Verizon reported results this morning. In listening to the call and reviewing some of my numbers, I was struck my the fact that Verizon is in the midst of several important transitions. I’ll highlight three here today:

- Converting the phone base to smartphones

- Converting the phone base to installment billing

- Converting broadband subs to FiOS

Each of these three transitions is largely about moving a portion of Verizon’s base from one thing to another, rather than about growth per se, but each has a financial impact, and two of the three are accompanied by new growth opportunities.

Converting the phone base to smartphones

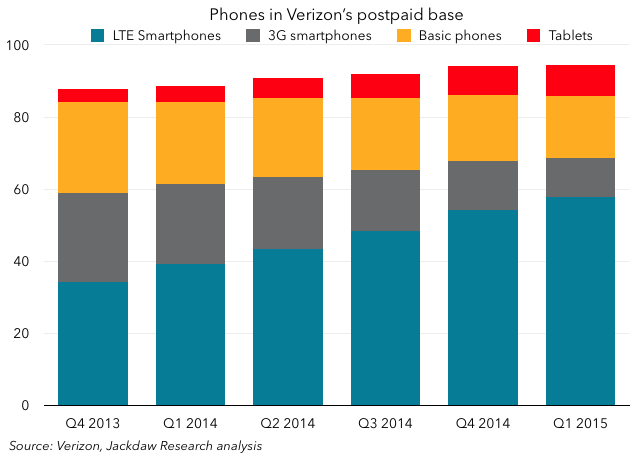

The first transition is converting the phone base to smartphones, and specifically to 4G LTE smartphones. Here’s what that process looks like at Verizon Wireless:

As you can see, the total number of phones isn’t really growing much (in fact, Verizon lost phone customers in Q1). But smartphones within the base, and especially 4G smartphones, are growing very rapidly. The financial impact here is that smartphone owners, and 4G smartphone owners in particular, consume lots more data. In a world where almost every plan includes unlimited text and voice, the path to growth from these customers is increasing data usage, and getting them on a 4G smartphone is the best way to do that. This growth opportunity will last for another couple of years at least – there are still 11 million 3G smartphones and 17 million basic phones in the base to convert. But at some point it will come to an end.

As you can see, the total number of phones isn’t really growing much (in fact, Verizon lost phone customers in Q1). But smartphones within the base, and especially 4G smartphones, are growing very rapidly. The financial impact here is that smartphone owners, and 4G smartphone owners in particular, consume lots more data. In a world where almost every plan includes unlimited text and voice, the path to growth from these customers is increasing data usage, and getting them on a 4G smartphone is the best way to do that. This growth opportunity will last for another couple of years at least – there are still 11 million 3G smartphones and 17 million basic phones in the base to convert. But at some point it will come to an end.

The good thing is that Verizon has done better than any of the other carriers in driving adoption of another set of devices: tablets. If we add tablets to the chart we can put this in context:

As you can see, Verizon’s tablet base is a useful additional source of subscriptions, with 8.8m in use at the end of Q1. Tablets and other non-phone devices will be critical to long-term growth as phone growth is almost non-existent and the vast majority of the base will be on smartphones before long. AT&T is currently the US market leader in connected devices – subscriptions driven by things like connected cars and machine-to-machine services – but Verizon is building this business up too.

As you can see, Verizon’s tablet base is a useful additional source of subscriptions, with 8.8m in use at the end of Q1. Tablets and other non-phone devices will be critical to long-term growth as phone growth is almost non-existent and the vast majority of the base will be on smartphones before long. AT&T is currently the US market leader in connected devices – subscriptions driven by things like connected cars and machine-to-machine services – but Verizon is building this business up too.

