Note: you can see all my previous posts on Netflix here. The analysis here draws on financial and operating data I collect on Netflix, along with around a dozen other big tech companies. Subscribers to the Jackdaw Research Quarterly Decks Service get quarterly charts based on this data, and data sets are also available to purchase on a one-off or subscription basis. Please contact me if you would like more information about any of this.

Netflix just announced that it’s expanding to around 130 new countries including many of the largest countries it wasn’t in yet. This was a huge and unexpected move, at least so early in 2016, since Netflix had previously indicated that it would make this move more gradually during the year, with just a handful of markets pre-announced for early 2016. I want to focus on the possible financial impact of this expansion, because it seems to me that it could be significant.

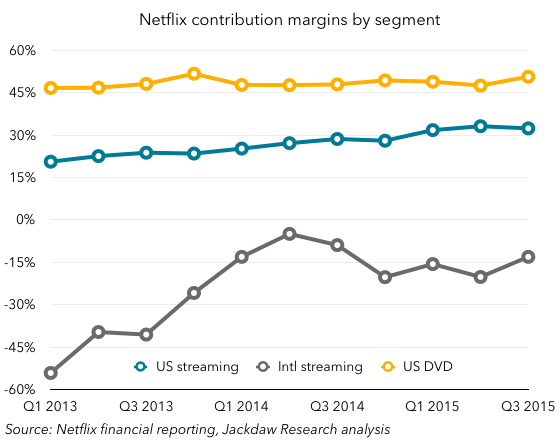

First off, Netflix’s International business is significantly less profitable than its US business: I’ve written in the past (somewhat jokingly) that every time its international business threatens to turn a profit, Netflix expands into a few more countries. As you can see, though, its International segment continues to be unprofitable at this point, and has much lower margins than its increasingly profitable US streaming business. Why is this? There are several reasons, but they’re all applicable to this new expansion and the likely financial impact.

I’ve written in the past (somewhat jokingly) that every time its international business threatens to turn a profit, Netflix expands into a few more countries. As you can see, though, its International segment continues to be unprofitable at this point, and has much lower margins than its increasingly profitable US streaming business. Why is this? There are several reasons, but they’re all applicable to this new expansion and the likely financial impact.

Free trials

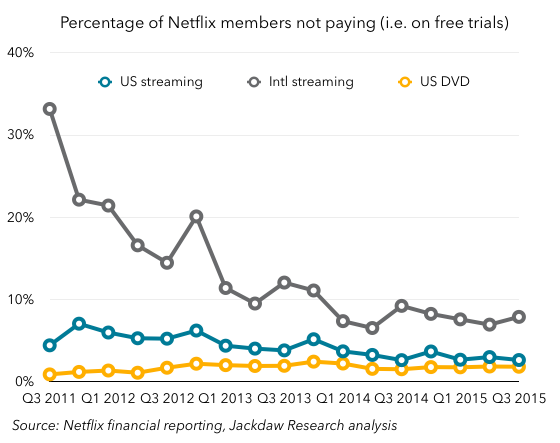

Firstly, Netflix offers one-month free trials to customers. Naturally, the impact of these free trials is heaviest in new markets, and you can see this when you look at the percentage of Netflix customers in various markets who are included in its membership count but not in its “paid members” count:

In the past, as Netflix has expanded into new markets, this percentage has been in the 30% range, though it’s recently dropped down to around 10% or just below. However, with 130 new countries going live simultaneously today, it’s likely that this number will skyrocket. With 25 million members in its existing markets, it’s easy to imagine that Netflix might garner comparable numbers of free trial subscribers in the coming months in 130 countries. As such, a huge percentage of its subscribers overseas will be incurring costs but not generating revenue.

In the past, as Netflix has expanded into new markets, this percentage has been in the 30% range, though it’s recently dropped down to around 10% or just below. However, with 130 new countries going live simultaneously today, it’s likely that this number will skyrocket. With 25 million members in its existing markets, it’s easy to imagine that Netflix might garner comparable numbers of free trial subscribers in the coming months in 130 countries. As such, a huge percentage of its subscribers overseas will be incurring costs but not generating revenue.

Marketing costs and scale

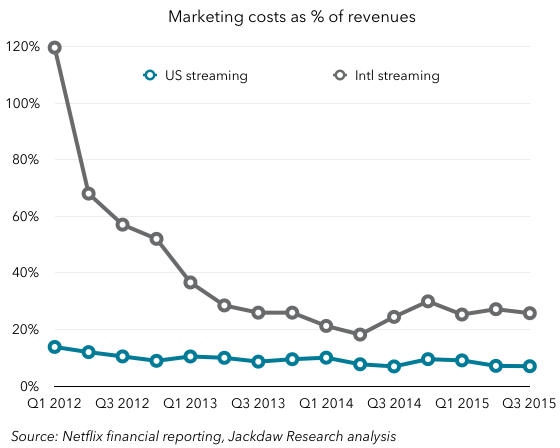

Another major reason why new markets are less profitable is that Netflix has to do far more to promote itself in these markets where customers aren’t yet familiar with its brand. This chart shows marketing spend as a percentage of revenues for the US and International streaming businesses: As you can see, marketing spend is a much higher percentage of revenue in the overseas business than domestically, where Netflix has actually been reducing its marketing spend other than in its big new content launch quarters.

As you can see, marketing spend is a much higher percentage of revenue in the overseas business than domestically, where Netflix has actually been reducing its marketing spend other than in its big new content launch quarters.

As Netflix scales in a given market, this impact is reduced, as the base of revenues from existing customers allows the company to spread that high marketing cost over a larger base, and as awareness and therefore word of mouth marketing grows. However, with 130 new countries, Netflix will have to spend heavily on marketing in the coming months to promote its services. Another huge scale effect is the shared costs of doing business in a new country – converting content to new languages, hosting the content locally, and so on all adds up, and in these countries those costs will be shared by a very small number of subscribers in the short term.

Outgrowing the DVD business

One interesting aspect of Netflix’s business which I’ve covered in the past is the fact that the US DVD business continues to throw off very nice profits, which in turn has largely funded Netflix’s overseas expansion: The problem is that this new expansion will be so significant that it seems very unlikely Netflix will be able to offset the losses with its cash cow anymore. As such, overall margins will likely suffer significantly.

The problem is that this new expansion will be so significant that it seems very unlikely Netflix will be able to offset the losses with its cash cow anymore. As such, overall margins will likely suffer significantly.

The financial impact could be considerable in the short term

For all these reasons, I believe the financial impact of Netflix Everywhere could be very significant in the short term. I’ve been pretty bullish on Netflix overall, and I’ve felt that its slow and steady international expansion coupled with its gradual improvement in US streaming margins was a fantastic combination. This big-bang approach threatens to derail that strategy, albeit only temporarily, bringing what might have been a longer-term dampener on margins forward into a much more compressed space of time, but opening up a far bigger opportunity longer term. I’m very curious to see how Netflix talks about the financial impact here – its press release on the news was conspicuously devoid of any talk of the financial side. But the market certainly seems to like the news so far.