This analysis is based on the data from US wireless operators’ earnings for Q1 2014. You can see a set of data published previously here, or a fuller set of data on Slideshare here. The deck is also embedded below:

Scale

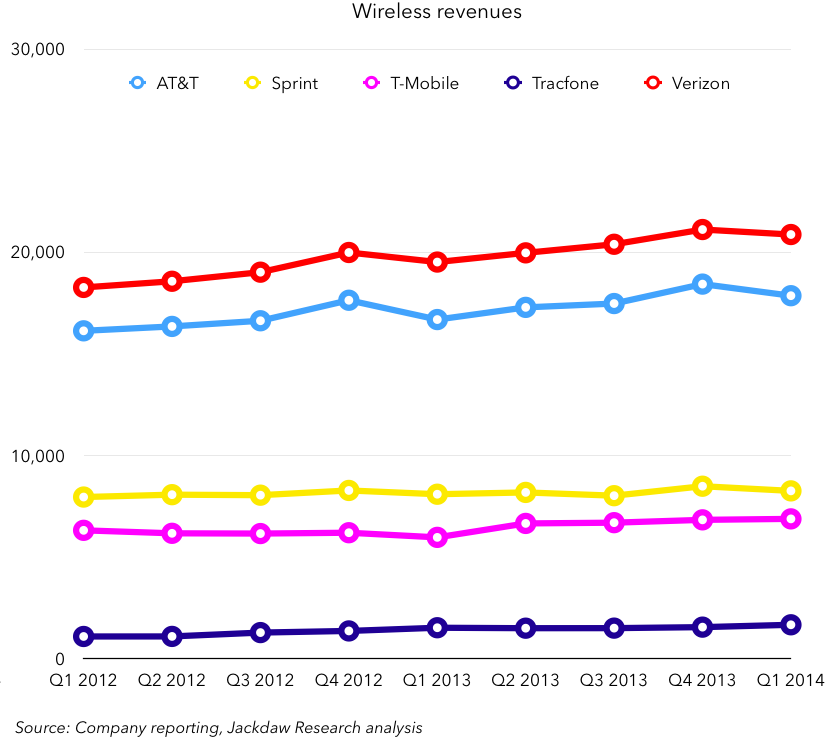

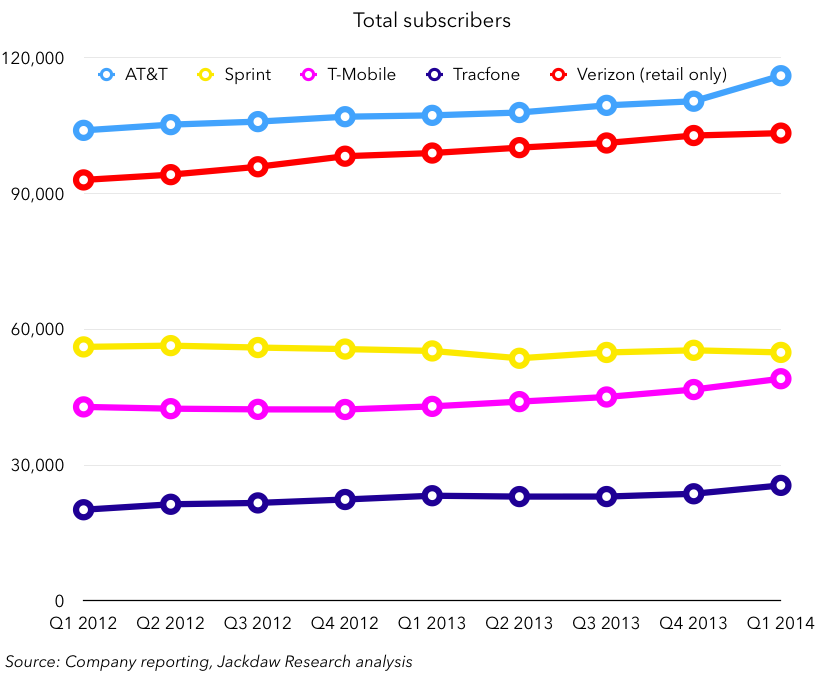

The US wireless market continues to be a game of four sets of players: AT&T and Verizon, Sprint and T-Mobile, Tracfone, and everyone else. The “everyone else” set is thinning out rapidly as more and more of the smaller regional carriers are snapped up by the bigger carriers, including Leap and MetroPCS in the last few months. Tracfone is included in the analysis here because it’s significant in scale, with as many prepaid subscribers as T-Mobile has postpaid subscribers, but of course its business model is entirely different as an MVNO. It is therefore excluded from a number of the comparisons below, either because they’re not meaningful or because Tracfone provides only limited data, as a subsidiary of America Movil. The revenues and total subscribers charts below are good illustrations of the scale differences between the three groups we’ll look at:

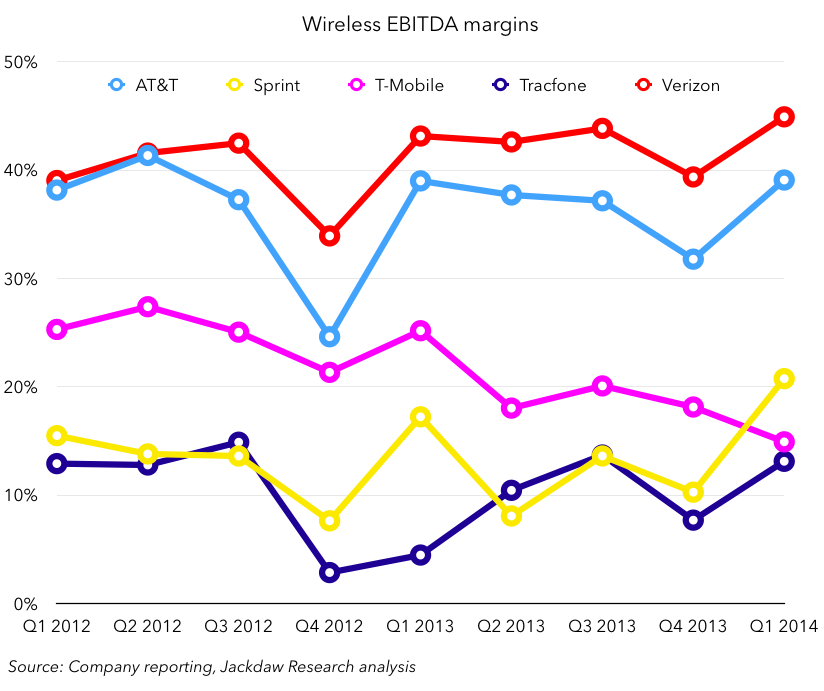

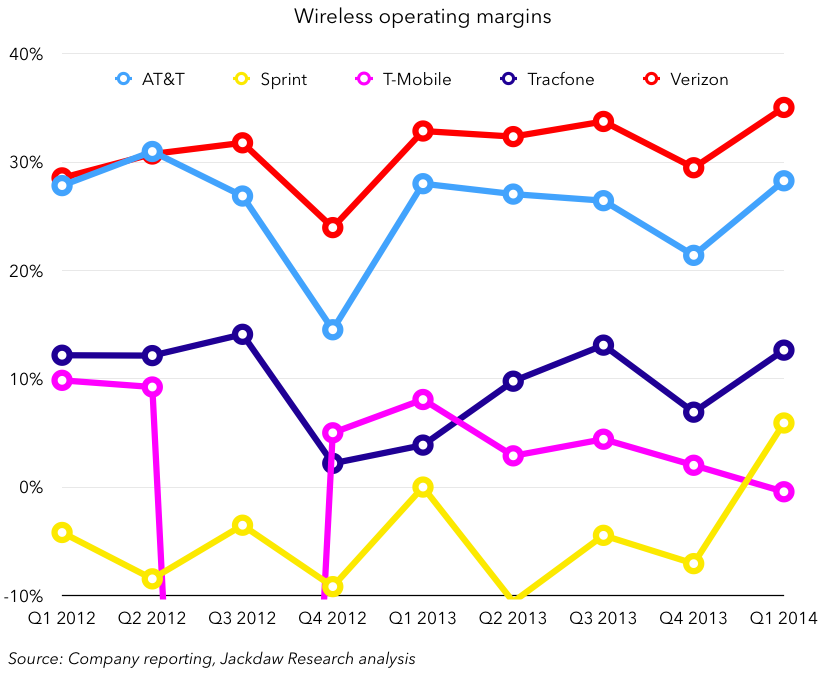

It seems impossible, now that penetration is reaching near saturation, that any of these three groups should ever overlap in terms of either total revenues or subscribers without some sort of M&A activity. The gaps are simply too large to be overcome through organic growth alone within the next few years, unless there is an implosion by one of the carriers. This scale leads to other financial characteristics, notably a marked difference in profitability between the major carriers:

Here, the bottom three occupy similar territory, but again the big two are way out in front, and it doesn’t seem likely that their paths will cross at any point with the smaller carriers. The other thing to notice here is that T-Mobile is suffering from declining profitability as it pursues growth at all costs, reducing prices, offering significant financial incentives for switching (such as paying ETFs), and subsidizing international calls and roaming, which have real fixed costs outside of T-Mobile’s control. At this point, T-Mobile is coming to resemble Amazon in its combination of rapid growth and very thin operating margins. Neither company can keep this up forever.

