I’m kicking off the Q1 2015 earnings season (past earnings posts here) with a post on Netflix, just as I did last quarter. I’ll also be doing an updated deck for subscribers to the Jackdaw Research Quarterly Decks service. Having done a pretty broad run-down last time around, I’m going to focus on three things this time around:

- Subscriber growth, especially in the domestic streaming business

- Profitability of the US streaming business

- Profitability of the other two businesses.

Subscriber growth in the US becomes ever more cyclical

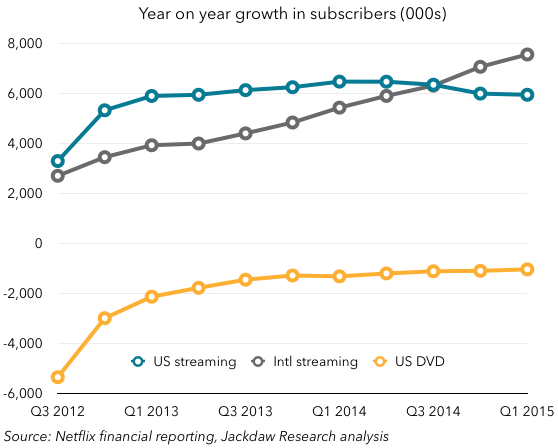

As I said last time around, subscriber growth in the US is likely to slow down over time as the service reaches later adopters and much of the lower-hanging fruit is already harvested. However, Netflix had a really good quarter for net additions in Q1, and year on year additions were flattish compared to last quarter rather than down dramatically too:

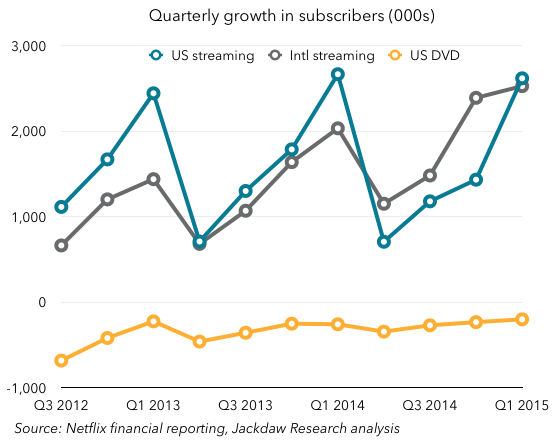

So what happened? Was I wrong about the long-term trend? Actually, no. What’s happening is that Netflix’s domestic subscriber growth in particular is becoming increasingly cyclical, driven heavily by new series launches in Q1 and lower in every other quarter. This is easier to see in this quarterly chart showing just US streaming subscriber growth:

So what happened? Was I wrong about the long-term trend? Actually, no. What’s happening is that Netflix’s domestic subscriber growth in particular is becoming increasingly cyclical, driven heavily by new series launches in Q1 and lower in every other quarter. This is easier to see in this quarterly chart showing just US streaming subscriber growth:

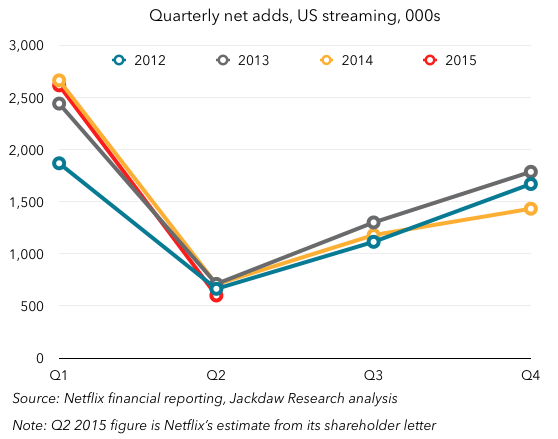

As you can see, Q1 2014 was higher than Q1 2013, which in turn was higher than Q1 2012, so there was year on year growth in Q1 every year, emphasizing the increasing importance of this quarter to Netflix’s business. You’ll note that back in 2012 Q4 and Q1 were very similar. Conversely, later quarters in the year have been sagging somewhat: though Q1 2014 was the highest ever for growth, Q2 and Q3 were only second highest, and Q4 was third. Even as Q1 becomes ever better for subscriber growth, the other quarters are showing all the effects of the long-term slowdown. Interestingly, 2015, shown in red, was lower than Q1 2014 and is forecast by Netflix to be the lowest-growth year in four years in Q2. One big question is whether Netflix’s significant slate of Originals planned for later this year can help to change this trend – it’s clearly not expecting that it will in Q2.

As you can see, Q1 2014 was higher than Q1 2013, which in turn was higher than Q1 2012, so there was year on year growth in Q1 every year, emphasizing the increasing importance of this quarter to Netflix’s business. You’ll note that back in 2012 Q4 and Q1 were very similar. Conversely, later quarters in the year have been sagging somewhat: though Q1 2014 was the highest ever for growth, Q2 and Q3 were only second highest, and Q4 was third. Even as Q1 becomes ever better for subscriber growth, the other quarters are showing all the effects of the long-term slowdown. Interestingly, 2015, shown in red, was lower than Q1 2014 and is forecast by Netflix to be the lowest-growth year in four years in Q2. One big question is whether Netflix’s significant slate of Originals planned for later this year can help to change this trend – it’s clearly not expecting that it will in Q2.

