Notes: this is part of a series on major tech companies’ Q4 2014 earnings. All past earnings posts can be seen here, and all earnings posts for Q4 2014 can be seen here. For the sake of easy comparisons and transparency, I always use calendar quarters in my analysis. Hence, Q4 2014 in this and every post on this blog means the quarter ending December 2014, even though some companies (Apple included) have fiscal years that end at other times of the year.

A blowout quarter

The hardest posts to write are often the ones where it’s utterly uncontroversial that the results were astonishingly good, and that was definitely the case with Apple’s record-breaking earnings today. So instead of hashing over the same stuff as everyone else is, I’m going to try to pull out a few possibly overlooked data points. Apple changed its reporting structure in a couple of ways this past quarter, and that gave us one or two new insights while also sadly burying some data points and obscuring others. I’m going to be working through the revised numbers over the next 24 hours or so, and will be issuing my quarterly deck for subscribers once the 10-Q report is out, as that’ll fill in some gaps in the current data. I may well do another post on the earnings at that point too.

ASPs

I tweeted about the iPhone ASPs as follows shortly after the numbers came out:

Holy cow – iPhone ASPs: pic.twitter.com/GsYTHTdeJZ

— Jan Dawson (@jandawson) January 27, 2015

In some ways, that about sums it up. But of course that chart shows two sets of ASPs, going in dramatically different directions (as I indicated they would in my Techpinions earnings preview post on Monday):

- iPhone ASPs rose in Q3, but even more dramatically in Q4, largely thanks to two things: the iPhone 6 Plus, which raised the base price of the top-end iPhone model by $100, and the introduction of a 128GB model, which raised the top-end price as well. The combination of these two conspired to lift ASPs $50 above last year’s number.

- iPad ASPs continue to fall, on a fairly predictable slope, over the last few quarters, enabled conversely by a lowering of the entry price for iPads.

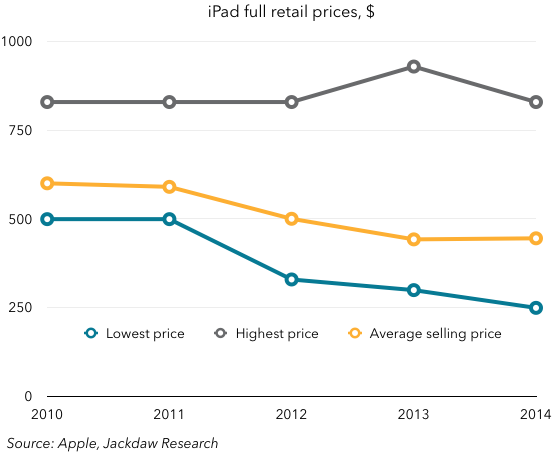

The two charts below show the pricing moves behind those ASP trends:

As you can see, the lowest price for iPhones has remained very stable for four years, while the highest possible price has risen $200 since 2010. But the iPad’s lowest selling price has fallen from $500 to $250 during that same period, while the highest price has barely changed. Given the lack of subsidies on the iPad, lower full retail prices translate directly to what consumers actually pay, whereas higher prices on the iPhone side are masked by carrier subsidies and/or installment plans in many cases. All this helps to explain why the iPhone ASP keeps rising while the iPad ASP keeps falling.

As you can see, the lowest price for iPhones has remained very stable for four years, while the highest possible price has risen $200 since 2010. But the iPad’s lowest selling price has fallen from $500 to $250 during that same period, while the highest price has barely changed. Given the lack of subsidies on the iPad, lower full retail prices translate directly to what consumers actually pay, whereas higher prices on the iPhone side are masked by carrier subsidies and/or installment plans in many cases. All this helps to explain why the iPhone ASP keeps rising while the iPad ASP keeps falling.

Retail’s varying importance in different geographies

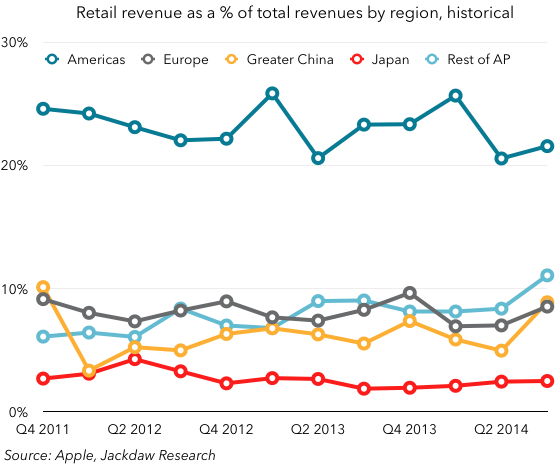

Apple giveth and Apple taketh away when it comes to financial reporting. This quarter, Apple took away all visibility over the current quarter’s retail finances, as it rolled retail reporting into regional reporting. However, in so doing, it provided a wonderful insight into past retail performance on a region-by-region basis, something we’ve never had before. I’m curious to see whether it provides any retail-related financials in its 10-Q, but for now we’ll have to make do with this interesting data set. I’ve taken that historical data and generated the following chart, which shows retail revenues as a percentage of total revenues on a regional basis:

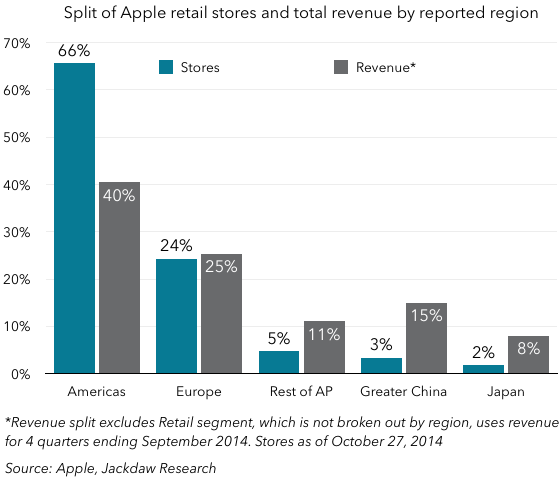

There’s obviously a huge variability by region, and this reflects a factor I’ve documented in the past. Here’s the old-style revenue split by region vs. the number of retail stores by region, which highlights the regions which have fewer retail stores than their revenue contribution would suggest:

There’s obviously a huge variability by region, and this reflects a factor I’ve documented in the past. Here’s the old-style revenue split by region vs. the number of retail stores by region, which highlights the regions which have fewer retail stores than their revenue contribution would suggest:

As you can see, the regions with the smallest percentage of revenue from retail are the same as those with the smallest number of retail stores relative to their overall revenue contribution, so this isn’t a big surprise. Japan comes bottom on both metrics. The next question is which of these two factors is the cause and which is the effect, given that there’s clearly a correlation. I suspect there’s some of each, but it’s also clear why Apple is investing so heavily in retail stores in China. It’s also clear why Apple is adding so many more retail stores outside the US than inside it (though that trend reversed a little in the last two quarters).

As you can see, the regions with the smallest percentage of revenue from retail are the same as those with the smallest number of retail stores relative to their overall revenue contribution, so this isn’t a big surprise. Japan comes bottom on both metrics. The next question is which of these two factors is the cause and which is the effect, given that there’s clearly a correlation. I suspect there’s some of each, but it’s also clear why Apple is investing so heavily in retail stores in China. It’s also clear why Apple is adding so many more retail stores outside the US than inside it (though that trend reversed a little in the last two quarters).

Growth remarkably diversified by region

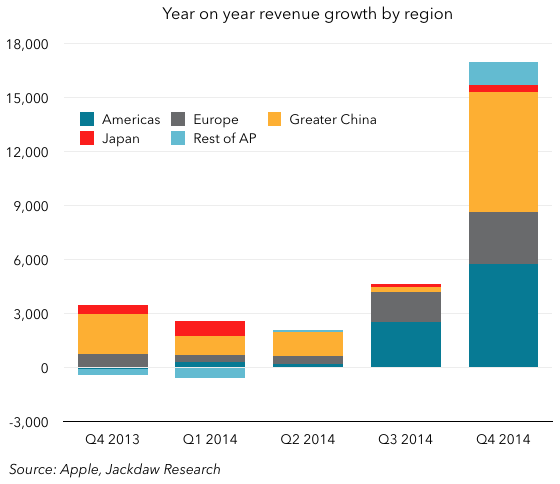

One last data point: Apple’s growth this past quarter was amazingly widespread by region. Over the last five quarters Apple’s gone from pretty low overall growth back to roaring growth on a year over year basis. In some of those past quarters, one or two regions carried much of the overall growth, whether Japan for a couple of quarters last year, or China during almost all quarters. But this quarter was notable for just how broad-based that growth was by region, with every region but Japan making a pretty meaningful contribution to overall growth (and Japan suffering from tough comparisons with a very strong quarter a year ago rather than any poor underlying performance):

Apple provided some numbers around this on the earnings call, citing 22% revenue growth in developed countries, 58% revenue growth in emerging markets as a whole, but 70% revenue growth in China year on year. Unit shipments grew by an astonishing amount in the BRIC countries as a while too – I’m not 100% sure of the number but I believe it was 90%.

Apple provided some numbers around this on the earnings call, citing 22% revenue growth in developed countries, 58% revenue growth in emerging markets as a whole, but 70% revenue growth in China year on year. Unit shipments grew by an astonishing amount in the BRIC countries as a while too – I’m not 100% sure of the number but I believe it was 90%.

Divergent fortunes for Apple and other major phone makers

As I said, I hope to have more top-line analysis later on, but for now I’ll end with this thought: the contrast between Apple’s and most other phone makers’ numbers couldn’t be starker, perhaps most dramatically as it relates to Samsung: record-high shipments at record-high prices, generating record-high profits, just as other vendors are seeing ASPs plunge, shipments stall and and margins squeezed. There’s been so much skepticism for so many years about Apple’s ability to continue to make its unique business model work over the long term, and Apple continues to prove them wrong. I believe with the launch of the Apple Watch in April, HomeKit devices finally starting to ship in significant numbers in the coming months, CarPlay, Apple Pay and who knows what else that might arrive in 2015, Apple is simply reinforcing what’s becoming an incredibly strong, sticky, and growing ecosystem.