Subscriber mix shifting

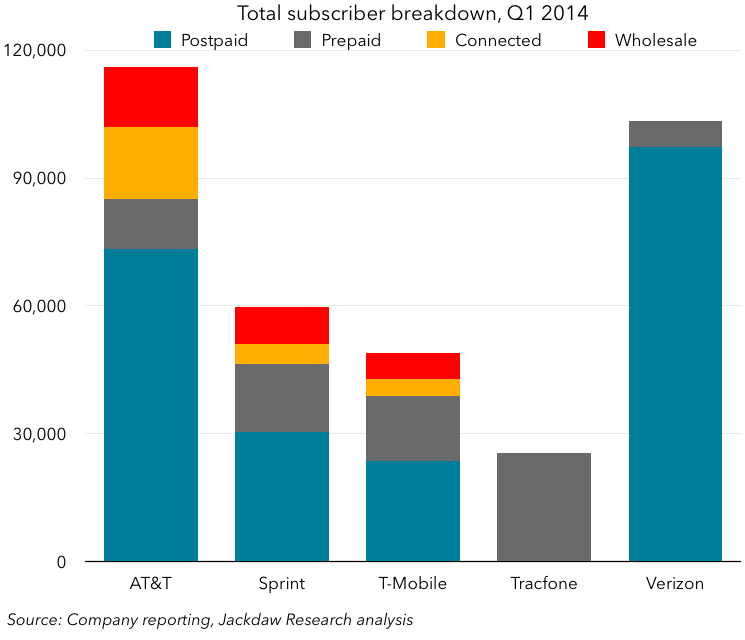

The mix of subscribers at each of the four big operators is fascinatingly different, and their mix of net adds even more so. The picture here is complicated by the fact that Verizon only reports retail subscriber data, so its connected devices and wholesale businesses are a mystery. However, the resulting picture of the current subscriber mix is as follows:

Verizon dominates the postpaid market, with significantly more subscribers than AT&T, and massively more than any other operator, though the fewest prepaid subscribers of any of the five big operators. Sprint, T-Mobile and AT&T all have much more mixed bases, with significant prepaid, connected device and wholesale bases as well as postpaid. Prepaid is dominated by Tracfone, with more subscribers than T-Mobile has postpaid subs as I mentioned above. AT&T dominates connected devices already and is further pulling away with much higher net adds (see chart below). Both Sprint and Verizon had significant footholds in the connected devices business in the past (with Kindle and OnStar respectively) but have ceded much of the market to AT&T in the last couple of years.

