulfillment capacity not only for our retail customers, but also for third-parties on behalf of fulfillment by Amazon.

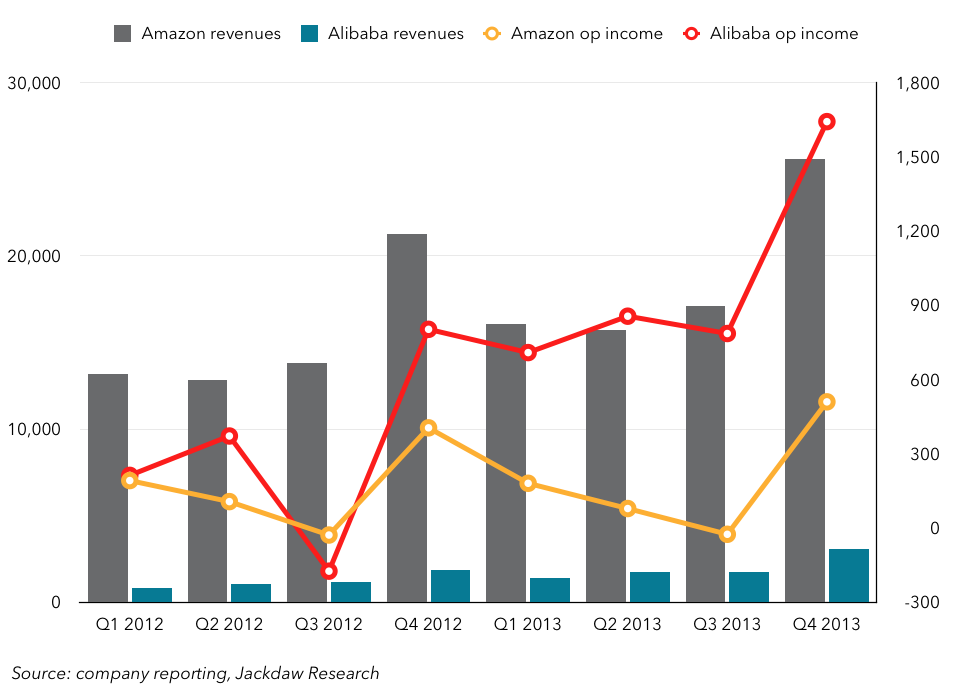

Secondly, the largest e-commerce player in China, Alibaba, has a very different model from Amazon, in that it doesn’t do any fulfillment of its own at all, merely acting as a go-between or marketplace for buyers and sellers who handle their own fulfillment. As such, it’s all third-party sellers, and there’s no fulfillment involved, which could go either way for Amazon. On the one hand, partners might find it very attractive to use Amazon for fulfillment rather than doing their own, but on the other it’s an unfamiliar model for both Chinese customers and businesses. In addition, Alibaba’s model generates a higher total transaction value than Amazon, with much lower revenues, but much higher profits:

It will be interesting to see how Amazon fares in China over the next few years, and whether its model can be successful at the same scale as Alibaba’s. China is clearly a huge area of investment for Amazon, but it faces significant local competition there as well.

Pingback: Haftalık #59 | Ozan Sağlam()

Pingback: Links – April 26, 2014 | Business Forecasting()