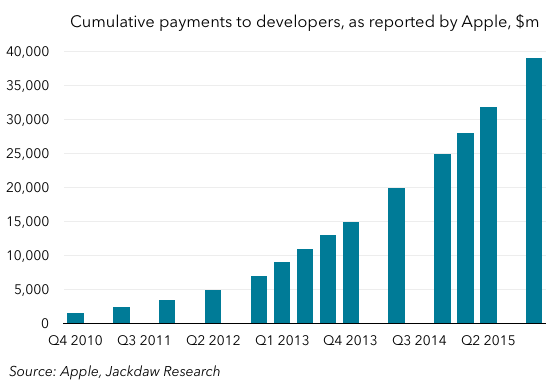

For reference, this page lists all prior Apple posts, with a little context. Subscribers to the Jackdaw Research Quarterly Decks Service will be getting a preliminary Apple deck tomorrow, with a final deck to follow once Apple files its 10-Q.

This is a post I’ve been meaning to write for a while now, but it seems particularly apt given Apple’s results announced today. My key point is this: even as Apple continues to diversify its revenue streams beyond the iPhone, the size of the installed base of iPhones becomes ever more important to its revenue growth.

The context here is that I’ve been talking to lots of reporters over recent weeks in the run-up to Apple’s earnings, and I’ve heard this question (or variations on the theme) a lot: “is Apple’s increasing dependence on the iPhone a problem?” The reason for the question is twofold: on the one hand, Apple’s revenues and margins have been increasingly dominated by the iPhone, and on the other it’s become increasingly clear that iPhone growth would slow following its stellar year off the back of the iPhone 6.

My answer usually goes something like this, and this gets to the heart of the paradox here. On the one hand, yes, Apple has been increasingly dependent on the iPhone for revenue and margin growth, but it’s been working hard to introduce new products and services to the market which can help to contribute meaningfully to growth and profitability. The Apple Watch, Apple TV, Apple Music, and iPad Pro were all introduced in 2015, and could over time provide significant additional revenue and margin. So Apple has the potential to lessen its dependence on the iPhone over time in this way.

However, the other side of the paradox is that almost all of these new products and services are tied to the iPhone in some way, and benefit greatly from the installed base of a half billion iPhone users. The iPad Pro has the weakest tie here, but obviously benefits from its use of iOS and the App Store, and with features like Handoff and iCloud works better with the iPhone than it does independently. The rest have much closer ties to the iPhone: the Apple Watch is (for today at least) strictly an iPhone accessory, the new Apple TV runs apps, most of which were originally developed for the iPhone, Apple Music will be used on iPhones far more than on any other devices, and so on. Even if iPhone growth slows or goes negative (as it will now certainly do in the March quarter), that massive base of iPhone users will keep many other contributors to Apple’s financial success ticking over nicely.

Interestingly, Apple seems to have latched on to this idea as a key talking point for its earnings today, with an emphasis on Services revenue tied to the overall installed base of devices, which it pegs at 1 billion users. (My estimate for the end of December for iOS devices plus Macs was 996 million, so adding in Apple Watch and Apple TV should certainly push it over that billion user threshold). This base of devices, and the rather smaller number of unique users it represents, is Apple’s single greatest asset, and one it will increasingly leverage both as it continues to grow the product and service lines it announced in 2015 and as it adds to them going forward. As such, even as the iPhone itself as a product contributes less to Apple’s overall performance, it’s going to become ever more central to Apple’s future growth.