Verizon dominates the postpaid market, with significantly more subscribers than AT&T, and massively more than any other operator, though the fewest prepaid subscribers of any of the five big operators. Sprint, T-Mobile and AT&T all have much more mixed bases, with significant prepaid, connected device and wholesale bases as well as postpaid. Prepaid is dominated by Tracfone, with more subscribers than T-Mobile has postpaid subs as I mentioned above. AT&T dominates connected devices already and is further pulling away with much higher net adds (see chart below). Both Sprint and Verizon had significant footholds in the connected devices business in the past (with Kindle and OnStar respectively) but have ceded much of the market to AT&T in the last couple of years.

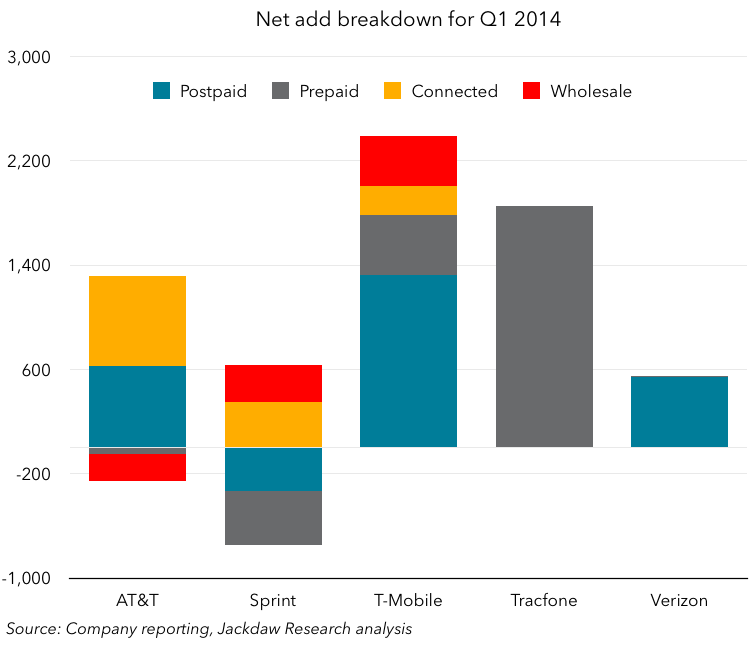

The net add picture is different again, though Tracfone again dominates prepaid net adds, and T-Mobile is the only other carrier adding subs prepaid subs. T-Mobile dominated postpaid net adds though, too, and Verizon – which has had very healthy net adds until this quarter – dropped quite a bit from its normal levels. This was apparently due to losing low end feature phone subscribers to other carriers (presumably mostly T-Mobile) and it’s said it’s fixed that issue with some new pricing, so it should rebound next quarter.

AT&T appeared to add a comparatively healthy number of postpaid subs, but it turns out that they were split evenly between phones and tablets. So, of AT&T’s positive net adds, only about a quarter were smartphones, half were connected devices and another quarter were tablets. That’s a far cry from T-Mobile, which added just 67,000 postpaid tablets and tons of phone subscribers. Sprint continues to struggle to add net subscribers, losing both postpaid and prepaid subs and offsetting some of those losses with wholesale and connected device adds.

AT&T appeared to add a comparatively healthy number of postpaid subs, but it turns out that they were split evenly between phones and tablets. So, of AT&T’s positive net adds, only about a quarter were smartphones, half were connected devices and another quarter were tablets. That’s a far cry from T-Mobile, which added just 67,000 postpaid tablets and tons of phone subscribers. Sprint continues to struggle to add net subscribers, losing both postpaid and prepaid subs and offsetting some of those losses with wholesale and connected device adds.

