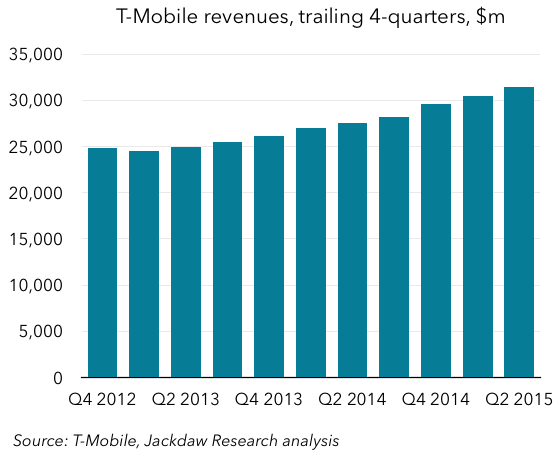

T-Mobile reported its earnings this morning, and as usual lately there was a strong component of growth – across subscribers, revenues, and even average revenue per subscriber. I’m going to run through the highlights quickly, but then I’m going to drill down around what drives that growth, and how T-Mobile is able to grow at this rate even as its competitors struggle to do so.

Note: I’ve written extensively about T-Mobile before, and remain skeptical about some of the aspects of its business model and strategy, but this post will focus on the flip side of that: the undeniable growth in its business. In addition, you can find my analysis of other major tech companies’ earnings here, and you can subscribe to the Jackdaw Research Quarterly Decks service if you want to get a full set of charts on the major tech companies and on the US wireless, cable, satellite, and telecoms operators.

Quick growth review

The two charts below show all you really need to know about growth at T-Mobile – from stagnation and decline pre-2013, the company has turned itself around dramatically, growing subscribers at a now fairly steady pace of 15-18% per quarter, and as a result revenues have been growing too.

How does T-Mobile do it?

So, the big question becomes how T-Mobile is able to achieve this, when the other three major US carriers are not able to do so. Verizon’s year on year wireless revenue growth has been around 5-10%, AT&T’s has recently been in the low single digits, and Sprint’s has been negative for several quarters. Subscriber growth at T-Mobile’s two largest competitors – AT&T and Verizon – has been stronger, but largely driven by things other than phones, whereas T-Mobile’s growth has been almost entirely based on the traditional phone business. That’s a liability in some ways, because the base of phones in the US isn’t really growing much anymore, but at the moment T-Mobile is capturing what growth there is, while stealing subscribers from competitors. I’m going to focus mostly on postpaid in most of the analysis below, because that’s where T-Mobile’s growth is largely coming from.

The key to T-Mobile’s growth is the combination of two separate effects: churn (subscriber losses) and gross additions (the new customers a carrier adds). Simply put, the net subscriber additions number that most analysis of the wireless industry focuses on is the net result of these two forces. However, when you just focus on that number it’s easy to miss how these two come together in very different ways for the different carriers. What T-Mobile is doing uniquely well is combining very low churn (subscriber losses) with high gross additions (new customers). Note that T-Mobile and the other carriers typically don’t report their actual postpaid subscriber losses or gross additions directly, but given their churn and net addition numbers we can do a fairly straightforward calculation that gets us there with a reasonable degree of accuracy.

Churn – far lower than in the past, and at smaller scale

Churn is the first aspect of this equation. Briefly, the reported churn number is the average percentage of the subscriber base that leaves the carrier during each month of the quarter. So, if churn is 1%, that means that on average during the quarter 1% of the subscriber base stopped being a customer, and that in turn means that around 3% left during the quarter. The US carriers generally report churn for their two major sets of customers – postpaid and prepaid – because churn rates are very different for these two groups. Prepaid churn is far higher than postpaid, because these customers can more or less come and go as they please, without contracts, device payments, or anything else to make it hard to leave. T-Mobile has very successfully lowered its postpaid churn over the past couple of years, and this is a major component of how it’s turned its growth around:

T-Mobile has actually switched from metric to another during the period shown – first reporting total postpaid churn (including devices like tablets and modems) and now reporting phone churn specifically. As you can see, the combined number has fallen from 2.5% in 2012 to 1.3% now. That might not seem a lot – these numbers sound pretty small – but remember that that’s a monthly churn rate, so the quarterly churn is three times as high, and during the course of a year, a 2.5% churn rate means you lose 30% of your customers, whereas a 1.3% churn rate almost halves those losses.

T-Mobile has actually switched from metric to another during the period shown – first reporting total postpaid churn (including devices like tablets and modems) and now reporting phone churn specifically. As you can see, the combined number has fallen from 2.5% in 2012 to 1.3% now. That might not seem a lot – these numbers sound pretty small – but remember that that’s a monthly churn rate, so the quarterly churn is three times as high, and during the course of a year, a 2.5% churn rate means you lose 30% of your customers, whereas a 1.3% churn rate almost halves those losses.

