This is mostly a Facebook earnings post in disguise – part of my series on major tech companies’ earnings. Google reports this afternoon and it’s my hope to get this out before their results hit the wires. I did a big deck full of charts and comparisons for Facebook for subscribers – sign up or read more about that offering here.

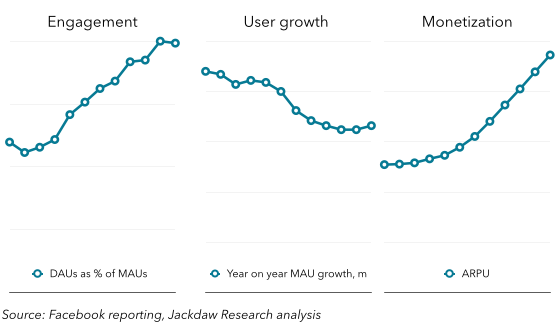

Google and Facebook are the two largest online advertising businesses in the US, and as such face similar market conditions. But they’re coming from very different places, while managing the challenges in very different ways. I maintain that the best way to look at Facebook’s growth potential (and Twitter’s, incidentally) is through three key metrics:

- User growth: measured in growth in monthly active users (MAUs) year on year

- Engagement: growth in DAUs as a % of MAUs

- Monetization: growth in average revenue per user.

The chart below summarizes the state of affairs with regard to Facebook according to these three metrics:

As you can see, two of the three look very healthy over the longer term, with engagement growing steadily and monetization increasing rapidly. User growth has slowed a little from past rates, but Facebook still adds over 150 million new MAUs every year, and the number’s actually begun to tick up slightly. Engagement stalled a bit this past quarter, as DAUs appeared to plateau at 64%. That was driven by slight declines in Asia and the Rest of World segment, along with flat numbers elsewhere. But it’s a one-quarter phenomenon for now, so we shouldn’t get overly worked up about it. We’ll see what happens next quarter. Engagement is, at any rate, merely a means to an end, as one of two drivers of monetization, which is doing fine. In short, Facebook’s core levers for growth are going well.

As you can see, two of the three look very healthy over the longer term, with engagement growing steadily and monetization increasing rapidly. User growth has slowed a little from past rates, but Facebook still adds over 150 million new MAUs every year, and the number’s actually begun to tick up slightly. Engagement stalled a bit this past quarter, as DAUs appeared to plateau at 64%. That was driven by slight declines in Asia and the Rest of World segment, along with flat numbers elsewhere. But it’s a one-quarter phenomenon for now, so we shouldn’t get overly worked up about it. We’ll see what happens next quarter. Engagement is, at any rate, merely a means to an end, as one of two drivers of monetization, which is doing fine. In short, Facebook’s core levers for growth are going well.

At the same time, this can’t go on forever:

- Facebook’s user growth can’t keep going at the same rate forever – almost all services eventually start reaching saturation of the addressable market, and with 60% penetration of the total population and 75% penetration of the mobile population in the US and Canada, it’s already bumping up against a ceiling in some regions. Elsewhere, notably in Asia, penetration remains low, but isn’t growing rapidly either.

- Engagement can’t keep going up forever either – some users will always be occasional rather than regular visitors to Facebook’s properties, and they can only spend so much time on the core Facebook experience in a day.

- Monetization will start to slow eventually too – both the limits to overall ad spend and increasing competition from other companies in mobile advertising generally and app-install ads specifically will start to eat into Facebook’s growth prospects.

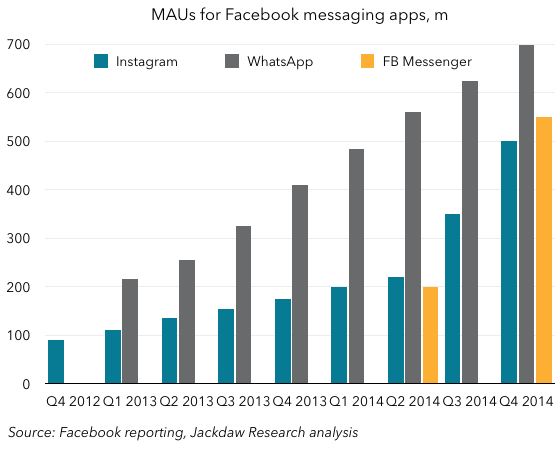

I believe Facebook is aware of all these things, which is why it’s invested in several new businesses, among them WhatsApp and Instagram in the messaging/photo sharing space and Oculus Rift in the interfaces business. It’s also broken Facebook Messenger out as a separate service, which has been controversial but seems to have paid off in spades. Here are the user numbers for the three messaging apps:

None of these is generating significant revenue today, but as Mark Zuckerberg said on yesterday’s earnings call, they all have potential to to do so in future, and Facebook will be very careful about turning the profit spigot on for each of them in the meantime. In other words, Facebook has invested for the future, and has several products waiting in the wings which can start to generate additional revenue (mostly through advertising though potentially through payments or other streams) when they’re needed to shore up overall growth.

None of these is generating significant revenue today, but as Mark Zuckerberg said on yesterday’s earnings call, they all have potential to to do so in future, and Facebook will be very careful about turning the profit spigot on for each of them in the meantime. In other words, Facebook has invested for the future, and has several products waiting in the wings which can start to generate additional revenue (mostly through advertising though potentially through payments or other streams) when they’re needed to shore up overall growth.

Perhaps the most heartening thing about Facebook, though, is that it’s been so clear about two things: the strategy behind these products, and the metrics associated with them. The underlying drivers behind both Facebook’s business today and its business tomorrow are clear for all to see, and we’ve just looked at them. You can draw different conclusions about where those trends might be going longer term, but at least you’re looking at the same data Facebook is looking at as an outsider, and especially as an investor.

This is where Google comes in. I’ve written elsewhere, and especially in a couple of recent pieces on Techpinions, about the fundamental risks to Google’s business in the near term. But I’m more worried than anything else about the fact that Google (a) doesn’t provide good enough transparency into the drivers of its current business, and (b) hasn’t articulated a clear vision for how and when its equivalent investments for the future will pay off. It is neither providing outsiders (including investors) with the understanding they need of how its current business will develop, nor is it telling a compelling story about how its business will evolve over time.

Meanwhile, there are significant headwinds coming up for Google: despite its efforts to shore up its control of Android, it’s arguably in greater danger than ever of losing control over this core platform. Between Chinese OEMs, Amazon and Samsung each customizing the platform to meet their own needs, Cyanogen threatening to take it away, and Microsoft investing in Cyanogen, there are several threats to Google’s ability to continue to control and drive revenue through Android. Internet growth is slowing worldwide, and the new users who come online will have and command far less spending power, while gravitating towards local alternatives and app rather than web models in their usage. Google really doesn’t seem to have an answer for any of these. So far, their earnings are holding up (we’ll see what happens today), but I think it’s only a matter of time before these cracks begin to show.

For those interested, below is a screenshot of the Facebook deck, with some of the metrics described above and many others. Again, click here to find out more or to sign up.