Note to new readers: I use calendar rather than fiscal quarters for easier comparability between companies’ results. As such, I use Q3 2014 universally to refer to the period ending September 2014, even though some companies (in this case Microsoft) use a different reporting calendar). All the charts and analysis below use calendar rather than Microsoft fiscal quarters. This is part of a series on major tech companies’ Q3 2014 earnings. Prior analysis on Microsoft can be seen here.

There are four sections in this post – click below to jump to each of them:

- Consumer hardware performing surprisingly well

- Cloud run-rates and actuals

- Office in transition

- Online advertising divergence continues

Consumer hardware performing surprisingly well

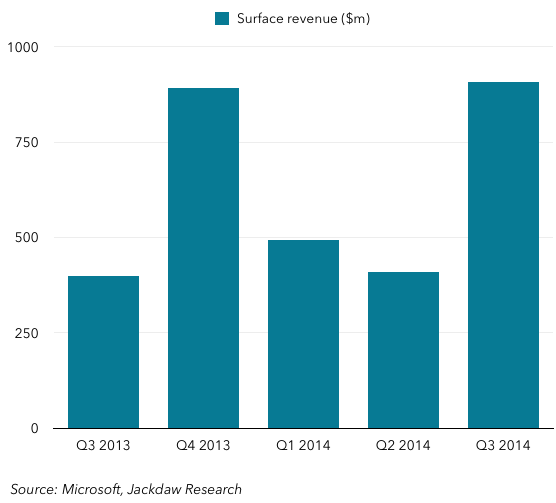

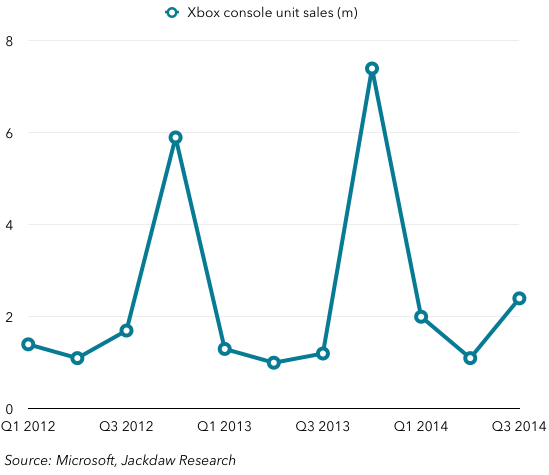

One of the most surprising things about today’s earnings was that the consumer hardware businesses, which are important to Microsoft’s strategy but have performed poorly, all got a bit of a boost this quarter. Xbox, Surface and Lumia devices all had strong year on year growth:

All three device categories saw record results, in fact – Lumia sales and Surface revenue were both the highest they’ve ever been, while Xbox unit sales were the highest they’ve ever been outside the seasonally much higher fourth calendar quarter. Now, we have to put all this in context: both Lumia and Surface sales are dwarfed by the respective markets in which they compete. But on a relative basis, the company continues to see growth in both categories, and the Xbox year on year growth was solid too.

All three device categories saw record results, in fact – Lumia sales and Surface revenue were both the highest they’ve ever been, while Xbox unit sales were the highest they’ve ever been outside the seasonally much higher fourth calendar quarter. Now, we have to put all this in context: both Lumia and Surface sales are dwarfed by the respective markets in which they compete. But on a relative basis, the company continues to see growth in both categories, and the Xbox year on year growth was solid too.

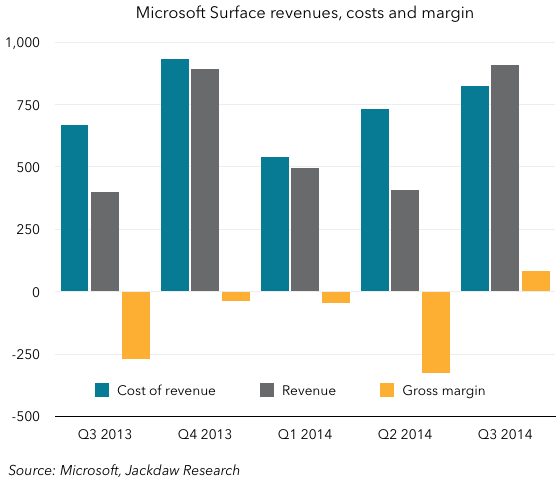

Now, much has been made of the fact that Microsoft reported a positive gross margin for the first time for the Surface as well. Long-time readers will now that I have teased estimated gross margin numbers out of Microsoft’s SEC filings for the past few quarters, so I thought I’d provide an update on the same basis. Here’s the chart including this quarter’s numbers:

As you can see, the number does indeed seem to be positive this quarter on the basis of my analysis, at a little under $100 million. That’s a gross margin of around 9%, which is not earth-shattering and in fact about half the gross margin of the phone business at Microsoft. But it’s progress, as with the growth numbers above. There’s a long way to go to get to the kind of gross margins that would lead to true profitability once marketing and other costs are factored in. How many Surface devices did Microsoft sell in the quarter? Well, they won’t say, but given the new version starts at $800, it’s entirely possible that the company sold a million or fewer Surface tablets in total, and likely well under a million Surface Pro 3s in their first full quarter on sale. It sold about ten times as many Lumia devices, and about 40-50 times as many mobile phones, just for comparison’s sake.

