BlackBerry reported earnings today, and as ever so much of the analysis in the mainstream news media is glossing over some of the most important details. To my mind, the most important thing in the earnings was the revenue the company announced from Software and Technology Licensing this quarter, which jumped significantly. This revenue line is the single most important element of BlackBerry’s business, and the numbers this quarter along with some of the executive commentary on the earnings call lead me to believe that the company might finally be on a trajectory to get where it needs to go to build a sustainable and growing business over time. This echoes an earlier piece I wrote, which outlined BlackBerry’s situation and the challenges it faces as it moves forward.

First, the bad news

So much of that mainstream news coverage stayed at a fairly high level, or picked up on the same old trends we’ve seen now for a couple of years, so let’s cover those at least briefly. Firstly, the hardware business is a shadow of its former self, and continues to decline, although the company has now been profitable at a gross margin level for hardware for the past year. Hardware has always been the core of BlackBerry’s business, but it simply can’t be anymore – the company doesn’t have the broad appeal to be a mass-market devices company. But those devices are still important for two fundamental reasons: BlackBerry is still the device vendor of last resort of the most regulated industries and for governments, and device revenue (and the associated service revenue – more on this below) are critical to its revenues as it works hard to grow its future revenue source: software.

The services revenue line has always been closely tied to devices, and is declining in a very predictable fashion, at around 15% or roughly $50 million per quarter:

The fact is that this decline will continue until there is almost nothing left, since this revenue line is tied to BlackBerry’s dwindling base of devices. Hardware revenue will likely stabilize in the coming months with somewhere around 1 million devices shipped per quarter, so the decline is likely mostly over there at this point.

Software finally gets a boost

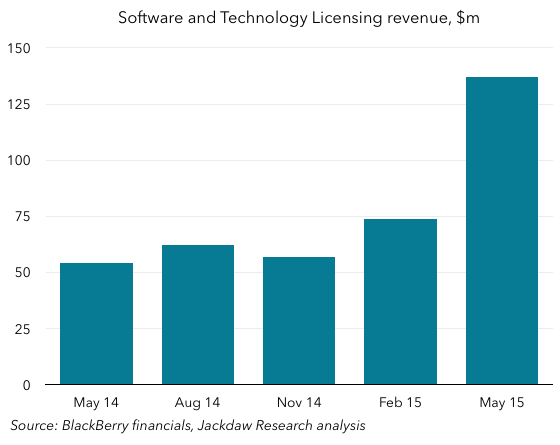

My biggest skepticism about BlackBerry’s future has come from the fact that the company set an ambitious goal of $500 million in revenue from software this year, and its run-rate has been nowhere near that, until this quarter. What changed this quarter – and dramatically at that – is that BlackBerry suddenly posted a huge boost in Software and Technology Licensing revenue. The revenue line for this segment is shown below:

You can see this line bouncing around with hardly any growth, and with a run-rate much closer to last year’s revenue of around $250 million than to the goal for next year of double that. However, it grew modestly in the February quarter and then it suddenly spiked in the quarter just reported. What’s behind this spike in revenue in this segment? Well, a lot of it came from a technology licensing deal with Cisco, which is the major reason BlackBerry renamed this revenue line from just Software in previous quarters to the new, more expansive moniker. This deal seems to have added an enormous amount to this segment’s revenues in the quarter, and also to BlackBerry’s overall North American revenues, which grew by $80 million quarter on quarter after a fairly steady decline. This deal is clearly good news for the software revenue growth story, although it’s questionable whether this is really the kind of revenue the company was talking about when it set that $500 million goal.

Understanding this deal is an exercise in frustration

The big problem, though, with this deal (and another execs mentioned on the call but haven’t formally announced) is that the economics associated with it are utterly opaque. The earnings call was one of those entertaining ones where analysts try to find any way they can to get more information on a particular data point, largely without success. The deal with Cisco is apparently subject to such tight non-disclosure terms that BlackBerry couldn’t say how much the deal would bring in, whether it was a one-time item or recurring revenue, what exactly was included in the revenue, or anything else of interest. All of this makes it incredibly tough to evaluate the real significance of the Cisco deals and others like it, because it’s almost impossible to tell what it means for the future. John Chen did say on the call that there were more such deals in the pipeline and that they should land later this fiscal year (which ends in February 2016), but he provided no real visibility at all over what the run rate in this business is likely to be, other than to say that the $500 million goal now looks very achievable.

That still feels to me like moving the goalposts on the original goal of growing software revenues (rather than technology licensing revenues) to $500 million, but the larger story is that BlackBerry looks like it might finally have an alternative source of revenue which can in time take the place of its legacy hardware and service revenues, which is the company’s single biggest challenge. As those older revenue streams fall, BlackBerry has struggled to find a new revenue stream that could offset the decline and get the company back to growth. It’s possible that it’s now found that revenue stream, through a combination of fairly modest core enterprise software growth and this new technology licensing stream. The big question is whether that revenue stream is sustainable over time – will it provide recurring revenues each quarter going forward in a way that can mimic its previously very dependable hardware and service revenues? Or will it be a series of, as John Chen said on the earnings call, “lumpy” one-off payments that provide no real certainty over the future of the business?

The revenue mix is changing again

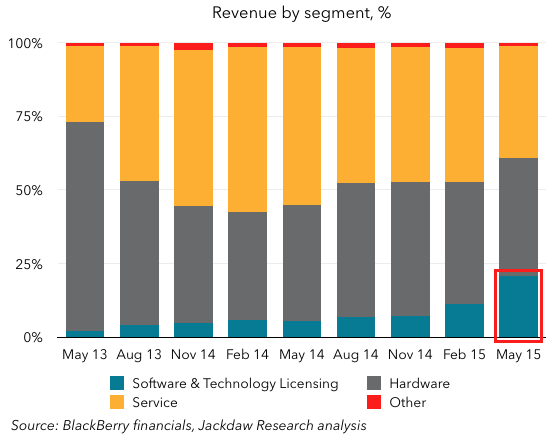

If this Software and Technology Licensing revenue stream really does keep up the momentum, it will mean a second major shift in BlackBerry’s revenue mix. The first was due to the decline of hardware, which once regularly accounted for 70-80% of BlackBerry’s revenues but has now dropped to 40% or so, with Services making up most of the difference. This second shift, though, will see software become first a significant contributor to overall revenue and in time the major contributor to revenue. This quarter was the start, as the chart below shows: The question is whether BlackBerry can keep this momentum going – it’s not too much of a stretch to suggest the company’s future depends on it.

The question is whether BlackBerry can keep this momentum going – it’s not too much of a stretch to suggest the company’s future depends on it.