When the new 9.7″ iPad Pro was released a few weeks ago, Apple was kind enough to send me a review unit, which I’ve been testing since. I thought I’d share some of my thoughts on using this device for the past couple of weeks.

Update: I added a little something on the Apple Pencil – I initially left it out because I simply haven’t used it much, but it’s worth noting that fact in and of itself. The addition is near the end of the review.

Initial impressions

My first experiment was to try a day of working solely with the 9.7″ iPad Pro, and I got through a whole day of fairly varied work without needing to use any other computing device. That surprised me to some extent – other than on the occasional business trip, I hadn’t really ever tried to use an iPad as my sole computer, and I really wasn’t sure how well it would go. That first day turned into several days and eventually two weeks, but even after that first day I immediately knew I also wanted to test the larger iPad Pro, and so I purchased one from the local Apple Store (I’ve since returned it), along with a Surface Pro 4 I acquired for testing too. During that period, I used one or other of the iPads virtually exclusively, with a couple of brief exceptions, and found this barely limited my ability to get done what I wanted to.

The first thing I noticed was that the device felt more intimate and personal – instead of staring at a screen sitting a couple of feet away and using peripheral keyboard and mouse that felt very disconnected from the computer, I was engaging entirely with this screen that was immediately in front of me, including touching it occasionally. That felt very different from my usual computing experience in subtle ways. Obviously you get some of the same feeling from using a laptop, but with the iPad it felt subtly different, and I think part of that is because I’m used to thinking of iPads as devices that you hold. Although a lot of my work was done with the iPad resting on the keyboard case, throughout the day I also picked it up from time to time without the case and used it for catching up on Twitter or reading things, and in the evenings it had the flexibility to be used that way too.

For this reason, I love the new modular approach to cases and covers Apple now has – it used to be that you either had a case that included a cover, just a cover, or some sort of keyboard case. But the new modular cases from Apple allow you to have a case permanently attached to protect the body, and then to swap out the plain cover and the Smart Keyboard case at will. This feels a lot more flexible and means you just always use whatever you need at any particular point in time, whether that’s just the case when you’re reading something, the case and standard cover when moving around, or the Smart Keyboard cover and case when you know you’ll need to type. This flexibility is one of the biggest things that sets the iPad Pro apart from the Surface Pro too – the Surface always feels more like a computer than a more personal device like a tablet, whereas the iPad Pro makes that transition seamlessly without feeling either awkward or as though it’s missing an important appendage.

The other big difference I noticed in switching between the iPad and Surface was that the default state on the Surface is an empty screen – the desktop. You have to actively go looking for something to do in the Start Menu, where there’s little consistency in how items are presented with all the different sizes of live tiles. Apps you install don’t even show up there by default and it takes hunting around and then replacing default apps with the ones you choose to get them accessible. By contrast, on the iPad (as on any iOS device) you’re always presented with a screen full of possibilities in the form of a set of app icons. You can, of course, rearrange these icons and swipe through several pages of them to find the one you want, but ultimately the default state is being presented with lots of things you could do next. This, too, makes the iPad feel like a more personal device than the Surface.

Keyboards

I found the keyboards on both sizes of iPad very usable. I’m typing this review on the smaller of the two keyboards, and I’m able to type more or less as fast as on my Mac or MacBook Air keyboards. I don’t find the lack of key travel a problem at all, and I like the fabric on the surface of the keyboard. The smaller of the two is definitely more space constrained, but I find that I can adjust very quickly when switching between devices, and the fact that the keys are raised and nicely separated is very helpful. My one niggle with the keyboards is that the globe icon key for switching between virtual keyboards (e.g. invoking the emoji keyboard) is at the bottom left corner and as such the other keys are shifted over to the right a little from other Apple keyboards. That has meant I’m often either hitting that key by mistake or hitting the control key when I mean to hit the option key, for example. I’m a big user of keyboard shortcuts on the Mac and I found most of them translated easily to the Smart Keyboard, but this one change has caused more errors than anything else in the keyboard. My other frustration with keyboard shortcuts has been that option-deleting hasn’t worked the same was as in OS X, in that instead of deleting whole words at a time, it only deletes single letters as if the option key weren’t depressed. That’s one of those muscle memory things that’s been hard to adjust to on the iPad, and should be easily fixable through a software update.