Cloud run-rates and actuals

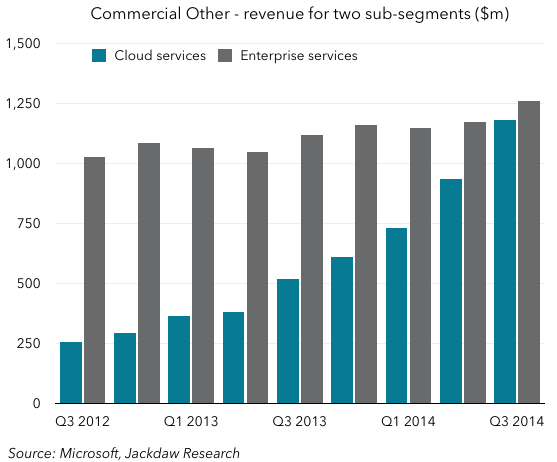

Much was made last quarter of Microsoft’s cloud “run-rate” which turned out to be based on a single month of sales, somewhat unconventionally. Here, too, I’ve estimated cloud revenues in the past and will do so again here. Here are my estimated numbers for Cloud and Enterprise Services, the two major components of the Commercial Other segment at Microsoft:

Last quarter, the run-rate was said to be $4 billion, and I pointed out that it wasn’t on the basis of the full quarter’s results, but that the trajectory was clearly there to support that claim. This quarter, the number did indeed cross $1 billion (it was just under $1.2 billion), so the run-rate now on a quarterly basis is almost enough to carry it to $5 billion for the year. This business clearly is growing very quickly, and we’re getting to some very big numbers. Last quarter it looked like Cloud Services might overtake the older and slower-growing Enterprise Services category for the first time. It didn’t – mostly because Enterprise Services grew faster – but almost certainly will next quarter.

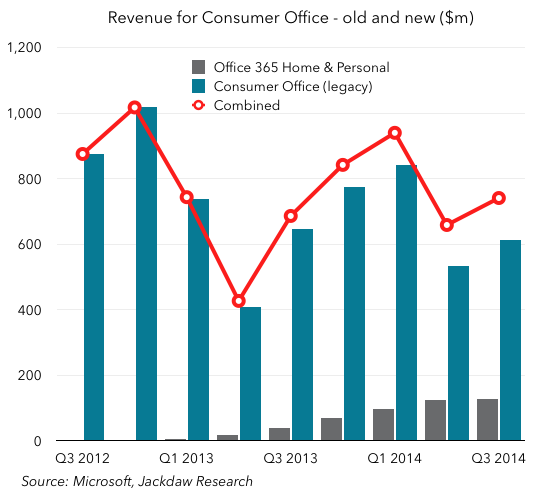

Office in transition

Microsoft used to report a year on year growth rate for Consumer Office, but it was based solely on legacy Office sales to consumers, and excluded the newer Office 365 versions for consumers. This quarter, it changed its reporting to reflect the overall picture, which is actually fairly reassuring. The combined number is growing ever so slightly year on year, as shown in the chart below (again, the numbers are my extrapolations from Microsoft’s SEC filings):

This is a somewhat cyclical business, so the key is to compare Q3 with last year’s Q3 rather than looking at quarter-to-quarter changes. Office 365, of course, is not cyclical in nature, since it’s subscription-based rather than a one-off sale. But it’s still much smaller, so it doesn’t affect the overall line much.

One interesting thing to note is that Office 365 Home and Personal subscribers grew strongly, from just 2 million a year ago and 5.6 million last quarter to 7.1 million this quarter. However, revenue from those subscribers seemed to barely budge as far as I can tell (I have a couple of different ways of arriving at this figure and they end up in almost exactly the same place). The number seems to have stayed at around $125m for the quarter from last quarter to this, despite the growth in subscribers. There are two possible explanations, which I think both contributed to this: Microsoft has begun a strategy of giving away some of its paid services with new hardware purchases, so some of these subscribers may not be paying subscribers (at least not yet). In addition, the Personal version of Office 365, which retails for $70/year instead of $100/year, went on sale shortly before the quarter began, so that may be starting to drag down the average price users are paying. It’s also worth remembering that these sales are the best indicator of how much people are using the full versions of Office for iPad. The conclusion: not that many.

Online advertising divergence continues

As with Google and Yahoo, Microsoft’s online advertising business continues to see divergent trends around search and display advertising. Here are my estimates for these two businesses:

As you can see, Display advertising revenue, which was almost as high as Search revenue two years ago, has fallen to a fraction of it, while Search revenue continues to grow reasonably strongly year on year. Bing and the Yahoo arrangement seem to be working well for Microsoft, but it’s struggling to make a dent in Display advertising despite revamped MSN, Outlook.com and other products over the past year. Given Microsoft’s strategy of attacking Google over its use of advertising to fund its products, I’m starting to wonder whether Microsoft shouldn’t just strip out the ads from some of these products and run them at a loss as platform differentiators, much as Apple bundles many of its services into purchases of devices.

That’s it for now – I may have more later in this busy earnings period. Amazon should be next up, likely tomorrow.