It looks like a slew of reviews of Google’s OnHub router have come out in the last 24 hours or so, so I’m guessing some sort of embargo has lifted. It seems the reviews are decidedly mixed (which feels par for the course today for products both good and bad, as reviewers each seek to find something unique to say, often overreaching in search of something worth praising or criticizing). Glenn Fleishman has an interesting review of reviews of sorts at TidBits, which is worth reading for its own sake and for the links to other reviews.

What I wanted to write up here quickly isn’t a review (I don’t have a review unit) but some other related thoughts I’ve had about the OnHub router since it was announced, and which have been reinforced by reading some of these reviews. We discussed some of this on the Beyond Devices Podcast a few weeks back, the week the router was announced, but I’ll probably go a bit deeper on some of it. I’ll embed the podcast episode at the end of this post too.

A router for novices at a power user price

One of the things that struck me off the bat, but has really been brought home by these reviews, is that there’s a fundamental mismatch between the price positioning of this router and the target audience. The whole value proposition (at least for today – and we’ll come back to this) of this router is that it’s enormously simple to use. And yet it’s priced at $200, the same sort of range as the high-end routers in the market. The Wall Street Journal review notes some interesting trends in the router market, which I think serve as useful context for this device:

Cable companies and other Internet service providers now rent their customers basic Wi-Fi routers when they sign up for service. As a result, U.S. router sales have fallen from 6.1 million year-to-date in 2012 to 3.5 million in the same period this year, market research firm NPD reports… NPD determined that the average selling price is on the upswing. Cheap routers aren’t selling so well, but higher-end models… are. “People are willing to pay a lot of money—more than before—for an AC router with significantly better performance than they had in the past,” said Mr. Baker.

Here’s the thing: I’m betting that the kind of people who are willing to pay a lot of money for “an AC router with significantly better performance” are not the kind of people who feel intimidated by those routers. They’re the kind of people who know enough about routers to understand what distinguishes 802.11ac from some of the older technologies, and who are likely pretty comfortable customizing the various settings. And yet Google’s router is priced in this same range and yet removes many of the typical settings available to power users in other routers in that category. You can’t specify separate SSIDs for the 2.4GHz and 5GHz bands, you can’t get into a web interface, and many of the other deeper settings you can configure on almost any other router. This is a router for novices sold at a power user price point. As such, it’s likely to please neither group.

This is further reinforced by the fact that the router is clearly something of a trojan horse for Google in the home automation space, given the inclusion of Bluetooth and Zigbee, and yet again those users are likely to want far more control over their routers than the OnHub provides. Some of this may be solvable in software down the line, but I suspect Google’s whole mentality around this router is wrong, and that can’t be fixed by software updates.

A symbol of Google’s disjointed approach

To my mind, the OnHub router is also a symbol of Google’s disjointed approach to so many of its projects, and I worry that the Alphabet reorg will only make things worse. Google already has a home automation business, Nest, which not only makes its own products but has been the vehicle for both making further home automation acquisitions (Dropcam) and for acting as a hub for other home automation gear (the Works with Nest strategy). And yet, this product isn’t branded Nest, nor does it apparently sit under Tony Fadell’s hardware group, which also includes Google Glass. In fact, Mark Bergen of Recode and Amir Efrati of the Information have both suggested that this product actually came out of the Google Fiber team. I’ve written previously about how disconnected from the rest of Google the Fiber project has seemed, and it’s ironic to now see Google proper appropriate this technology just as Fiber is being hived off into a separate Alphabet company. The good thing about Google is that people throughout the organization feel free to experiment with various things, some of which eventually become products. The bad thing is that this means you could have several separate teams working on similar things in isolation, and in some cases you end up with several products apparently chasing the same use case (e.g. the Nexus Q, Chromecast, and Google TV/Android TV).

The naming of the OnHub router, the subdomain on.Google.com, the naming of the companion app (Google On), and so on all suggest that this is the beginning of a broader strategy (and we already know that there will be another router made in partnership with Asus). But this is yet another effort within Google to tie together the different devices in the home. Why isn’t it owned by Nest? How will it relate to Android TV and Chromecast, Google’s other living-room projects? So many questions, and so few answers…

The theory and the reality

One other thing Google has touted as part of its positioning for the OnHub is this idea that it is pretty enough to sit in the living room. This, too, feels like a very Googley statement – I’m not sure how many people with real design sense would actually want even a relatively good-looking router in their living rooms. But it’s also a bit of a non-starter as a practical matter – the router doesn’t stand alone – it needs both a power cable and an ethernet cable to function, and you’ll seldom find both of those in the middle of a living room. You’ll at least have power outlets in the wall, but your cable modem is likely to be in a closet somewhere rather than in your living room. And with only one jack in the back of the device, you’re going to need a switch somewhere else anyway for the rest of your hardwired devices, another example of the mismatch between functionality and pricing.

