This is the latest in a series on major tech companies’ earnings for Q1 2014. As with the others, I won’t aim to be comprehensive, but rather to pull out some key figures and draw some conclusions from them.

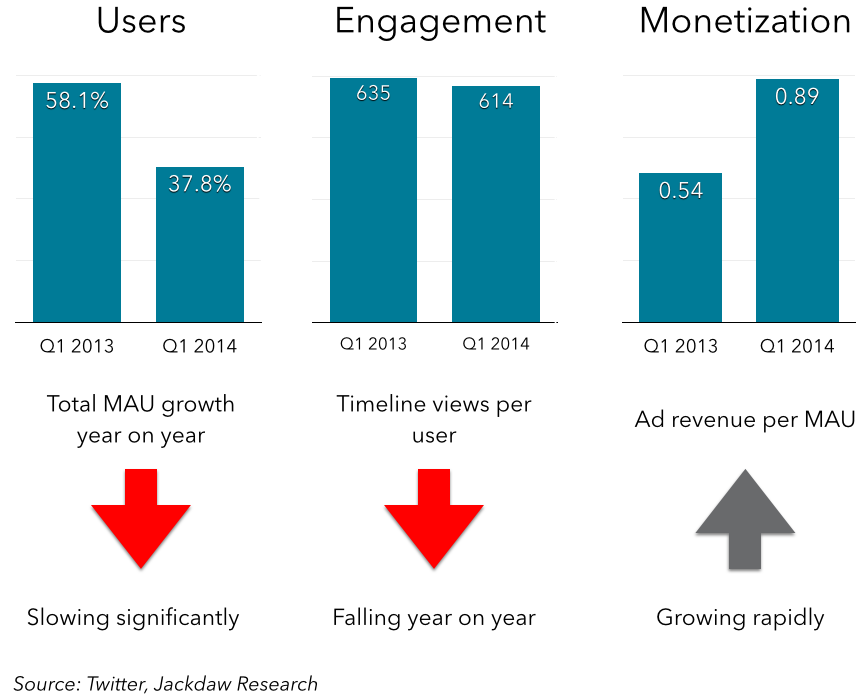

As with Facebook, I borrow Twitter’s own three-part approach to growth to gauge these companies’ potential, in a sort of scorecard. In each case, I try to use the metrics the companies themselves provide in these three categories: user growth, engagement and monetization. Below is my growth scorecard for Twitter:

The biggest difference between Facebook and Twitter in this regard is engagement. Whereas Facebook’s measure of engagement (DAUs as a % of MAUs) is rising globally and in all regions, the main metric Twitter offers – timeline views per user – is falling. Now, there’s apparently a good reason for this – Twitter changed the way certain features work in its mobile app, and that led to fewer timeline views recorded for similar levels of engagement. But as long as this is the (only) metric Twitter consistently provides to measure engagement, it’s going to get beaten up over it.

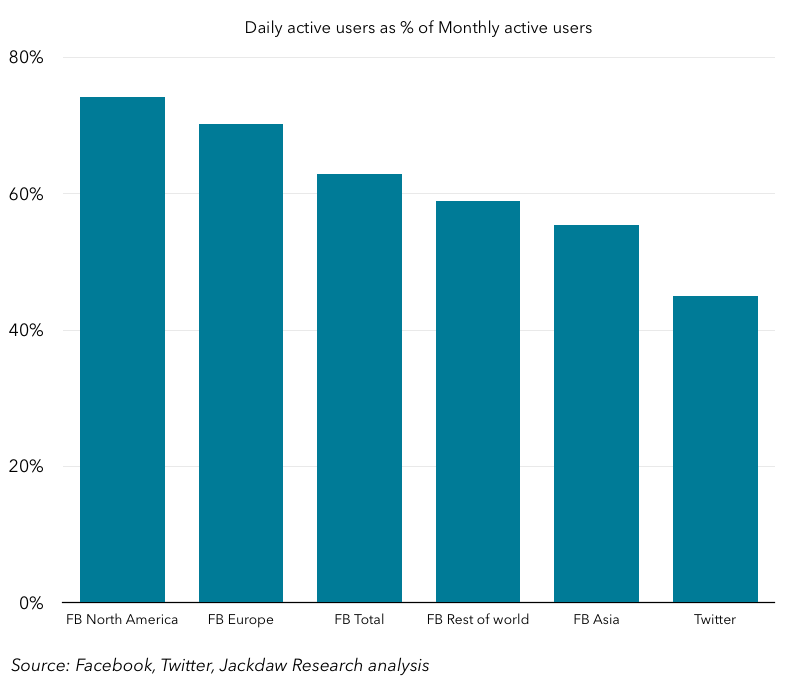

Twitter has given occasional glimpses at its own figures for DAUs per MAU, for example in its S-1 filing and again on today’s earnings call. But there’s too little data here to see long-term trends, and what little we do have compares unfavorably to Facebook’s equivalent metrics:

The 45% figure I’ve used for Twitter is an estimate based on today’s guidance that it was in the high 40s. As you can see from the chart above, that’s lower than Facebook’s engagement rate, even in its poorest performing region, Asia. And it’s way lower than Facebook’s engagement in North America and even globally. Twitter still fundamentally struggles with getting over half its users to make visiting Twitter a daily habit.

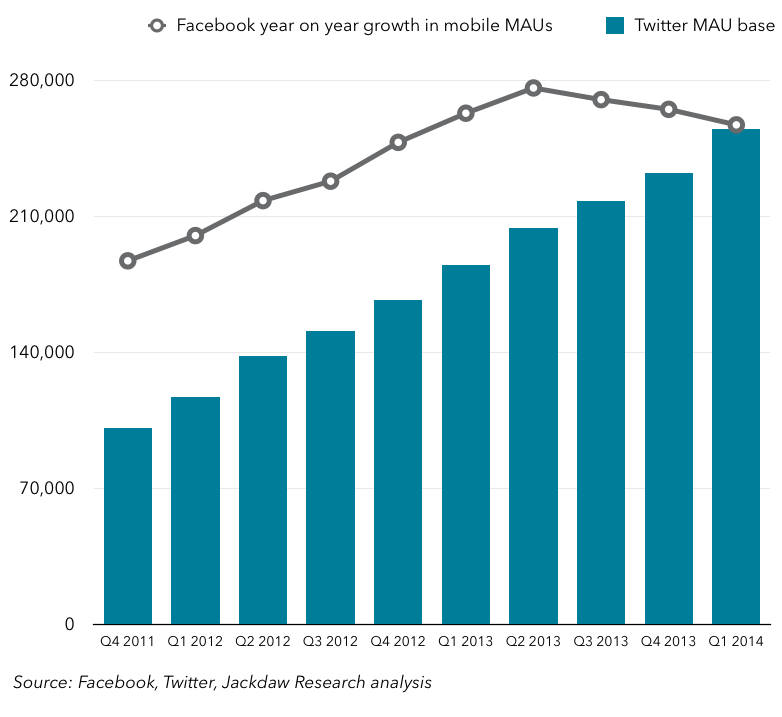

On other metrics, too, Twitter compares unfavorably to Facebook. There’s sheer scale, where Twitter’s base of MAUs is just barely catching up to Facebook’s annual growth in mobile MAUs:

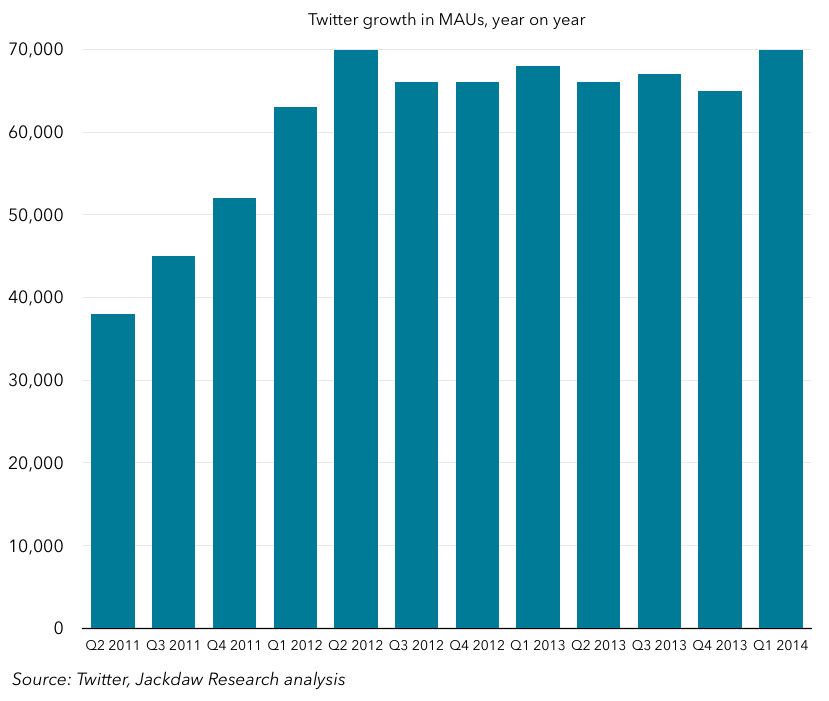

The reason for that is that Twitter’s growth is plodding along very consistently at between 65 and 70 million net MAU adds year on year each quarter, a number that’s remained consistent for the last two years:

The reason for that is that Twitter’s growth is plodding along very consistently at between 65 and 70 million net MAU adds year on year each quarter, a number that’s remained consistent for the last two years:

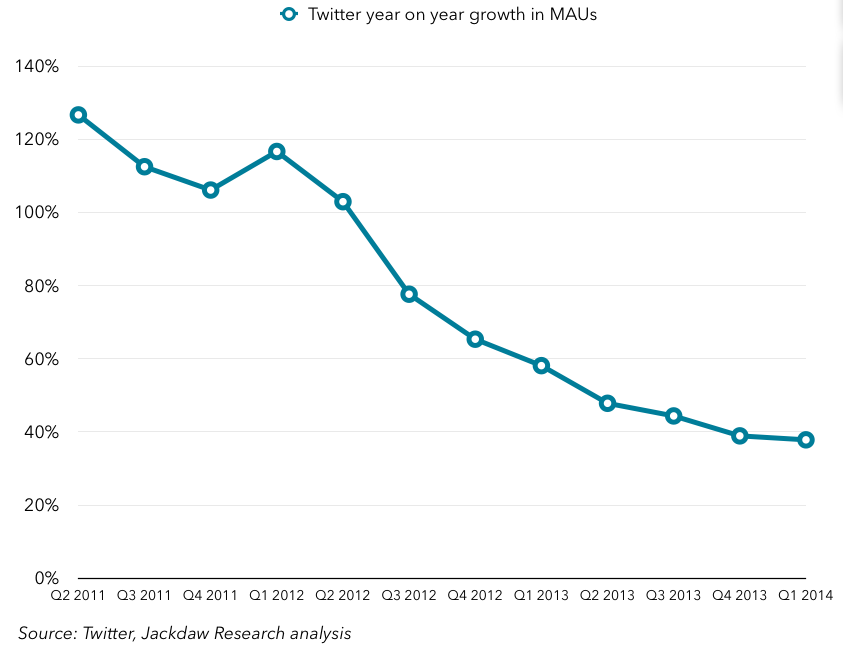

The problem is, whereas 70m represented 100% growth two years ago, it now represents less than 40% growth, so that the growth curve everyone is obsessed about looks like this:

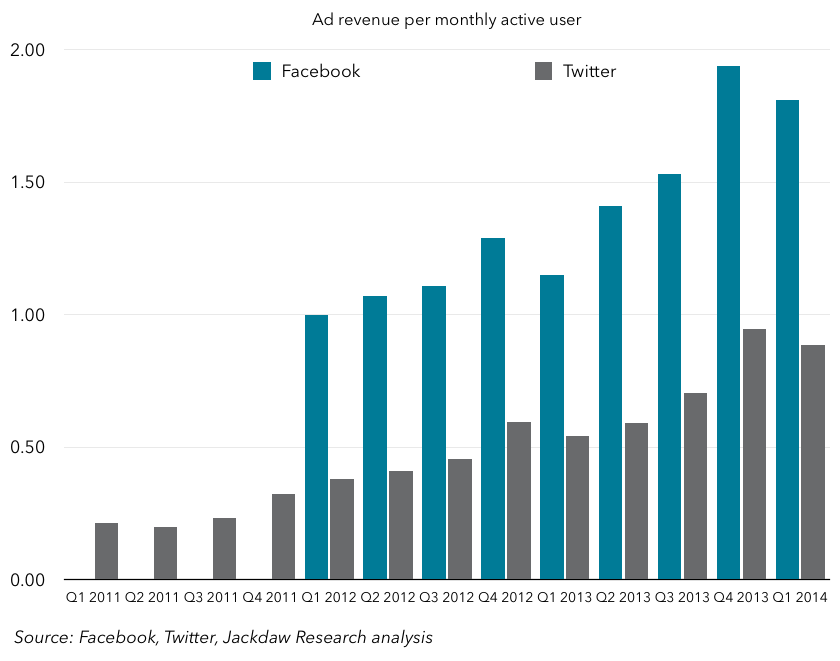

At this rate, Twitter will reach about 400 million users in two years from now, which is equivalent to Facebook’s current base in Asia alone. And then there’s monetization, where Twitter’s ad revenue per user, though growing rapidly, is still about half of Facebook’s on a global basis:

The challenge for Twitter is that Facebook feels like the most comparable company out there, but in almost every respect Twitter looks inferior. Twitter is fundamentally a much smaller business than Facebook, and it’s unlikely it will ever be able to bridge that gap unless something fundamentally changes.

It’s for that reason, then, that Twitter has started to play up its MoPub ad exchange and the 1 billion or so users it can reach with ads. It recognizes that its upside as a company and as a stock is fundamentally limited by the Twitter user base, which is growing slowly and generating relatively small spend per user. As such, Twitter is trying to get them to see the bigger picture in the form of MoPub. The fundamental challenge, though, is that Twitter is providing absolutely no data on this part of the business. And all its key metrics – number of monthly active users, ad revenue per user, timeline views per user and so on – are increasingly irrelevant to this part of the business.

Interestingly, as MoPub grows, Twitter will become less and less like Facebook and more and more like Google (especially Google following the DoubleClick acquisition), with revenues increasingly disconnected from specific, identifiable users. The challenge is that investors (and financial analysts) are fixated on the core Twitter business, because it’s measurable. Just look at the earnings call transcript to see analyst after analyst asking how MoPub can drive the “core” Twitter business. That’s the part of the business they understand, while MoPub is still a relative black box. Google’s business, too, is something of a black box, but it’s got a great track record of success at this point and investors are willing to buy into it. But with so little data to go on with regard to MoPub, Twitter’s investors can’t see beyond the “core” business, and that’s not looking so hot, which explains the hammering the stock took after earnings were released today.

The key for Twitter is to start to provide new sets of metrics that are better aligned with the larger business that MoPub enables, so that analysts and investors can start to see beyond the core business. But it also needs to start to provide better metrics for measuring engagement. If timeline views per user aren’t a good measure, stop reporting them and instead report something else – DAUs per MAU, time spent per user, the number of favorites and retweets (apparently up 26%) or something else that provides a truer representation of engagement.