I wrote a piece a few days back for Techpinions about the challenges Google needed to address at I/O this year. Now that the I/O keynote is over (which I was fortunate enough to attend in person), I thought I’d revisit that list of challenges to see how Google did.

Retaking control of Android

There were a couple of things that Google did related to retaking control of Android at I/O: reinforcing the value proposition of its Android One initiative, and announcing Android Pay. The former is obvious: it’s Google’s attempt to get a close-to-stock version of Android as the default version in emerging markets. But the latter may be less obvious. However, by launching Android Pay, Google nixes its OEMs’ efforts to introduce their own payment systems, as this post outlines. Samsung is likely to be the hardest hit by this, since it’s the only Android OEM that had launched a payment service. But I wonder how much Google will spread this model of Google Services Mandatory classification for key Android features to other areas, squeezing out OEMs from offering competing services.

Defending the web against apps

This year’s I/O was a mixed bag in this respect, with a couple of initiatives clearly aimed at just this, but some others moving things in the opposite direction. On the one hand, Google announced Chrome Custom Tabs, an alternative to in-app browsers for displaying web content, which brings users back into the web, where Google can better track their activity and otherwise capture data. It also reiterated its app indexing and deep linking projects, which recently began to roll out on iOS too. These efforts are both aimed at making the web more relevant in a world where apps are becoming dominant. Google Now on Tap is an interesting mix in this respect – on the one hand, it allows users to stay in apps when they have Google Now queries, rather than having to exit out of them, which could be seen as favoring apps rather than the web. But on the other hand, this inserts a Google layer between users and apps, in some cases recommending other apps for users to open, but in others using the Google Knowledge Graph to disintermediate those apps. On balance, Google seems to be serving its own needs pretty well with these new announcements.

Convince developers Android users are worth targeting

There was remarkably little at I/O about why developers should target Android users exclusively or in addition to iOS users. There was no update on the total number of Android users, which remains at “over one billion”. And Google did very little to argue why these users might be attractive, rather emphasizing the fact that many of the new users on Android will come from emerging markets, where there are lower incomes and less propensity to spend. There was no mention of carrier billing at all, and the only mention of monetization was in relation to better ad products within apps rather than paid apps or in-app purchases. I don’t think Google has given up on the paid apps route, but it was hard to escape that impression from the keynote, which I find baffling. To be sure, Android will never have the same attractive demographics as iOS, but it can still do much better than it has in the past, especially in mature markets.

Take Android beyond personal computing devices

The big announcement here was the Brillo project, which takes Android and strips it down to a barebones version for use in Internet of Things devices (and for today at least home devices specifically), together with the Weave communication protocol, which will be baked into Android at the Google Play Services layer and therefore make compatible devices instantly discoverable from Android devices. This is exactly what I was getting at in my preview piece on this topic – a version of Android that’s optimized for these devices, which have no need for the full version of Android but have other specific needs Android in its current form doesn’t meet well. There’s a lot of work still to be done here – though Brillo will launch in Q3 (and Weave in Q4) I sensed many decisions about Brillo still haven’t been made (not least the final name for the OS itself). More broadly, I was disappointed that we didn’t hear more about operating systems for the car, another area I highlighted in my preview piece, and one in which Google has been reported to be making some interesting progress. I wonder if we’ll see more on this in the months building up to the Android M public release.

Demonstrate a clear value proposition in TV

This was the other big area where I was expecting much more from Google’s keynote at I/O than we got – it got barely a mention in the keynote, and the expected announcements were made either not at all or in press releases. Nvidia announced its Shield device built on Android TV, and bought up almost every outdoor advertising spot within a few blocks of the Moscone Center to advertise it, but there was nothing in the keynote to demonstrate meaningful progress in this area. The only other concession to this challenge was the announcement that HBO Now would be coming to Android and Chromecast shortly. Speaking of which, Chromecast has now sold 17 million units, putting it in the same ballpark with Apple TV and Roku. There continues to be an odd disconnect between Chromecast and Android TV in Google’s TV strategy which I hope it can resolve in time. Chromecast certainly seems to be the more successful model so far, though the total number of casts (1.5 billion) relative to the number of Chromecasts sold (17 million) implies relatively low usage of those devices.

Continue to unify Android and Chrome OS

There was even less on this theme at I/O 2015 than there was last year, where Google at least talked about Android apps running on Chrome OS. Chrome OS was barely mentioned at all in the keynote, and there was no news about it at all. This continues to be an area where Google has to do a much better job telling its story and bringing the disparate threads together.

Differentiate against Amazon and Microsoft in the cloud

The whole enterprise space, and cloud in particular, got incredibly short shrift in the keynote too, after a lengthy session in last year’s keynote. There was nothing here to indicate that Google was going to make meaningful progress in this department in the coming year beyond its existing strategies.

