After a couple of days of talking to various reporters about the Sprint and T-Mobile news from this week, I thought I’d take some time to write up my thoughts on the situation. I already posted some thoughts on Dan Hesse’s tenure at Sprint here. This has turned into a longish post, so here are some signposts for you: the first section deals with why the Sprint-T-Mobile merger made sense, the second deals with where Sprint goes from here, the third deals with where T-Mobile goes from here, and at the end I talk about other issues relating to T-Mobile, namely the other potential merger offers, T-Mobile’s claim to be the largest prepaid carrier in the US, and its goal of catching Sprint by the end of the year (each of those hyperlinks will take you to the relevant part of the post).

Why the merger made sense

I did a long post previously about why the Sprint-T-Mobile merger made sense. If you haven’t read that, I suggest you do, because I won’t cover the same ground in detail again here and the basic arguments haven’t changed even if some of the numbers have. In brief, Sprint and T-Mobile both suffer from their small scale relative to Verizon and AT&T, which manifests itself especially in advertising spend, network costs, retail distribution and purchasing power. Sprint and T-Mobile have attempted to overcome their ad spend disadvantage through various means, Sprint with its Framily plans, which create a viral effect as people try to sign up friends, family and apparently complete strangers; and T-Mobile with its heavy use of social media for marketing. And SoftBank’s acquisition of Sprint and Brightstar has allowed the combined company to generate greater purchasing power in devices and accessories. But a fundamental and significant gap remains.

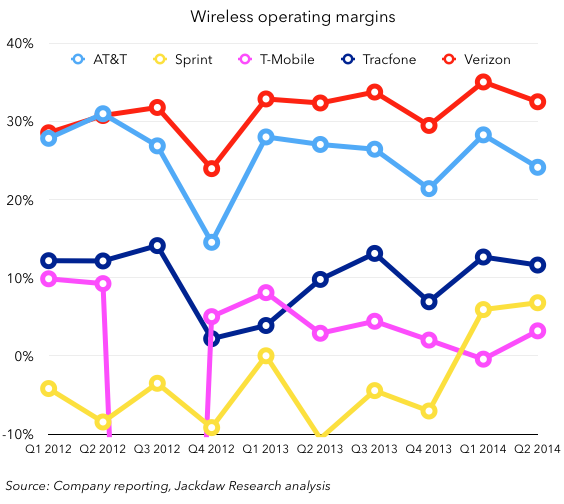

This is evident nowhere so much as in the various companies’ margins, as shown below (this chart is an excerpt from the deep dive on US wireless operators’ Q2 performance which I’ll be publishing early next week. A preview is available on FierceWireless now):

As you can see, both T-Mobile and Sprint are languishing in the single digits, while AT&T and Verizon were at around 25% and over 30% respectively last quarter. This is a direct result of their lack of scale, and slow organic increases in subscribers won’t solve this problem anytime soon. This is the single greatest argument for a merger between the two, and nothing else can solve this fundamental problem. The fifth company in the mix there is Tracfone, which is a mobile virtual network operator (MVNO), which piggybacks off the carriers’ networks. Most of its costs are variable rather than fixed, and as such it doesn’t have the same scale disadvantages, but it has to pay wholesale rates to the carriers, which doesn’t allow it to be as profitable as AT&T and Verizon either.

As you can see, both T-Mobile and Sprint are languishing in the single digits, while AT&T and Verizon were at around 25% and over 30% respectively last quarter. This is a direct result of their lack of scale, and slow organic increases in subscribers won’t solve this problem anytime soon. This is the single greatest argument for a merger between the two, and nothing else can solve this fundamental problem. The fifth company in the mix there is Tracfone, which is a mobile virtual network operator (MVNO), which piggybacks off the carriers’ networks. Most of its costs are variable rather than fixed, and as such it doesn’t have the same scale disadvantages, but it has to pay wholesale rates to the carriers, which doesn’t allow it to be as profitable as AT&T and Verizon either.

Ultimately, though, the merger faced enormous regulatory opposition, and it was by no means a certainty that it would go through. US regulators would apparently rather see a short-term continuation of the current market structure than a more sustainable long-term competitive environment. I suspect that will come back to bite them a year or two from now. The challenge is that neither Sprint nor T-Mobile is exactly on the brink of collapse today, and so it’s easy to argue the situation isn’t urgent. However, each company faces fundamental challenges beyond those related to scale, and I’ll address those below. Continue reading