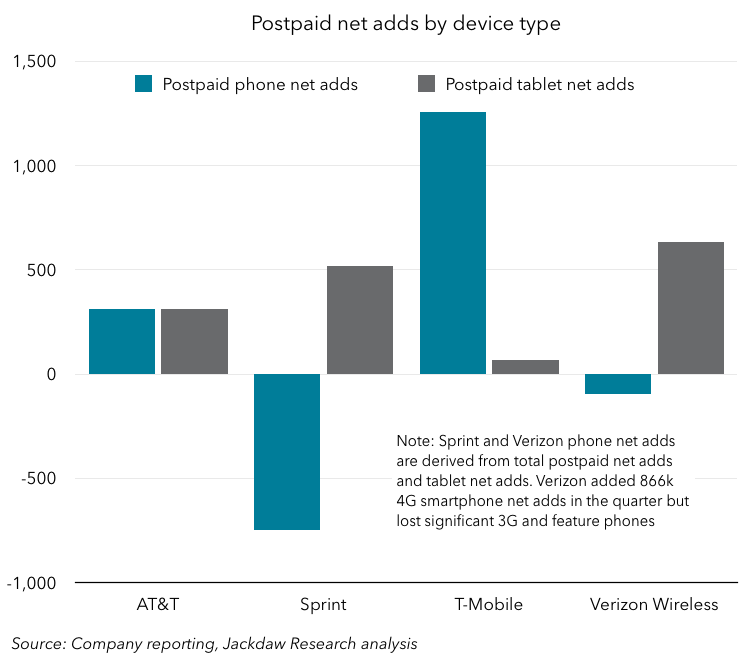

A further breakdown of the four network operators’ postpaid net adds by device is shown below, and it illustrates the interesting split between tablets and smartphones at Verizon, Sprint and AT&T:

Verizon did say that it added 866,000 postpaid 4G smartphone subscribers, so its negative phone adds are all due to a massive loss in 3G and feature phone subs. But the three biggest carriers all saw tablet adds equal to or greater than smartphone adds in the quarter, which is a big shift.

Verizon did say that it added 866,000 postpaid 4G smartphone subscribers, so its negative phone adds are all due to a massive loss in 3G and feature phone subs. But the three biggest carriers all saw tablet adds equal to or greater than smartphone adds in the quarter, which is a big shift.

Changing subsidy models

Although T-Mobile’s Un-Carrier moves have had some impact on all carriers’ churn and net adds, I’d argue that its shift away from subsidies and towards installment pricing for smartphones is going to have a much wider-ranging and longer-lasting impact on the industry. Verizon remains the holdout in aggressively embracing subsidy pricing (which may be wise), though it has at least caved on pricing finally, acknowledging that subscribers shouldn’t have to pay twice for a device. But all three other major carriers have now embraced installment pricing, and Sprint and T-Mobile are providing useful data for understanding the impact on their finances. Some of that data is presented below. First, Sprint:

That chart shows Sprint’s net wireless subsidy per quarter, which fell by about 70% from Q1 2013 to Q1 2014 even though smartphone sales were fairly constant. It also shows the percentage of equipment cost which was covered by equipment payments, which has risen significantly in the last two quarters, from the low 30s to almost 50%. Sprint is very successfully shifting its subscribers away from subsidized handsets and towards handsets they explicitly pay for themselves.

That chart shows Sprint’s net wireless subsidy per quarter, which fell by about 70% from Q1 2013 to Q1 2014 even though smartphone sales were fairly constant. It also shows the percentage of equipment cost which was covered by equipment payments, which has risen significantly in the last two quarters, from the low 30s to almost 50%. Sprint is very successfully shifting its subscribers away from subsidized handsets and towards handsets they explicitly pay for themselves.