Performance

For the tasks I undertook on the iPad Pros, there was never a performance issue that felt related to hardware. The devices are snappy for all sorts of activities, app switching happens quickly and without glitches, and on the few occasions where you do encounter bugs they feel like they’ll be resolved soon. I loved being able to use the familiar command-tab shortcut for app switching, and it even implements in a clever way when you’re in split-screen multitasking mode. My one big frustration about multitasking and split screen use is the way you have to scroll through an endless list of apps to find the one you want to have show up on the right side. Some sort of search function here is critical for anyone with a large number of supported apps installed. The work that MacStories has published this week on iOS 10 includes a much better interface for this scenario, and Apple would do well to implement something like it.

I found that many of the apps I use on a regular basis already support split-screen multitasking, and that interface works particularly well on the larger iPad Pro, where the apps get to run more or less full size from a 9.7″ iPad perspective side by side. I did find that some interfaces looked squashed on the 9.7″ iPad Pro, especially web interfaces that are designed to run full screen on such a device, but many others worked very well, and it made comparisons and copying and pasting between apps very easy. I had to find a workaround for working with two web pages at once, which involved installing the Chrome browser for the second screen – as others have pointed out, it would be nice to have the ability to put two Safari tabs side by side in the split screen view.

Limits to productivity

I mentioned earlier that I was able to accomplish more than I expected on the iPad Pro. But there were a few tasks that I found either too cumbersome, too risky, or simply impossible on the iPad, and for which I switched back to a Mac. I also found that a key element of my workflow was impossible to replicate on the iPad, and this was ultimately the biggest issue for me:

- Recording and editing podcasts – this is something I do at least twice a week in the case of recording and once a week in the case of editing, and it’s essential that it work well. There are ways now to hook up even powered microphones to the iPad Pro, but you can’t feed two apps at once with that microphone, so it doesn’t work for talking on Skype and recording podcast audio at the same time, as others have mentioned. When it came to editing, the iOS version of GarageBand simply doesn’t supporting importing multiple audio tracks and editing them together, even though I use GarageBand on the Mac usually. For all these reasons, I recorded and edited all podcasts on the Mac during my two-week experiment. I mentioned some of this on Twitter, and was pointed to Ferrite as a possible solution for editing podcasts on the iPad Pro, so there may be workarounds for all this, but it was too much work and too risky to test for a critical podcast recording.

- Document editing workflow – as I’ve written about elsewhere, my workflow involves using the iWork suite to create and edit files, whether spreadsheets, presentations, or documents. But I use Dropbox for storing and syncing those files across computers and making them available on mobile devices. This works fine on the Mac, which has full support for Dropbox at a system level, but it breaks down on iOS. The problem is that Dropbox isn’t available as a source of files to open within the iWork apps on iOS. You can open files from within the Dropbox app, but this process creates a copy, so you’re not modifying the original in real time, and have to export it back to Dropbox when you’re done editing if you want to update the original. There are several possible solutions to this – use Office instead of iWork because Office has proper Dropbox integration, or use iCloud instead of Dropbox because it’s supported natively in the iWork apps. But I prefer iWork for its ease of use and look and feel, and don’t yet fully trust iCloud for syncing really important documents. So I’m sort of stuck when it comes to my current workflow. If I knew I’d be committing fully to an iPad as my only device, I might feel differently, but for now it means it’s tough to carry over my workflow from other devices, which is something many iPad Pro users are likely to need to do. In addition, there are still detailed functions within iWork which simply aren’t available in the iOS versions, even though feature parity is pretty extensive. I found that a little frustrating too.

- Working with Apple News – I’ve recently started publishing this blog and our podcast to Apple News, something which comes with its fair share of pros and cons no matter which device you’re using (something we talked about on the podcast recently). But on iOS, the Apple News Publisher online interface at iCloud.com doesn’t work. If you visit iCloud.com on any iOS device (even the larger iPad Pro) you get redirected to the mobile site, which is mostly a holding page, but if you request the desktop site through Safari, you get the full site. However, even then, the Apple News Publisher site clearly isn’t meant to work on iOS, and frequently crashes and has other issues. This means if you want to use Apple News Publisher, you have to find some other way to do it than through the WYSIWYG editor online. It’s a new platform, and so maybe better support for iOS devices will come soon.

The iWork feature parity issue and this Apple News problem are indicative of one of the biggest issues I encountered productivity on the iPad Pro – for all that Apple wants to sell these devices as fully-fledged productivity machines, it’s Apple’s own services and apps that continue to hold it back. It’s frustrating that there are a number of Apple’s own apps which don’t support split-screen multitasking yet either. Ironically, you’d be better off in some ways using the Office suite than iWork on these iPads, and that raises an interesting possibility – that the future of mobile productivity marries Apple devices with Microsoft (or other third party) software.

Quick thoughts on the Apple Pencil

My review unit came with an Apple Pencil, and I was particularly keen to try it out. The reality is, however, that there’s very little that I have ever used a stylus for in the past, and that has less to do with the quality of the styli available and more to do with the way I work. I type much more quickly (and legibly and searchably) than I write by hand, and so I always type when I possibly can. I did take notes for a few hours using the Pencil and iPad in place of a pen and notebook, and found it a really solid experience. I was using Microsoft’s OneNote app, which was mostly fine but frustratingly doesn’t explicitly support the Pencil or the associated palm rejection. I tried using the Surface with its pen later for the same task, and found the tactile feel and the resulting handwriting significantly inferior to the Pencil. That’s a bit surprising given how much longer Microsoft has been doing Surface pens, but the difference was undeniable to my mind.

However, I’m not an artist either, and other than for the novelty value, and the occasional bit of doodling in Pigment just for fun, I find myself using the Pencil very little. I think it makes perfect sense that it’s an optional accessory rather than a bundled feature of the iPad Pro – many users aren’t going to need it. I used it enough to be convinced that it would work well should I need it, but I’m fairly certain that I’ll continue to use it only infrequently. My one frustration was charging – it’s not really practical either to charge the Pencil in the standard way (i.e. plugging it into the iPad) while using the iPad or while charging the iPad. Several times, I wanted to charge both devices at night but couldn’t without using the specialized adapter for the Pencil with its own charging cable. That feels like a mistake (and I’m convinced I’d lose the adapter and/or the Pencil’s cap pretty quickly if I were using it more regularly).

Conclusions

After using the iPad Pro(s) more or less exclusively for two weeks, I can say that (with very few exceptions) I’d be happy to do so again in future. I do like the flexibility of my usual Mac Pro setup, but I got a great deal out of using an iPad instead for a while, not least a greater sense of focus on the task at hand and that sense of intimacy I mentioned earlier. Were I to find myself in a situation where I had to commit to one of these devices full-time, I’d definitely pick the larger iPad Pro – the increased screen real estate allows multitasking and other features to really thrive, and its similarity to the size of a standard laptop helps too.

The reality is, though, that these devices don’t have to fill that role for me. I have other computers available to me, and for a variety of reasons they’ll continue to be my main ones. As such, the smaller iPad Pro feels like a great fit as more of an occasional device – one to use in the evenings, or when I need to go out for a while but stay productive, or when I’m traveling. I’d almost always resisted only taking an iPad with me on business trips in the past, but could see myself relying solely on an iPad Pro for at least short business trips in future.

