As with last quarter’s Apple earnings call, there has been lots of handwringing about why iPad shipments aren’t growing this quarter. I’ve done a fair amount of thinking about this, and did some analysis as part of the recent Apple profile my clients received. I thought I’d share some of that thinking here, and expand on it a bit. A fuller review of Apple’s earnings will be coming shortly.

Update: In-depth review of Apple’s earnings is up here now.

Shipments versus the base

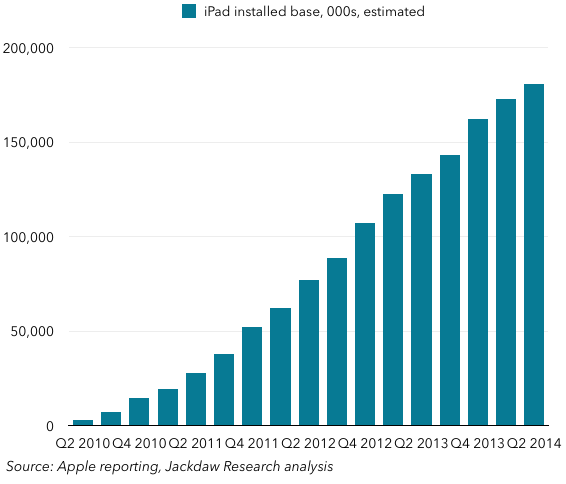

First, it’s important to be clear about one very important thing: the difference between iPad shipments and the iPad base. Stagnant or even shrinking shipments don’t mean the base is shrinking, and in fact it’s likely growing at a decent rate. Here’s my estimate of the iPad installed base over time: You’ll see that it’s been growing at a fairly steady clip, and that it’s reached about 180 million. Naturally, I’ve made some assumptions about how long people hang on to their iPads based on various data sources, so it’s not 100% accurate, but it’s likely a good guess at what’s been happening. So the first thing to note is that the number of people who have iPads is growing, not flat or shrinking, even if shipments are stagnant or falling slightly.

You’ll see that it’s been growing at a fairly steady clip, and that it’s reached about 180 million. Naturally, I’ve made some assumptions about how long people hang on to their iPads based on various data sources, so it’s not 100% accurate, but it’s likely a good guess at what’s been happening. So the first thing to note is that the number of people who have iPads is growing, not flat or shrinking, even if shipments are stagnant or falling slightly.

Three reasons for shrinking shipments

On, then, to why shipments are shrinking. I suspect there are three reasons:

- The saturation point for tablets is much lower than for smartphones, and as such the ceiling for iPad growth is significantly below the ceiling for the iPhone. The iPhone is part of a ubiquitous product category (phones) and is heavily subsidized by carriers, so both the entire category and the iPhone’s addressable segment are larger than for the iPad.

- The iPad has grown much faster towards that saturation point than the iPhone did, benefiting from the iPhone’s installed base, App Store, and retail channels.

- The iPad has faced meaningful competition much faster than the iPhone did. It took about 4-5 years for Android-based competitors to offer devices which began to really compete with the iPhone head on, but it took only 1-2 years for competitors to provide meaningful competition to the iPad. In addition, several competitors including Amazon, Google/Asus and most importantly Samsung have priced their offerings at or below cost, something which didn’t happen in smartphones.

For all these reasons, iPad shipments have tailed off much more quickly than iPhone shipments as the iPad approaches mass-market consumer saturation much more quickly and faces steeper competition than did the iPhone.

One more reason – which points to future growth

But there’s one more very important reason that iPad shipments have slowed down, which also points to a future acceleration in growth, and that’s replacement cycles. The iPhone benefits from carrier-induced upgrade cycles which both prompt and subsidize upgrades, but the iPad doesn’t. As such, iPad users facing the full cost of upgrading their device have a different financial equation, and given the iPad’s status as an occasional device rather than a constantly-present one, owners are upgrading their devices less frequently.