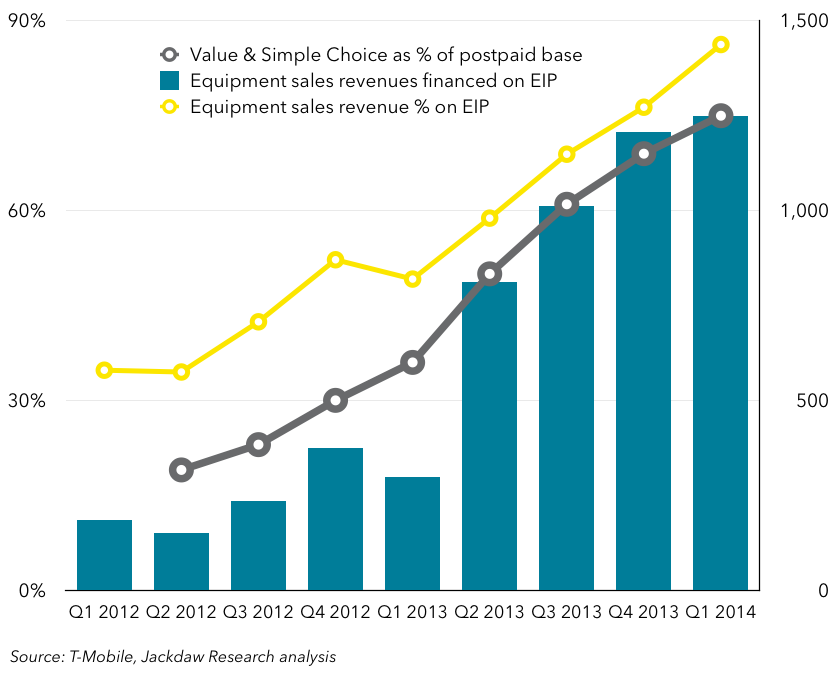

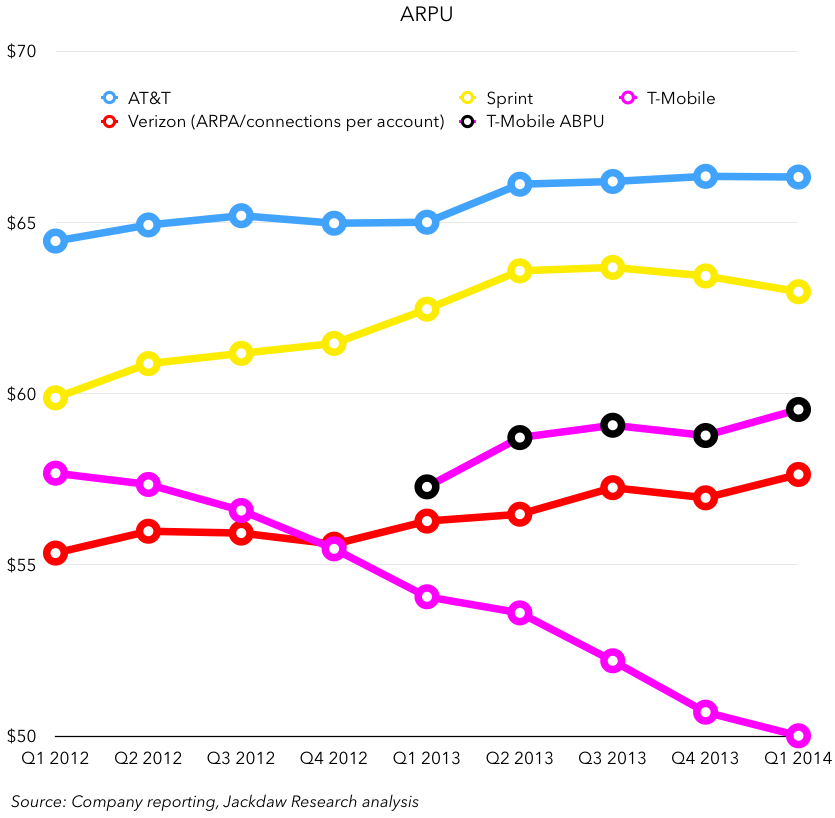

Now, T-Mobile’s numbers: T-Mobile is further ahead than any of the other carriers on this path, having been walking down it for longer, and it’s also been most aggressive in getting customers to shift. As such, 86% of equipment sales revenue is now on equipment installment plans, and 80% of customers are on plans where they’re going to be paying for their own devices. Both of those numbers should reach 100% over the next year or two, meaning that T-Mobile will have entirely shifted the costs of devices out of the murky world of subsidies and into explicit handset payments. The result is that its reported service ARPU is falling rapidly:

T-Mobile is further ahead than any of the other carriers on this path, having been walking down it for longer, and it’s also been most aggressive in getting customers to shift. As such, 86% of equipment sales revenue is now on equipment installment plans, and 80% of customers are on plans where they’re going to be paying for their own devices. Both of those numbers should reach 100% over the next year or two, meaning that T-Mobile will have entirely shifted the costs of devices out of the murky world of subsidies and into explicit handset payments. The result is that its reported service ARPU is falling rapidly:

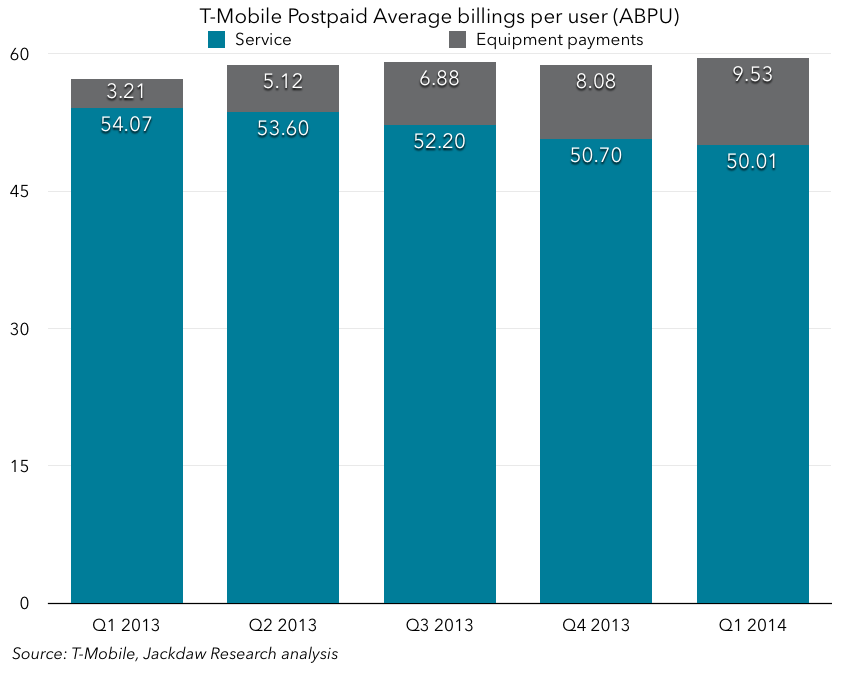

However, it’s now started reporting Average Billings Per User (ABPU) as well, which includes installment payments and is actually rising. The components of that new metric are as follows:

As you can see, average monthly equipment payments are already at almost $10, up from just $3 a year ago, and we can expect that number to rise significantly over the coming year until it reaches an equilibrium at around $20-25. Meanwhile, ARPU will continue to fall. AT&T hasn’t started breaking these numbers out so explicitly, but it has started to acknowledge that ARPU won’t rise as fast when considered on its own, and is using ARPU + NEXT as a better measure of true growth over time (though it hasn’t given the underlying numbers).

As you can see, average monthly equipment payments are already at almost $10, up from just $3 a year ago, and we can expect that number to rise significantly over the coming year until it reaches an equilibrium at around $20-25. Meanwhile, ARPU will continue to fall. AT&T hasn’t started breaking these numbers out so explicitly, but it has started to acknowledge that ARPU won’t rise as fast when considered on its own, and is using ARPU + NEXT as a better measure of true growth over time (though it hasn’t given the underlying numbers).

Conclusions

The quarter was certainly an interesting one – T-Mobile dominated growth, Verizon showed the first chinks in its armor after remaining stubbornly on top despite the onslaught from T-Mobile and competitive responses from the other carriers. Tracfone remains a real success story, but one the industry largely seems to ignore, partly because it’s so focused on prepaid and partly because the network operators benefit from its wholesale business. T-Mobile’s shift from subsidies to installment payments for devices is changing not only its own business but the other carriers’ too, and apparently for the better (at least for now). But all T-Mobile’s moves are coming at a significant cost in terms of profitability, and may well be unsustainable. Ultimately, only a merger between Sprint and T-Mobile can close the gap with AT&T and Verizon, but it remains a tough sell to regulators.