Conversion to installment billing

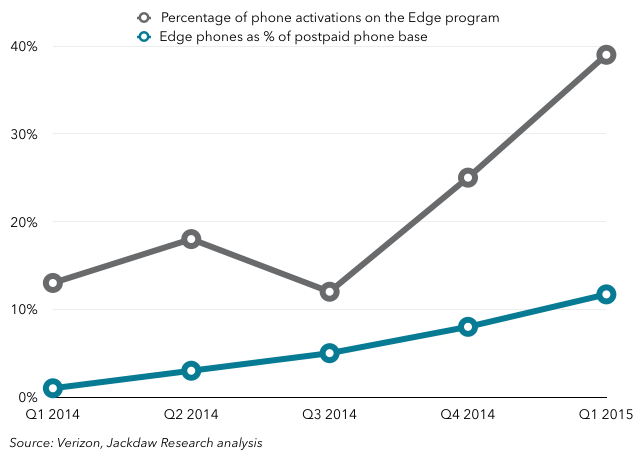

The second transition I want to cover is the switch all of the US carriers are going through with regard to how customers pay for their devices. The traditional model in the US has been a subsidy model, under which customers paid only a fraction of the true cost of their devices and the carrier recouped the rest in an opaque fashion through service fees. The new model, which Verizon has been slowest to embrace among the major US carriers but is now actively driving, sees customers paying for their devices in installments. Verizon’s installment program is called Edge, and the chart below shows the percentage of devices sold and the percentage of phones in the base on this plan for the last few quarters:

As you can see, the percentage of phones sold (”phone activations”) on the Edge plan is skyrocketing from just over 10% a year ago to almost 40% this quarter (and management said on the call that it’s now at almost 50%). It takes a while for that to drive meaningful change in the base, but you can see that in Q1 Verizon crossed 10% for the first time, and that number will rise rapidly going forward.

As you can see, the percentage of phones sold (”phone activations”) on the Edge plan is skyrocketing from just over 10% a year ago to almost 40% this quarter (and management said on the call that it’s now at almost 50%). It takes a while for that to drive meaningful change in the base, but you can see that in Q1 Verizon crossed 10% for the first time, and that number will rise rapidly going forward.

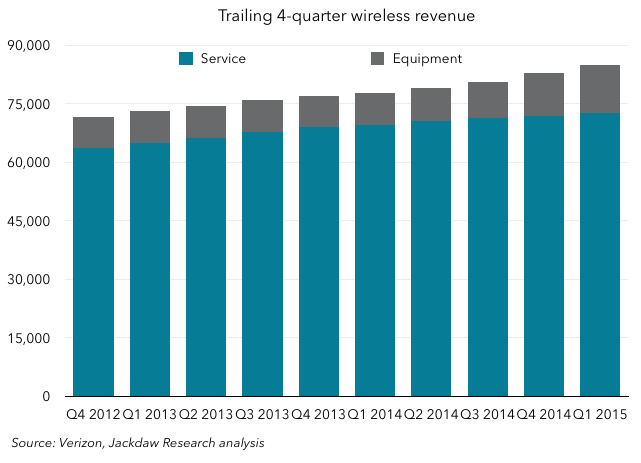

The financial impact of this transition is more complex – at a basic level, it takes some revenue that would have historically been classified as service revenue and moves it into the equipment revenue bucket. You can see the impact of this trend over time here:

This quarter, service revenue actually fell year on year for the first time, but that’s just because of this transition. Unfortunately, it makes a number of other traditional metrics like average revenue per user or per account (which are based on service revenue alone) less meaningful, because they no longer capture the entire revenue stream. Verizon has provided a different metric in recent quarters to account for this – ARPA plus Edge billings – but failed to do so this quarter, at least in the materials released today. The broader financial impact is more complex – there’s a set of receivables associated with these installment billings which some of the carriers are seeking to sell off in the financial markets, and they have complex impacts on margins too.

This quarter, service revenue actually fell year on year for the first time, but that’s just because of this transition. Unfortunately, it makes a number of other traditional metrics like average revenue per user or per account (which are based on service revenue alone) less meaningful, because they no longer capture the entire revenue stream. Verizon has provided a different metric in recent quarters to account for this – ARPA plus Edge billings – but failed to do so this quarter, at least in the materials released today. The broader financial impact is more complex – there’s a set of receivables associated with these installment billings which some of the carriers are seeking to sell off in the financial markets, and they have complex impacts on margins too.