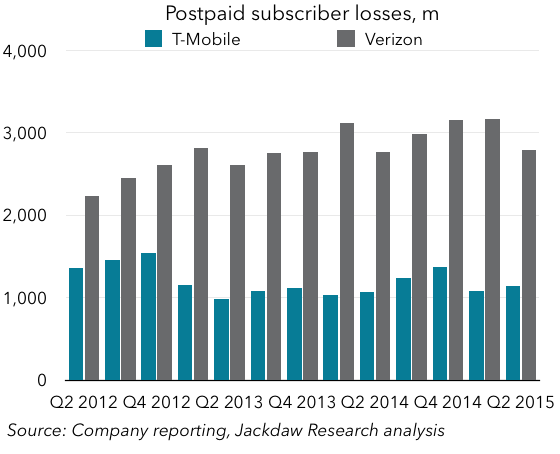

Of course, how many subscribers you actually lose is a factor not just of your churn rate but also the size of your subscriber base. To make it more concrete, let’s look at what’s happened to actual subscriber losses implied by that churn during this time. To put it in context, we’ll compare these losses to Verizon’s, which has typically had the lowest churn rate in the industry at around 1%, but also the largest number of postpaid customers (over three times as many as T-Mobile). The chart below shows the subscriber losses each quarter implied by the company’s respective churn rates and subscriber bases:

As you can see, each quarter Verizon loses somewhere around 3 million customers, even at its very low 1% churn rate, whereas T-Mobile’s slightly higher churn rate results in much lower losses – just over 1 million most quarters. So, right off the bat, even with a lower churn rate, Verizon has to win three times as many new subscribers as T-Mobile each quarter just to tread water. The combined effects of T-Mobile’s falling churn and its relatively small base give it a significant advantage over AT&T and Verizon (both of which have lower churn but much bigger bases) and Sprint (which has a very similar base but much higher churn).

As you can see, each quarter Verizon loses somewhere around 3 million customers, even at its very low 1% churn rate, whereas T-Mobile’s slightly higher churn rate results in much lower losses – just over 1 million most quarters. So, right off the bat, even with a lower churn rate, Verizon has to win three times as many new subscribers as T-Mobile each quarter just to tread water. The combined effects of T-Mobile’s falling churn and its relatively small base give it a significant advantage over AT&T and Verizon (both of which have lower churn but much bigger bases) and Sprint (which has a very similar base but much higher churn).

T-Mobile adds half as many subs as Verizon

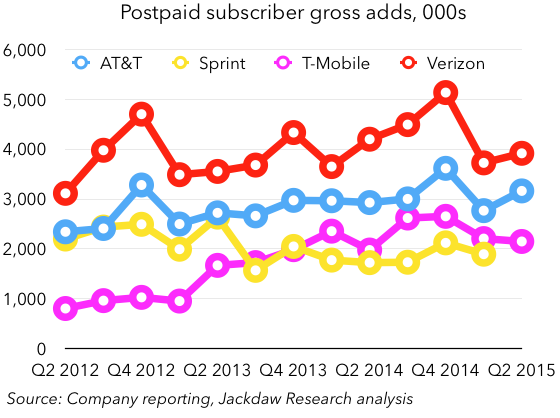

The other side, of the puzzle, then, is that these companies have to add enough new subscribers to at least offset the losses, but ideally quite a few more to drive subscriber growth. The chart below shows derived postpaid gross additions for the big four carriers (Sprint hasn’t reported Q2 results yet): What you can see is that T-Mobile has far from the highest gross additions of the four carriers – in fact, last quarter its gross adds were just barely higher than Sprint’s. Verizon and AT&T both had significantly higher gross additions, driven in part by their far larger bases (many additions are additional lines sold to existing customers at this point) and their far larger marketing spend and to some extent store footprints. In short, T-Mobile isn’t winning more new customers than its major competitors – in fact, it’s in third place and fairly close to Sprint. Verizon actually adds roughly twice as many customers each quarter. The big difference is that low churn combined with its small base size, which combine for a much smaller loss of subscribers each quarter, and allow it a head start on growing subscribers.

What you can see is that T-Mobile has far from the highest gross additions of the four carriers – in fact, last quarter its gross adds were just barely higher than Sprint’s. Verizon and AT&T both had significantly higher gross additions, driven in part by their far larger bases (many additions are additional lines sold to existing customers at this point) and their far larger marketing spend and to some extent store footprints. In short, T-Mobile isn’t winning more new customers than its major competitors – in fact, it’s in third place and fairly close to Sprint. Verizon actually adds roughly twice as many customers each quarter. The big difference is that low churn combined with its small base size, which combine for a much smaller loss of subscribers each quarter, and allow it a head start on growing subscribers.

Put another way, if T-Mobile had its current churn levels but was the size of AT&T or Verizon, it would currently be in last place rather than first place in net additions. AT&T and Verizon simply can’t grow phone gross additions much faster in the current, highly saturated, US phone market, so they’re pursuing growth where they can find it, which is in tablets and in new categories of connectivity like connected cars, home automation, and machine-to-machine communications. T-Mobile, however, benefits from its smaller scale (which is a liability in other ways) and from its good work in reducing churn rates, to the point that it’s consistently outperforming the other carriers in adding postpaid phone customers.

An increasing challenge

However, the larger T-Mobile gets, the more subscriber losses the same churn rates translate to, and the harder it will have to work to gain new subscribers. You can see from the earlier chart on subscriber losses that despite the progress on churn, losses aren’t falling, but rising. Despite a drop in churn from 1.48% in Q2 last year to 1.32% this year, losses actually rose slightly year on year, because that churn was on a base that had grown by almost five million. This will be an increasing challenge for T-Mobile, which is going to have a bigger hole to fill each quarter with new subscriber additions, even at a time when competitors are competing more aggressively and some of the lowest-hanging fruit for T-Mobile has been plucked.