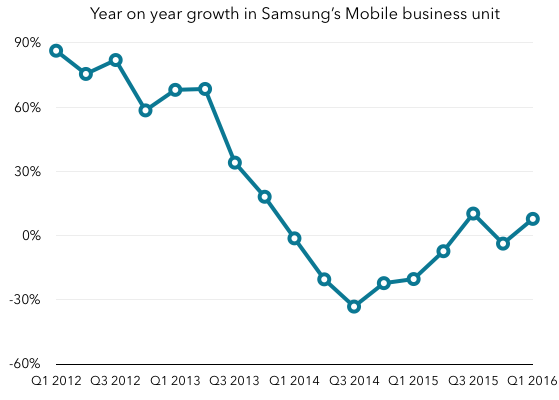

When it comes to margins, the IT and Mobile business unit did considerably better this quarter as well, with the best margins in almost two years:

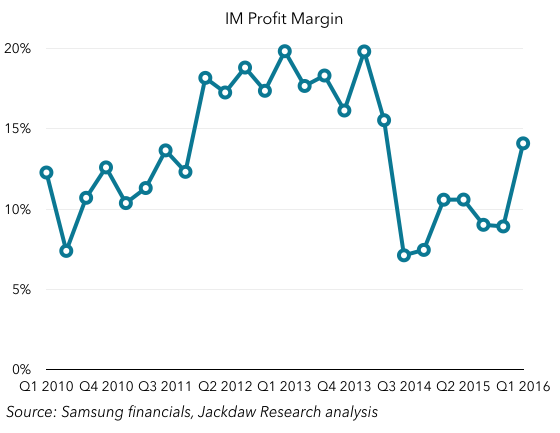

When it comes to margins, the IT and Mobile business unit did considerably better this quarter as well, with the best margins in almost two years: And thanks to a combination of that increase at the IM unit as well as slightly weaker operating margins in semiconductors, IM became the biggest contributor to profits again for the first time in two years:

And thanks to a combination of that increase at the IM unit as well as slightly weaker operating margins in semiconductors, IM became the biggest contributor to profits again for the first time in two years: To what should we attribute all this? These were the bullet points from Samsung’s management for the quarter as relates to mobile:

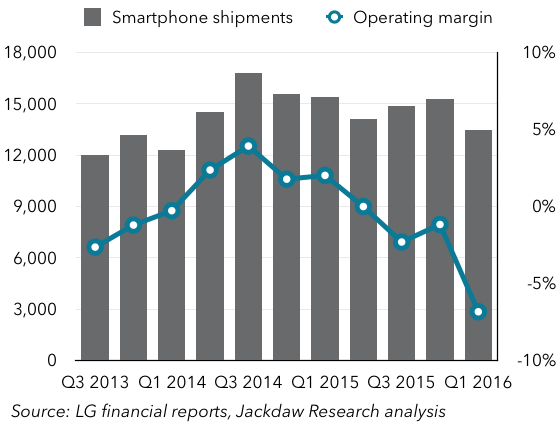

To what should we attribute all this? These were the bullet points from Samsung’s management for the quarter as relates to mobile: It’s harder to tell what’s going on there with the smartphone shipments line than the margin line, but over time it’s trending consistently downwards, as you can see in this trailing 4-quarter smartphone shipment chart:

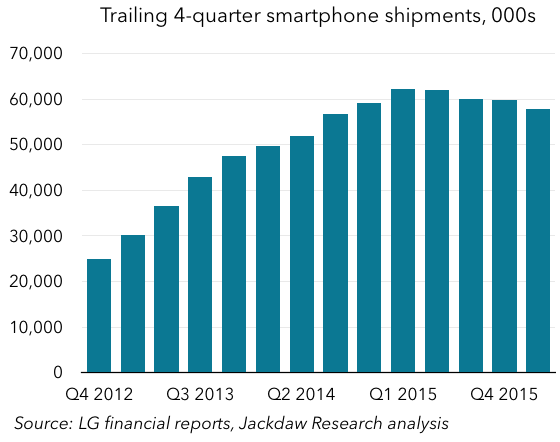

It’s harder to tell what’s going on there with the smartphone shipments line than the margin line, but over time it’s trending consistently downwards, as you can see in this trailing 4-quarter smartphone shipment chart: LG appears to be suffering from much the same malaise as the other mid-tier Android smartphone vendors:

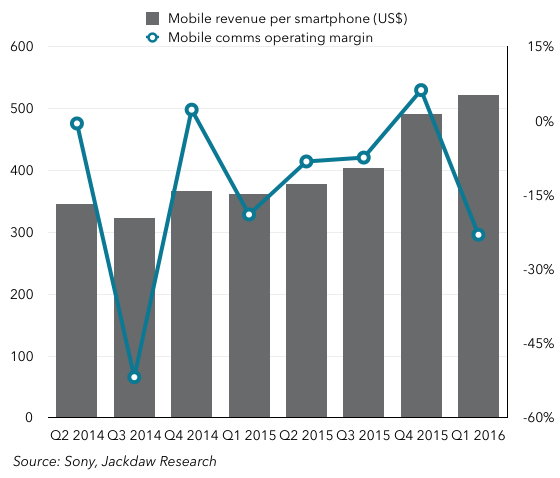

LG appears to be suffering from much the same malaise as the other mid-tier Android smartphone vendors: As you can see, the strategy to sell fewer phones is clearly working – sales dropped off a cliff from Q4 to Q1, and the company hasn’t sold so few phones in many years. What about the other side of the strategy? Well, that seems to be working too – revenue per device sold is up:

As you can see, the strategy to sell fewer phones is clearly working – sales dropped off a cliff from Q4 to Q1, and the company hasn’t sold so few phones in many years. What about the other side of the strategy? Well, that seems to be working too – revenue per device sold is up: The problem, though, as you can also see from that chart, is that the higher ASPs aren’t – yet – leading to higher margins. In fact, margins fell this quarter, and that means an even bigger loss per device, given what happened to shipment numbers. It’s likely that the problem here is that it’s very hard to scale down the operation that produces smartphones as quickly as the number of smartphones sold scales down. Certainly, cost of sales should come down fairly rapidly, but all the other general costs of running a smartphone business aren’t as easy to cut, at least not quickly. It remains to be seen whether that other side of the strategy can fall in line too. If not, Sony will have just cut its business in half without seeing any of the margin benefits it should see from focusing on premium devices. It’s also not clear whether anyone can make money selling just 3 million smartphones a quarter.

The problem, though, as you can also see from that chart, is that the higher ASPs aren’t – yet – leading to higher margins. In fact, margins fell this quarter, and that means an even bigger loss per device, given what happened to shipment numbers. It’s likely that the problem here is that it’s very hard to scale down the operation that produces smartphones as quickly as the number of smartphones sold scales down. Certainly, cost of sales should come down fairly rapidly, but all the other general costs of running a smartphone business aren’t as easy to cut, at least not quickly. It remains to be seen whether that other side of the strategy can fall in line too. If not, Sony will have just cut its business in half without seeing any of the margin benefits it should see from focusing on premium devices. It’s also not clear whether anyone can make money selling just 3 million smartphones a quarter.

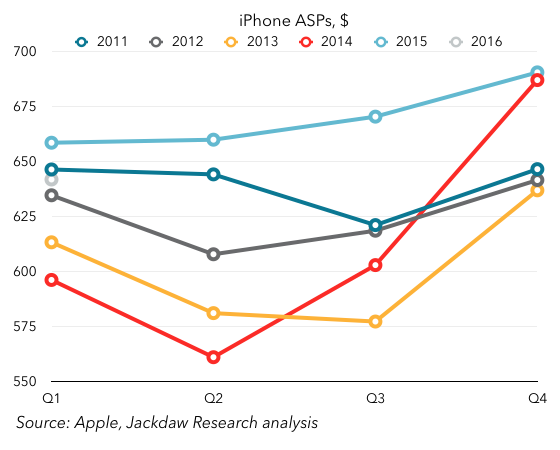

As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.

As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.