US streaming profitability continues to rise

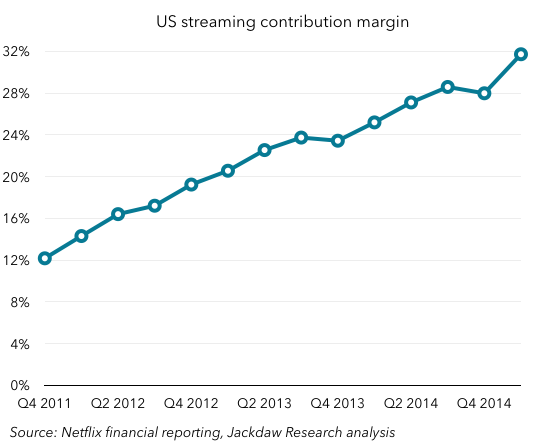

I remarked last time about the fact that Netflix is unique in that it has a public margin target for the year 2020, and the reason it’s able to do so is in large part that there are some very predictable upward trends in the domestic business (Q1 was unexpectedly better than Netflix expected because of higher subscriber adds and lower content costs):

That’s a really nice straight line, with only a couple of blips in it, and one big reason it looks like that is that another line is going steadily downwards. That’s the cost of those revenues – mostly in content and to a lesser extent streaming infrastructure:

That’s a really nice straight line, with only a couple of blips in it, and one big reason it looks like that is that another line is going steadily downwards. That’s the cost of those revenues – mostly in content and to a lesser extent streaming infrastructure:

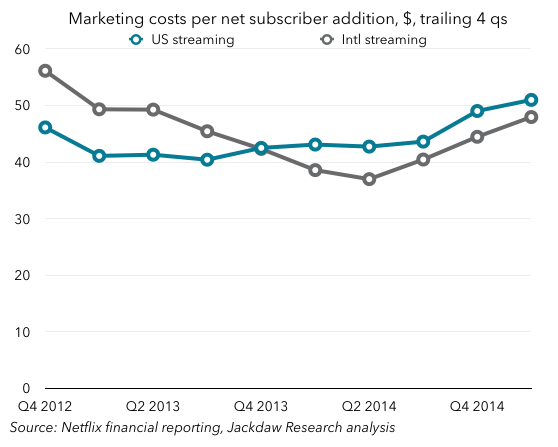

Since this cost keeps trending downwards, Netflix’s domestic streaming gross margin keeps going up. But one of the biggest secondary costs is marketing, which has actually been going up a bit, especially when you look at it on a per-net-add basis:

Since this cost keeps trending downwards, Netflix’s domestic streaming gross margin keeps going up. But one of the biggest secondary costs is marketing, which has actually been going up a bit, especially when you look at it on a per-net-add basis:

As you can see, this was the second successive quarter when Netflix’s annualized cost per net addition has risen. As I said last quarter, when growth is slowing, it costs more to acquire each new subscriber. Interestingly, though, Netflix signaled in its shareholder letter a shift in its marketing spend starting in Q2:

As you can see, this was the second successive quarter when Netflix’s annualized cost per net addition has risen. As I said last quarter, when growth is slowing, it costs more to acquire each new subscriber. Interestingly, though, Netflix signaled in its shareholder letter a shift in its marketing spend starting in Q2:

In addition, starting in Q2 we intend to shift some of our US marketing budget to international to take advantage of the substantial available growth opportunities. This, in the short term, drives down international contribution profits and drives up US contribution profits.

In other words, despite the fact that it has to work harder to acquire new subs in the US, it’s actually going to dial back spending there in favor of the rest of the world. As you can see from that chart above, it’s actually cheaper to acquire new subs there anyway, which makes sense given the much earlier stage in the market, offset slightly by the lack of familiarity with Netflix. All this will actually accelerate the positive margin trend in the US, but it may impact growth if Netflix doesn’t bring some of the marketing spend back by Q4 this year and especially Q1 next year, which as we’ve already seen are the two big quarters domestically.

US DVD and International streaming profitability

The US DVD business continues to be a wonderful example of a cash cow, throwing off great margins even as Netflix spends literally no money marketing it, simply by harvesting existing subscribers who spend an average of over $10 per month. In some ways, though, an interesting way to look at the US DVD business is that it’s essentially funding Netflix’s international expansion. Below are revenues and then contribution profit for these two segments:

As you can see, the international expansion took a while to begin to offset the decline in revenues from the domestic DVD business, but now more than makes up for it, helping to drive overall growth beyond domestic growth alone. However, the DVD business returns the favor when it comes to contribution profit, where the domestic DVD business more than offsets the losses from the international streaming business (the red line in the chart above shows the net contribution profit from these two businesses combined). It’s been a bit tight recently, but that line has never dipped below zero. In other words, the domestic DVD business is phenomenal not only in its own right, but especially because it allows Netflix to expand internationally without dragging down overall profitability, and essentially allowing much of that steadily increasing profitability in the domestic streaming business to flow through to the bottom line.

As you can see, the international expansion took a while to begin to offset the decline in revenues from the domestic DVD business, but now more than makes up for it, helping to drive overall growth beyond domestic growth alone. However, the DVD business returns the favor when it comes to contribution profit, where the domestic DVD business more than offsets the losses from the international streaming business (the red line in the chart above shows the net contribution profit from these two businesses combined). It’s been a bit tight recently, but that line has never dipped below zero. In other words, the domestic DVD business is phenomenal not only in its own right, but especially because it allows Netflix to expand internationally without dragging down overall profitability, and essentially allowing much of that steadily increasing profitability in the domestic streaming business to flow through to the bottom line.