Conversion of the broadband base to FiOS

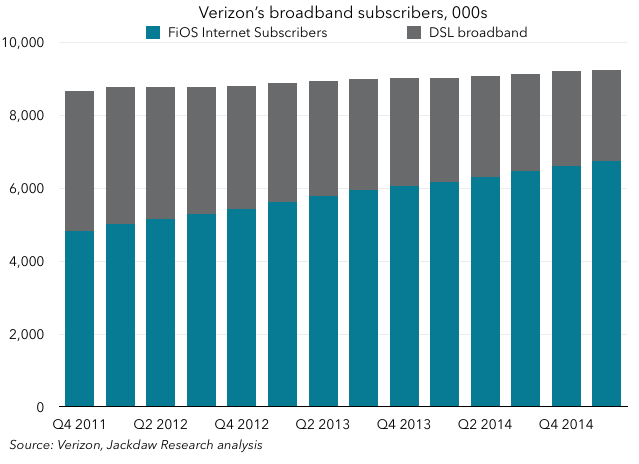

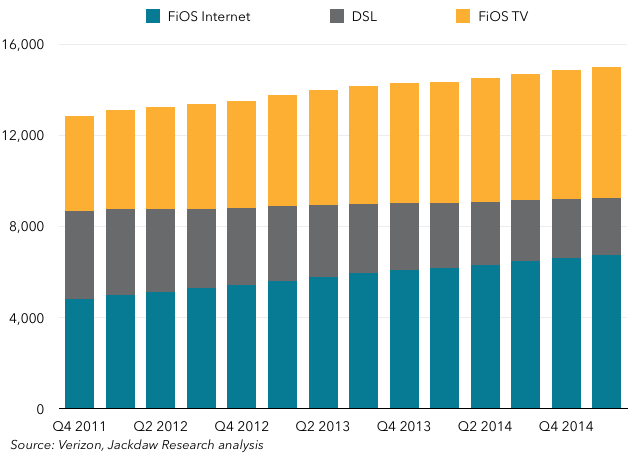

The last transition I want to talk about is the conversion of Verizon’s traditional DSL-based broadband base to its FiOS fiber broadband service. FiOS has become the major focus of Verizon’s landline activities, and it’s been slowly selling off portions of its landline business where providing FiOS isn’t practical. It’s now planning to sell off three “islands” within its wireline business that don’t connect with its otherwise contiguous service area in the Northeast: Florida, Texas, and California. With the focus on FiOS, the key is to convert as much of the base as possible to this technology, to enable the decommissioning of the copper network and to drive higher revenues. Here’s how that transition is going:

In some ways, that chart looks a lot like the smartphone transition chart I showed above – there is some growth in the overall base, but the major trend is the conversion from one technology to another, with the associated benefits for Verizon and its customers. One of the major benefits of the switch to FiOS is that it enables another major revenue stream: TV. Though the broadband base isn’t growing much, adding TV to the mix is a significant benefit from a revenue and customer stickiness perspective. I’ve layered FiOS TV subs onto the chart, though you should not that there’s very significant overlap between the FiOS broadband and TV bases:

In some ways, that chart looks a lot like the smartphone transition chart I showed above – there is some growth in the overall base, but the major trend is the conversion from one technology to another, with the associated benefits for Verizon and its customers. One of the major benefits of the switch to FiOS is that it enables another major revenue stream: TV. Though the broadband base isn’t growing much, adding TV to the mix is a significant benefit from a revenue and customer stickiness perspective. I’ve layered FiOS TV subs onto the chart, though you should not that there’s very significant overlap between the FiOS broadband and TV bases:

As you can see, that FiOS TV base is expanding rapidly, and at around $100 per month per subscriber, it’s a very useful additional revenue stream. However, it’s worth noting that this revenue is lower margin revenue than broadband, because much of the revenue is passed through to cable networks and broadcasters. Verizon sees broadband as the key product in the home, and as such its major focus is driving broadband usage, in contrast to AT&T, which sees TV as the anchor product. This is partly a reflection of their respective broadband networks – Verizon’s is largely unmatched in the areas where it operates because it’s the only fiber to the home network, whereas AT&T’s is less competitive. But it also explains why Verizon is investing in an over-the-top (OTT) video service to launch in the summer, and in back-end infrastructure for video delivery through its Verizon Digital Media Services unit.

As you can see, that FiOS TV base is expanding rapidly, and at around $100 per month per subscriber, it’s a very useful additional revenue stream. However, it’s worth noting that this revenue is lower margin revenue than broadband, because much of the revenue is passed through to cable networks and broadcasters. Verizon sees broadband as the key product in the home, and as such its major focus is driving broadband usage, in contrast to AT&T, which sees TV as the anchor product. This is partly a reflection of their respective broadband networks – Verizon’s is largely unmatched in the areas where it operates because it’s the only fiber to the home network, whereas AT&T’s is less competitive. But it also explains why Verizon is investing in an over-the-top (OTT) video service to launch in the summer, and in back-end infrastructure for video delivery through its Verizon Digital Media Services unit.