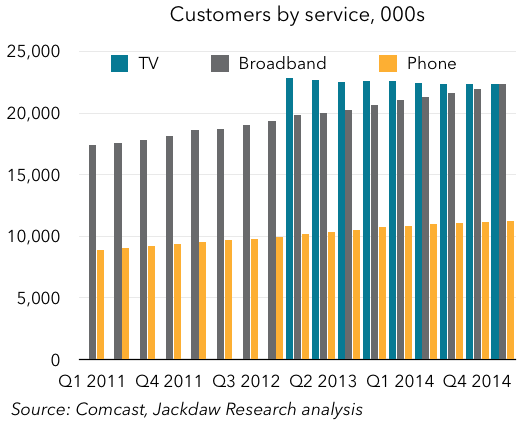

Comcast’s results today were notable for a significant transition that’s about to happen: this was likely the last time Comcast will report more TV customers than broadband customers:

As of the end of March, the two numbers were just 6,000 apart, so next quarter the two will have crossed over, and Comcast will have more broadband than TV subscribers. This is a hugely symbolic moment for a cable company, but Comcast is far from the first to make this transition – in fact it’s the last of the major public cable operators to do so:

As of the end of March, the two numbers were just 6,000 apart, so next quarter the two will have crossed over, and Comcast will have more broadband than TV subscribers. This is a hugely symbolic moment for a cable company, but Comcast is far from the first to make this transition – in fact it’s the last of the major public cable operators to do so:

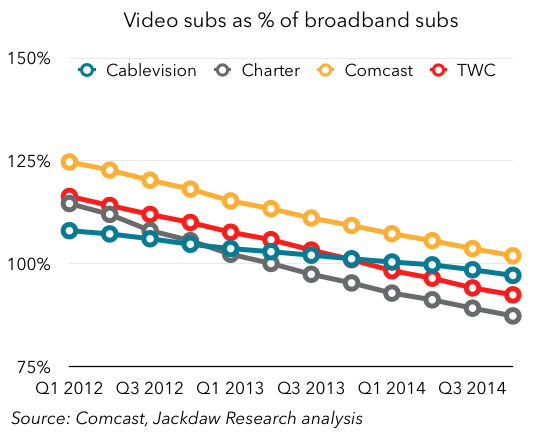

All the others crossed this line some time ago, and Comcast has been approaching this transition for some time. However, it’s important that we don’t get too caught up in the symbolism and start seeing Comcast as first and foremost a broadband company.

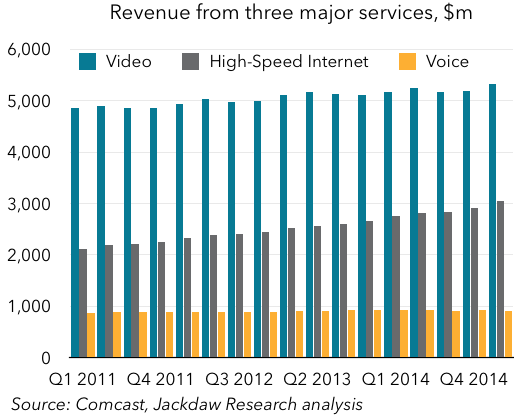

Revenues tell a very different story

Even though the subscriber line will be crossed in Q2, the picture as regards revenues is very different:

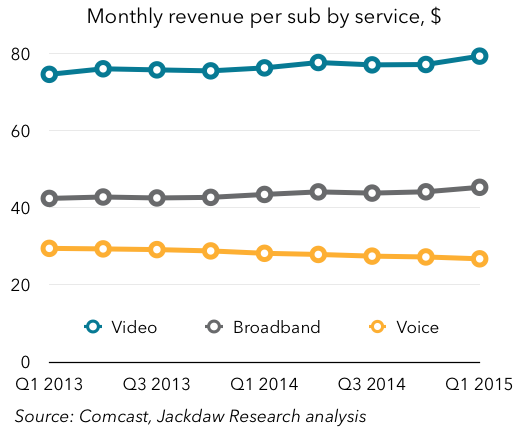

Comcast’s revenues from video are still far higher than its revenues from broadband, even as the subscribers are very similar. And that’s because the average revenue per subscriber per months is almost twice as high for TV as for broadband:

Monthly TV revenue per subscriber is about to cross the $80 mark, and is rising almost as fast as average broadband revenue. TV revenue is therefore still rising somewhat, even as TV subscribers fall. And why are TV subscribers falling? That’s largely because of competition rather than cord-cutting: the total number of pay TV subscribers in the US is staying roughly flat, with the telcos (principally AT&T and Verizon) and to a lesser extent the satellite providers making inroads into the cable TV base. So here too, it’s important not to overstate the significance of this transition.

Comcast is still adding customers, and services

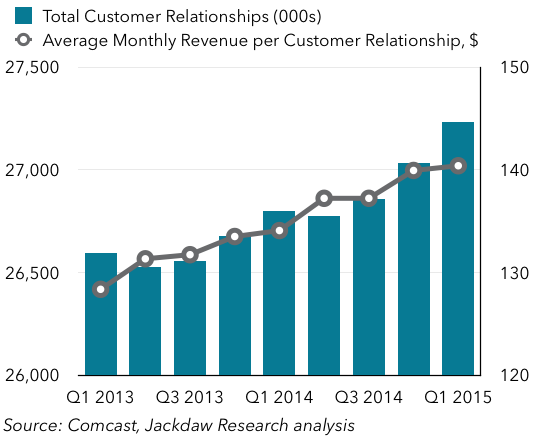

In all this, too, Comcast isn’t losing customers – some customers may not be taking TV anymore, but it’s still adding broadband customers and it’s still growing its total number of customer relationships. In addition, the total average revenue per customer relationship per month also continues to rise:

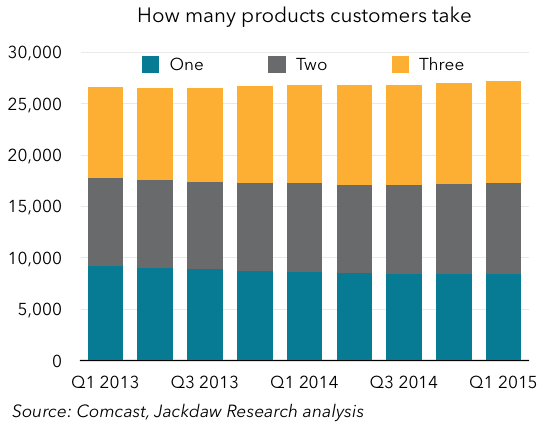

The increased revenue per service is part of this picture, but even despite the falling video numbers, Comcast’s base is still trending to more services per household over time:

It’s a subtle shift over time, but you can see the number of single-product customers falling while double- and triple-play customers continue to grow. 37% of Comcast’s customers take a triple play, up from 33% two years ago, while another 33% take two services.

The implications for cord-cutting scenarios

It’s tempting to see any sign that TV subscribers are falling as evidence of cord-cutting. As I mentioned above, though, that’s not the case with Comcast – in many cases, it’s likely that the video subscribers it’s losing are going to pay TV competitors, not cutting the cord. So should we see Comcast’s results as evidence that cord-cutting is never going to happen? Is this a lesson about the resilience of the pay TV business in the face of would-be disruptors?

The reality is that this, too, is an over-simplification. Yes, there’s absolutely evidence in Comcast’s results and in the results for the pay TV industry as a whole that TV subscribership is holding up pretty well, and this is evidence of the difficulty of disrupting the model. I think that’s at least in part because of the moves the pay TV industry has taken to embrace new forms of consumption such as TV Everywhere solutions, DVRs, video on demand and so on. Many of the things that have threatened to disrupt pay TV have simply been absorbed by it. But at the same time there are fundamental changes happening in the industry as regards viewing behavior and associated advertising revenue, and at the same time powerful new companies are entering or reported to be entering the market, including Apple. I think we might well see a scenario where the pay TV industry continues to look impervious to disruption until things very suddenly start to fall apart. At that point, it will be up to Comcast and its peers to decide whether they want to once again embrace and subsume the disruption or allow it to eat into their business.