Twitter’s earnings last night were something of a mess. Revenue fell short of the company’s forecasts, user growth was nothing special, two previous metrics were retired and two new ones introduced which don’t look great right now, and to top it off, the earnings report was accidentally posted before the market closed. Last quarter, I said this about Twitter’s results:

…there are three main growth drivers for [companies like Twitter]: user growth, increased engagement, and better monetization of that engagement. Twitter’s problem continues to be that only one of these three is going in the right direction… User growth has been slowing significantly over the past two years, and especially over the last few quarters. This quarter the company added just 4 million MAUs (or 8 if you’re charitable and give them back the 4 million additional MAUs they claim they lost to an iOS 8 bug). Even at 8 million, that’s by far the slowest growth in several years. Engagement, meanwhile, as measured by timeline views per MAU, has also been stagnant or falling for several quarters. The only metric moving in the right direction is monetization, and boy is it moving in the right direction!

I’ve often used these three metrics – user growth, engagement, and monetization – as a framework for evaluating Twitter’s earnings, and in Q4, only one was moving in the right direction. In Q1, however, even monetization stumbled, leaving the company without a single improving metric among the three. Let’s quickly review the key metrics here.

User growth: nothing special, with worse to come

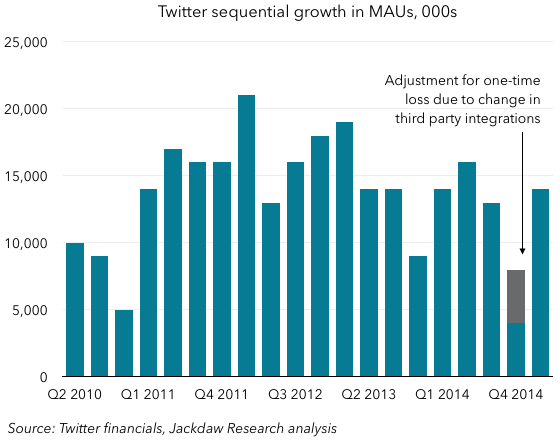

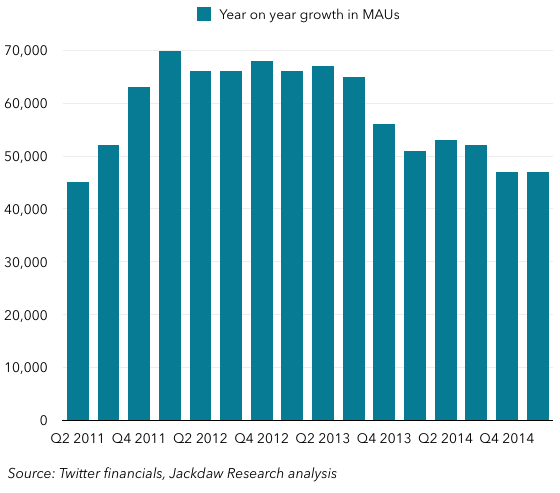

Twitter’s user growth numbers rebounded a bit in Q1 from Q4, but they really weren’t fantastic. Here’s sequential and year on year growth in monthly active users:

As you can see, neither of these was spectacular by any means. On a sequential basis, MAU growth rebounded a bit from the terrible Q4 numbers, but was still lower than several quarters in the last few years. On a year on year basis, it matched Q4 as the lowest since early 2011. Because of this, Twitter has been trying for several quarters to get the financial community to take a broader view of users, first focusing on “logged out users” (those who visit the site but don’t have accounts, or don’t bother logging into them) and now “SMS Fast Followers” – those who signed up for Twitter via SMS and still only use it in that way. However, both of these sets of users have dramatically lower potential for monetization, and although Twitter is quantifying the SMS group (very small today at 6 million), it still isn’t providing good numbers for the logged-out user group.

As you can see, neither of these was spectacular by any means. On a sequential basis, MAU growth rebounded a bit from the terrible Q4 numbers, but was still lower than several quarters in the last few years. On a year on year basis, it matched Q4 as the lowest since early 2011. Because of this, Twitter has been trying for several quarters to get the financial community to take a broader view of users, first focusing on “logged out users” (those who visit the site but don’t have accounts, or don’t bother logging into them) and now “SMS Fast Followers” – those who signed up for Twitter via SMS and still only use it in that way. However, both of these sets of users have dramatically lower potential for monetization, and although Twitter is quantifying the SMS group (very small today at 6 million), it still isn’t providing good numbers for the logged-out user group.

Lastly, it seems Q2 results for MAU growth will be even worse than Q1, based on what Twitter is seeing so far in the quarter – from the earnings call:

[with regard to] MAUs, the 302 million monthly active users that we reported without SMS follows in Q1 was driven by growth initiatives and a return to organic and seasonal growth and we had the benefit of all those factors working for us as we delivered that number. In Q2, we are not seeing the benefit from those three factors as much and there is also some headwinds. So at this point our visibility is actually limited as it relates to Q2 MAU adds. We are off to a slow start in April and so the visibility is not as strong as it was in Q1 and the trend is not similar to Q1.

Ouch.

Engagement: the only metric vanishes

When it comes to engagement, Twitter had used “Timeline views per MAU” as the metric, but it announced in last quarter’s earnings that it would be discontinuing the reporting of this measure, because it no longer felt it would be a good measure of true engagement (and, frankly, because it wasn’t growing). I had hoped we’d get a new metric to measure user engagement this quarter, but we didn’t. And that’s problematic, because increased usage of the service and loyalty to it is key to driving revenue growth over time. Twitter’s exclusive focus on MAUs as the unit of user growth is also problematic, because it’s a poor measure of true engagement with the service. Twitter’s management was asked about this on the earnings call and had this to say:

In terms of engagement metrics, there is a lot of different metrics that we look at internally. There is not one metric for engagement. And so I can give you a sense of some of them and quite frankly, we would like to be able to give you more visibility in this, but there is just a number of different measurement. So DAU is one measurement of engagement. We talked about that at Analyst Day. It’s a measurement that is dependent by market and you can have mix shift. So it could be a little bit misleading, but DAU to MAU ratios in the quarter were similar to what they were by market relative to Analyst Day.

Other engagement metrics that we look at are tweets per day, favorites and retweets, direct messages, searches. Our number of searches actually accelerated on a year-over-year growth basis in the quarter. Direct messages also accelerated on a year-over-year basis in the quarter. Favorites and retweets had strong growth and we had growth in tweets per day as well. So those metrics all were generally positive.

The timeline view metric, we don’t look at internally. It is a metric that we are doing things that actually hurt it and that was one of the reasons why we eliminated it. So we continue to look for metrics that could be helpful to you and we will try to give you color from time to time across these different metrics. But there is not one, the all-in metric.

In other words, Twitter has lots of potential metrics they could share, but they won’t. The worst thing about this is that it smacks of a “trust us” mentality, and I think investor trust is wearing thin with Twitter at this point, especially given that other metrics are also heading in the wrong direction.

Monetization: new metrics, mixed picture

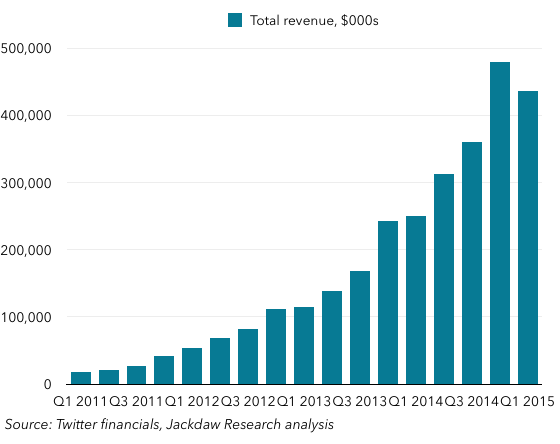

The third metric, and the only one which was looking positive last quarter, is monetization. Twitter had a massive Q4 on this basis, off the back of a huge rise in ad revenue per MAU. But Q1 was the first quarter in which Twitter suffered a sequential revenue decline:

The reason was twofold: firstly, ad revenue is always cyclical, and larger in Q4 than Q1 (Google saw the same thing this quarter, for example); but secondly, Twitter actually saw poorer than expected performance on its direct response advertising. It’s had to lower its guidance for the year off the back of that problem, and came in short of its estimates for Q1. Part of the reason was that Twitter tightened the definition of what counts as an engagement on an ad (equivalent to a click in traditional online advertising terms), which lowered the number of ads it got paid to serve. In time, Twitter hopes this will lead to higher prices per ads because advertisers find these engagements more valuable as true drivers of business.

The reason was twofold: firstly, ad revenue is always cyclical, and larger in Q4 than Q1 (Google saw the same thing this quarter, for example); but secondly, Twitter actually saw poorer than expected performance on its direct response advertising. It’s had to lower its guidance for the year off the back of that problem, and came in short of its estimates for Q1. Part of the reason was that Twitter tightened the definition of what counts as an engagement on an ad (equivalent to a click in traditional online advertising terms), which lowered the number of ads it got paid to serve. In time, Twitter hopes this will lead to higher prices per ads because advertisers find these engagements more valuable as true drivers of business.

One good way to look at this is to use the two new ad-related metrics Twitter began providing this quarter, which are similar to those reported by other online advertising businesses like Google and Yahoo. The first is growth in the number of ad engagements both sequentially and year on year. This isn’t the same as user engagement with content, but rather measures the number of ads shown to customers with which they engage in some way. As Twitter tightens the definition of an engagement, this seems to be heading in the wrong direction:

Part of this is the law of large numbers kicking in – as real numbers grow, percentage growth rates often fall. But part of it is also likely down to Twitter’s tightening of that definition. In time, the impact of that change should diminish, and this number should start growing faster again. But by using a percentage metric, Twitter risks setting itself up for a line that always looks like it’s heading downhill.

Part of this is the law of large numbers kicking in – as real numbers grow, percentage growth rates often fall. But part of it is also likely down to Twitter’s tightening of that definition. In time, the impact of that change should diminish, and this number should start growing faster again. But by using a percentage metric, Twitter risks setting itself up for a line that always looks like it’s heading downhill.

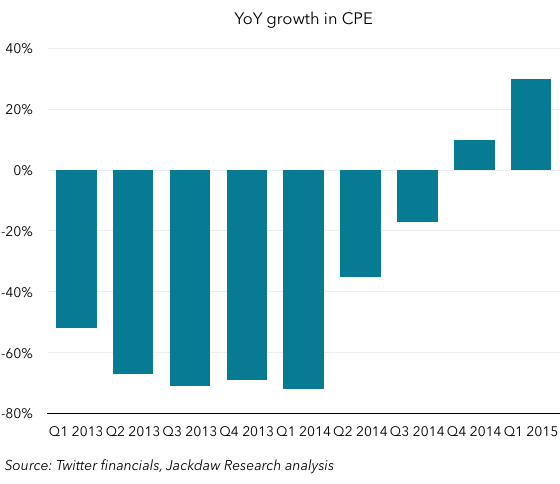

The second new metric is growth in cost per engagement (essentially, price per successful ad). Here is year on year growth: That trend certainly looks like it’s heading in the right direction, and if the strategy I just articulated works, it should continue to do so. The challenge with much of online and mobile advertising today is that there is an excess of total inventory, but a paucity of premium inventory. Prices are falling across the board, but if you isolate the premium category, prices are actually rising because demand is outstripping supply. Twitter’s shift here should help to position it in the premium category over time, if it really can deliver a higher quality engagement, and that in turn should help the monetization curve turn around.

That trend certainly looks like it’s heading in the right direction, and if the strategy I just articulated works, it should continue to do so. The challenge with much of online and mobile advertising today is that there is an excess of total inventory, but a paucity of premium inventory. Prices are falling across the board, but if you isolate the premium category, prices are actually rising because demand is outstripping supply. Twitter’s shift here should help to position it in the premium category over time, if it really can deliver a higher quality engagement, and that in turn should help the monetization curve turn around.

Twitter’s near-term future is cloudy

On balance, I continue to be somewhat bearish about Twitter’s growth prospects. Let me be clear, though: based on its current trajectory, I think it’ll get to profitability relatively soon, so I don’t think there’s any danger of it going out of business. Rather, the risk is that Twitter’s progress is capped at significantly less than its total potential, because of a combination of an inability to drive adoption beyond a relatively small base and its inability to monetize that usage effectively. On paper, I think it’s doing a lot right at the moment, with the new homepage and signup experience, Instant Timeline, and other new features. But so far these don’t seem to be translating into the kind of growth it should be seeing. And Twitter’s management seems too convinced that user value will automatically translate into significant revenue over time. It needs to do a better job of articulating exactly how those two are connected.