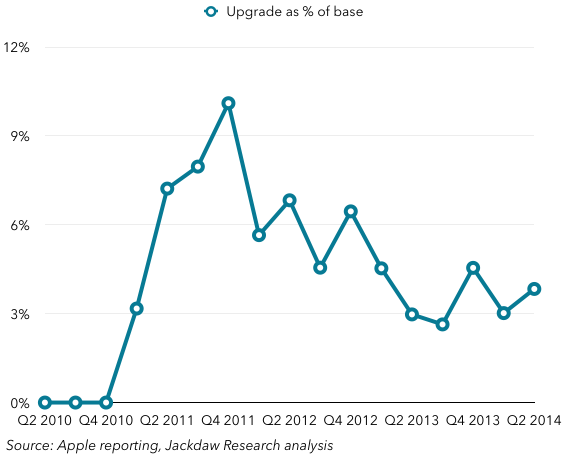

Look at the numbers Apple has begun to give for iPad buyers who were new to iPads, or new to tablets, in the last two quarters: last quarter, the “new to iPad” figure for the previous six months was 70%, and this quarter the slightly different “new to tablets” figure was 50%. Unfortunately, we don’t have a long history for this metric, but we can again make some reasonable assumptions to arrive at a picture for what’s driving iPad shipments. For starters, we know that over the last several quarters half or fewer of iPad shipments have come from upgrades. That’s pretty amazing given the size of the base we looked at above. The chart below shows estimated upgrades as a percentage of the iPad installed base, over time:

The line bounces around a bit, but it’s been settling down to between about 3 and 6% of the base, meaning during any given quarter only 3-6% of people who own iPads buy a new one. That number, though, is likely skewed somewhat by the fact that a small number of owners upgrade more frequently, while the majority hold onto their iPads much longer. It’s quite likely that the amount of time a typical user owns one before upgrading is well over two years, and perhaps closer to three. Now, let’s look at age profile of the iPad base:

The line bounces around a bit, but it’s been settling down to between about 3 and 6% of the base, meaning during any given quarter only 3-6% of people who own iPads buy a new one. That number, though, is likely skewed somewhat by the fact that a small number of owners upgrade more frequently, while the majority hold onto their iPads much longer. It’s quite likely that the amount of time a typical user owns one before upgrading is well over two years, and perhaps closer to three. Now, let’s look at age profile of the iPad base:

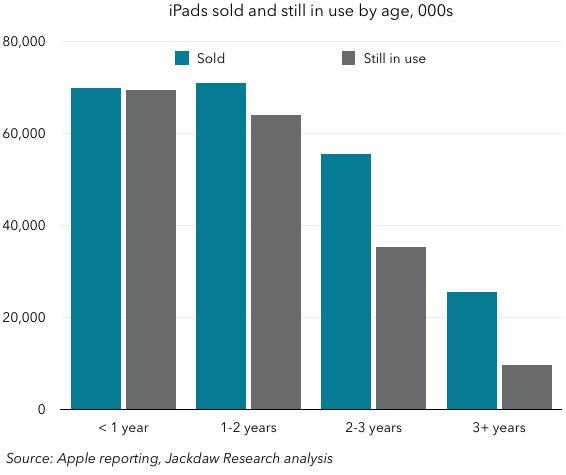

What you’ll see is that, because of the way iPad shipments took off in 2011, there’s a much bigger base of iPads 2-3 years old than there are older ones, and a bigger base still of iPads 1-2 years old and less than one year old. As such, over the next year or so, more of these iPad owners will reach the stage where they want to upgrade, especially as Apple releases new iPad hardware and as older devices are no longer well supported by the latest version of iOS. If upgrades continue at a similar rate to what we’ve seen so far, this bulge in the base should cause a similar bulge in sales over the next year or so, perhaps starting as soon as late Q3.

The death of tablets has been greatly exaggerated

For all these reasons, I believe the much-discussed death of tablets has been greatly exaggerated. By coincidence, just as iPad sales have reached this point in their lifecycle, PCs are going through a periodic upgrade cycle spurred by a release in pent-up enterprise demand, which makes it look like the two trends are related. But my suspicion is that longer term we’ll see the PC market return to slow decline, while the tablet market picks up a little, even if it doesn’t immediately return to past rapid rates of growth.

In addition, I think the iPad specifically will benefit from the same sort of mosaic strategy for growth I discussed here. Apple announced on today’s earnings call that iPad sales to education to date have reached 13 million, which was incidentally the same level of sales overall iPads hit just this quarter, or about 6% of all-time iPad sales. That’s pretty small in percentage terms (though 13 times as large as the Chromebook numbers Google released this week), and as more schools and colleges implement iPad programs it should spur continued growth in this segment. In addition, Apple’s deal with IBM should further stimulate growth in the enterprise. It also won’t be blockbuster growth, but should help drive overall numbers higher. For all these reasons, I’m optimistic about iPad growth going forward.

Lastly, for those talking as if the iPad business needs saving, let’s just remember some basic facts about Apple’s iPad segment:

- It’s selling 10-20 million units a quarter

- It’s generating revenues of $5-10 billion per quarter, or an annual run rate of about $30 billion, bigger than McDonalds or Time Warner

- Margins are very healthy.

To put it in context, Apple as an entire company didn’t hit this scale until 2008, a year after it launched the iPhone.