I could go on with all this, but you get the idea. Though an interesting product, the OnHub feels like it falls short on the theory alone, let alone the reality (where several of the reviews suggested it falls down too, even on the most touted features). But it also feels like it’s emblematic of several of the key challenges Google has – too many experiments and projects that are poorly coordinated, poorly thought-through, and ultimately poorly executed. I’m not convinced that the Alphabet structure will help with any of this, and in fact it’s quite likely that it will make the fragmentation problem worse rather than better.

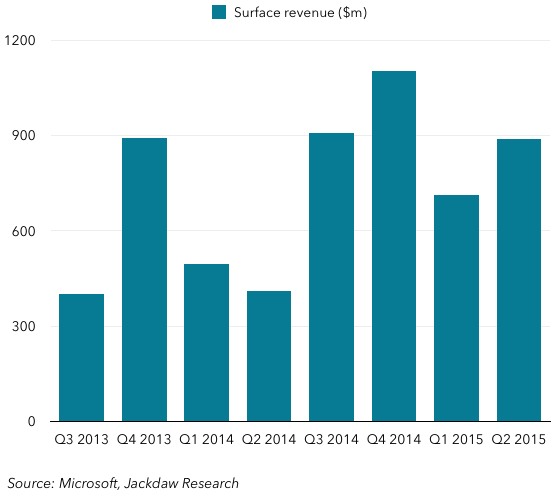

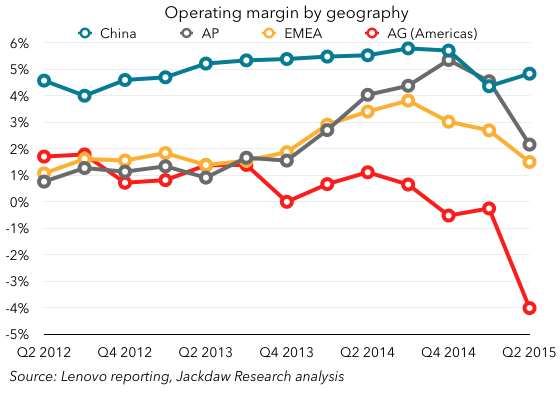

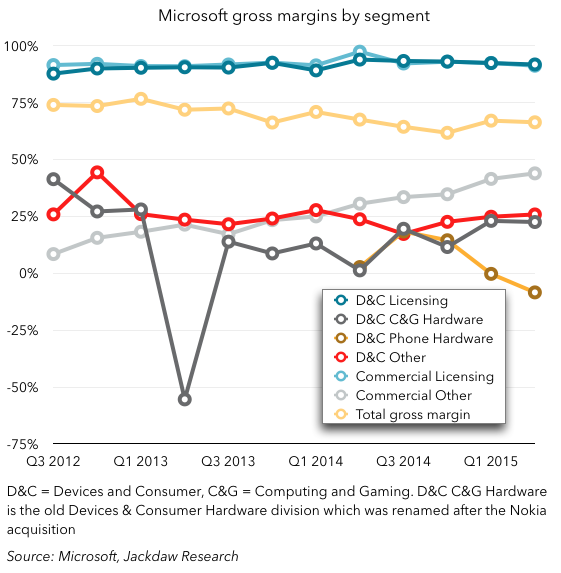

Licensing continues to have the highest gross margin – cost of sales are tiny compared to revenues in that business since the incremental cost of an additional sale is close to zero. But Commercial Other, composed primarily of cloud services and enterprise services, is becoming increasingly profitable, and with its growth is also becoming an increasingly important contributor to overall margins. It’s at around 9% of gross margins now, up from under 2% at the beginning of 2013, and growing fast. Commercial licensing continues to account for the lion’s share of gross margins, at 64.5%, while consumer licensing accounts for 20% or so. Note, however, the margins in the phone hardware business, which were never great to begin with, but have fallen steeply the last two quarters and are now negative. Remember, too, that these are gross margins, so operating margins in this business are likely substantially lower still. Computer and gaming hardware (Xbox, Surface, and a few other things) is becoming increasingly profitable at a gross margin level, however, helping to justify the continued investment in two products many people consider non-core to Microsoft’s business.

Licensing continues to have the highest gross margin – cost of sales are tiny compared to revenues in that business since the incremental cost of an additional sale is close to zero. But Commercial Other, composed primarily of cloud services and enterprise services, is becoming increasingly profitable, and with its growth is also becoming an increasingly important contributor to overall margins. It’s at around 9% of gross margins now, up from under 2% at the beginning of 2013, and growing fast. Commercial licensing continues to account for the lion’s share of gross margins, at 64.5%, while consumer licensing accounts for 20% or so. Note, however, the margins in the phone hardware business, which were never great to begin with, but have fallen steeply the last two quarters and are now negative. Remember, too, that these are gross margins, so operating margins in this business are likely substantially lower still. Computer and gaming hardware (Xbox, Surface, and a few other things) is becoming increasingly profitable at a gross margin level, however, helping to justify the continued investment in two products many people consider non-core to Microsoft’s business.