I’m on vacation this week in Europe, but I took a quick break to cover Apple and Twitter’s earnings this evening before heading to bed. I’ve tweeted quite a few charts tonight, but thought I’d pull some of the key ones together with some commentary for readers. A full deck of quarterly charts will go out to subscribers to the Jackdaw Research Quarterly Decks Service in the next few days as Apple releases its full data in an SEC filing, so look out for that if you’re a subscriber, and sign up here if you’re not.

Note: in this post, as in all my posts, I use calendar quarters for ease of comparisons with other companies and easy intelligibility by those not familiar with quirky fiscal years. As such, the labels and my commentary does not align with Apple’s fiscal calendar.

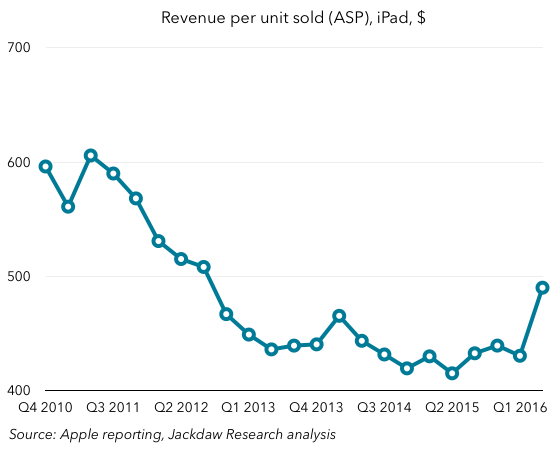

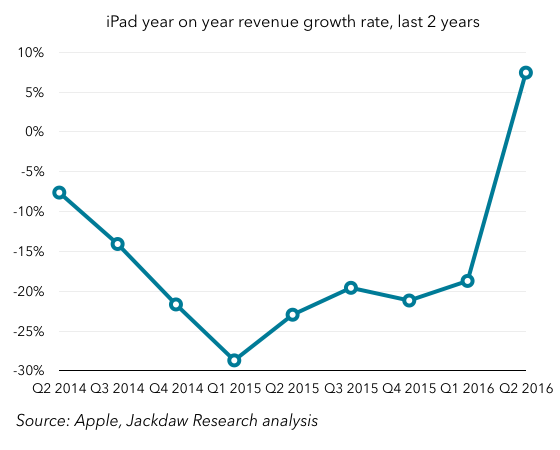

iPad returns to revenue (but not shipment) growth)

Last quarter, Tim Cook promised that the iPad would have its best year on year “compare” in over two years, which by my calculations meant something better than an 8% decline. Turns out iPad revenues actually returned to positive growth this quarter, though shipments still dropped, thanks to a really strong boost in ASPs:

That iPad ASP growth seems to have been driven by the launch of the iPad Pro, which in turn was likely designed in large part to drive higher ASPs as shipment growth has stalled. In other words, the strategy seems to be working. It’s also interesting that Apple reported that half iPad Pro sales went to people buying them for work, which is another validation of Apple’s strategy, but also points to a big opportunity for Apple, which is selling more devices into the enterprise, both to individual and corporate buyers. That’s something I first talked about in the context of Apple’s IBM deal, but it goes much further than that (as evidenced by subsequent Cisco and SAP deals).

That iPad ASP growth seems to have been driven by the launch of the iPad Pro, which in turn was likely designed in large part to drive higher ASPs as shipment growth has stalled. In other words, the strategy seems to be working. It’s also interesting that Apple reported that half iPad Pro sales went to people buying them for work, which is another validation of Apple’s strategy, but also points to a big opportunity for Apple, which is selling more devices into the enterprise, both to individual and corporate buyers. That’s something I first talked about in the context of Apple’s IBM deal, but it goes much further than that (as evidenced by subsequent Cisco and SAP deals).

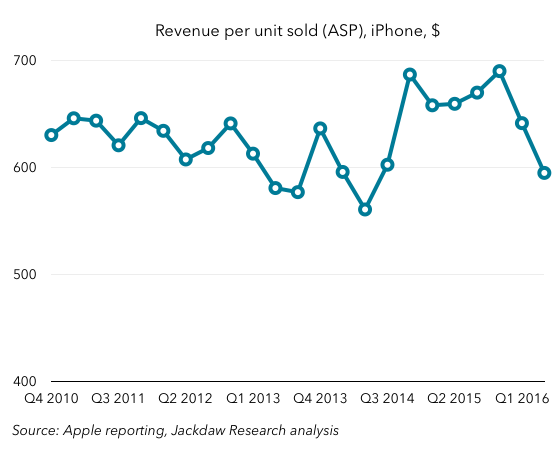

iPhone sales and ASPs down – the iPhone SE effect

Unsurprisingly, iPhone sales were down again, though perhaps not as badly as they seemed to be given the changes in inventory. But the most notable thing was the drop in average selling prices – the opposite of what happened with the iPad in the quarter: Just as the positive change in iPad ASPs was due to the successful launch of a new product (the 9.7″ iPad Pro), so is the larger than usual quarterly drop in iPhone ASPs due at least in part to the launch of a new product – the iPhone SE. It’s not all that – there was some impact from the inventory changes, as mentioned on the earnings call – but the magnitude of the drop is an indication that the iPhone SE has also had a successful launch, and has been something of a hit. That’s a good thing, in that these sales have filled something of a hole in iPhone sales in the quarter – which was arguably the purpose – while proving that Apple can tap into a market for iPhones at a lower price point with slightly lower specs and feature functionality.

Just as the positive change in iPad ASPs was due to the successful launch of a new product (the 9.7″ iPad Pro), so is the larger than usual quarterly drop in iPhone ASPs due at least in part to the launch of a new product – the iPhone SE. It’s not all that – there was some impact from the inventory changes, as mentioned on the earnings call – but the magnitude of the drop is an indication that the iPhone SE has also had a successful launch, and has been something of a hit. That’s a good thing, in that these sales have filled something of a hole in iPhone sales in the quarter – which was arguably the purpose – while proving that Apple can tap into a market for iPhones at a lower price point with slightly lower specs and feature functionality.

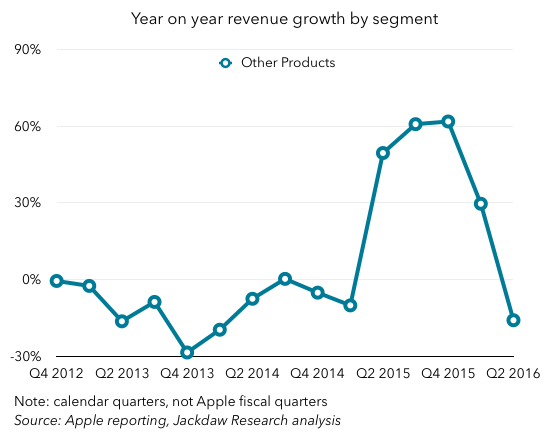

Apple Watch and Other Products

One last interesting point with regard to a specific product: the Apple Watch. It’s buried in Other Products, but perhaps a better way to look at it is that it now leads the Other Products category, which otherwise features a number of other smaller products. That’s been a double-edged sword for the reporting category over the past 18 months or so, as Apple Watch has first driven higher growth and now is driving negative growth for the category again: This is, to some extent, a temporary anomaly due to the launch of a brand new product and the subsequent (presumed) shift to a different time of year for the follow-up product as the second version of the Apple Watch launches in the fall. But it’s an indication of just how important the Watch is to that Other Products category.

This is, to some extent, a temporary anomaly due to the launch of a brand new product and the subsequent (presumed) shift to a different time of year for the follow-up product as the second version of the Apple Watch launches in the fall. But it’s an indication of just how important the Watch is to that Other Products category.

Short-term versus long-term

In concluding, I’m going to link back to my post last quarter, in which I both reviewed the good news and bad news in the results and looked forward to the rest of the year. The point remains the same: with Apple there are two current pictures, which are very different. On the one hand, there’s the short-term picture, characterized by the anniversary of massive growth in iPhone sales driven by the iPhone 6, and also an unusually long lull in the Mac upgrade cycle driven by delays in getting new chips from Intel. That short-term picture hasn’t changed, and is so far fairly predictable.

The bigger question, though, is what happens later this year as some of the unpleasant short-term factors start to go away. As I said last quarter, with the iPad performing better, that’s the first of those positive levers coming into effect, and if that higher ASP trend continues, that will be more grist to the mill. However, the far bigger effect obviously comes from the iPhone, which I still believe might return to revenue growth later this year or early next year. Lastly, the other major product lines – Mac and Apple Watch – have potential to contribute further to that growth. We should finally see new Macs in the fall if not before, which will unleash significant pent-up demand, while new Apple Watches combined with a much more capable watchOS 3 could drive more sales there. In other words, over the long term I remain very bullish about Apple’s prospects, and we could start to see signs of that in the September quarter, but especially in the December quarter and beyond.