Beyond the keynote, and beyond Android

Even though the pace of the keynote and the volume of individual announcements was somewhat overwhelming, as always, the substance of what was announced really wasn’t. The Android M release looks like a very modest, incremental, improvement on Lollipop. This was a little disappointing, but partly reflects the fact that Google is slowly extracting functionality from the operating system and putting it in more easily upgradable layers like Google Play Services instead. The new Photos app is a great example of this. This does mean, however, that the news around new Android version releases is going to become less interesting over time, while the announcements separate from Android will become more interesting in many ways. But this year’s I/O also looks like introducing much more news outside the keynote – I’m writing this on day two of the event, and several announcements around wearables, Google Loon, and other projects have been made separately. As an attendee, I’m grateful that the keynote was trimmed down to just two hours, but it does make it harder to follow all the news that’s coming out of I/O as Google starts to fragment the more notable announcements across sessions.

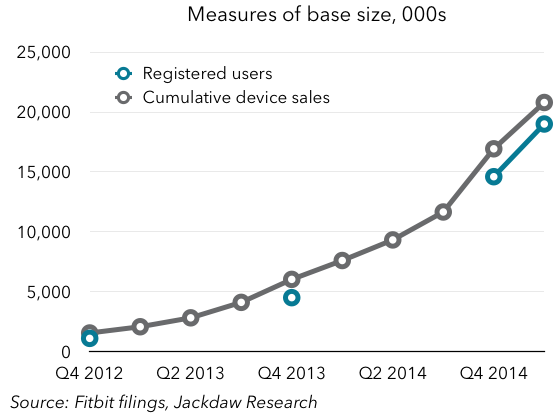

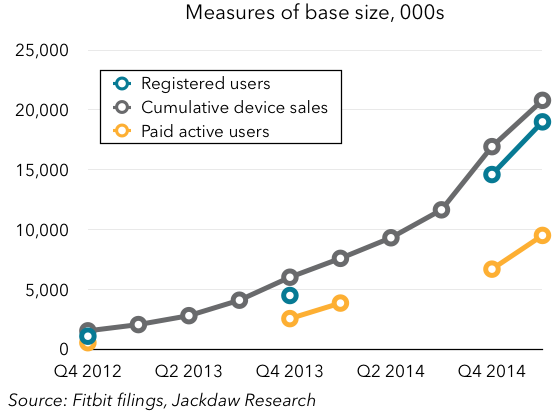

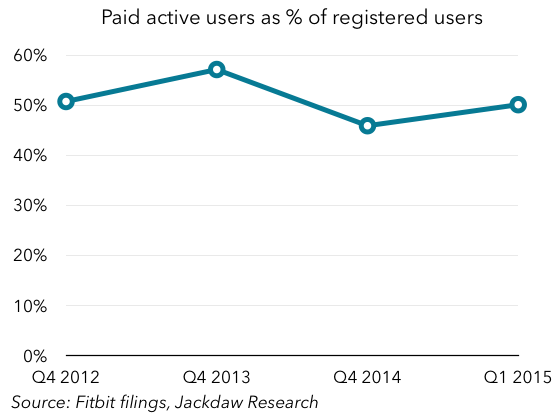

As you can see, the number of active users is far smaller than the number of registered users when added to that same chart. In the chart below, I’ve shown PAUs as a percentage of registered users at the four points in time where we have both numbers:

As you can see, the number of active users is far smaller than the number of registered users when added to that same chart. In the chart below, I’ve shown PAUs as a percentage of registered users at the four points in time where we have both numbers: The number bounces around at about 50%, rising or falling a little over time but remaining remarkably constant. In one sense, that’s obviously fairly bad news – in addition to the fact that very few Fitbit buyers purchase a second device, it would appear that half of those who bought one stop using it after a period of time. However, there’s a flip side to this, if you’re looking for a silver lining, which is that the number isn’t falling over time. In other words, over two years ago, the number was 50%, and it still is. I’m actually a bit surprised by this, because all the early abandoners should still show up in the numbers and drag the overall retention rate down, but that doesn’t seem to be happening. What’s interesting is that this correlates closely with a survey I did last year about fitness trackers. The key question here was the individual’s experience with fitness trackers:

The number bounces around at about 50%, rising or falling a little over time but remaining remarkably constant. In one sense, that’s obviously fairly bad news – in addition to the fact that very few Fitbit buyers purchase a second device, it would appear that half of those who bought one stop using it after a period of time. However, there’s a flip side to this, if you’re looking for a silver lining, which is that the number isn’t falling over time. In other words, over two years ago, the number was 50%, and it still is. I’m actually a bit surprised by this, because all the early abandoners should still show up in the numbers and drag the overall retention rate down, but that doesn’t seem to be happening. What’s interesting is that this correlates closely with a survey I did last year about fitness trackers. The key question here was the individual’s experience with fitness trackers: