This week marks the fifth anniversary of Tim Cook’s appointment as permanent CEO at Apple – he was appointed CEO on August 24th, 2011. As a result, we’ll no doubt see quite a few retrospectives this week looking back over his time at Apple, and evaluating his tenure. As context for that analysis, I wanted to share some numbers about Apple in the quarter and year before he took over, and compare it with numbers for the quarter and year ending in June of this year. Not all the applicable data sets go back that far – Apple has changed its reporting segments in at least a couple of ways during this five year period, but we’ll mostly try to compare before and after as closely as possible.

Note: here as in all the analysis on this blog, I use calendar quarters rather than companies’ fiscal quarters for analysis for ease of comprehension by those not familiar with companies’ fiscal calendars – hence, Q2 2016 is the June quarter recently ended and reported. Many of the charts shown here are part of the Apple quarterly deck which is available as part of the Jackdaw Research Quarterly Decks Service, which you can read more about here. The underlying data is also available on a custom basis as either a one-off delivery or a quarterly service – please contact me for more information.

P&L measures

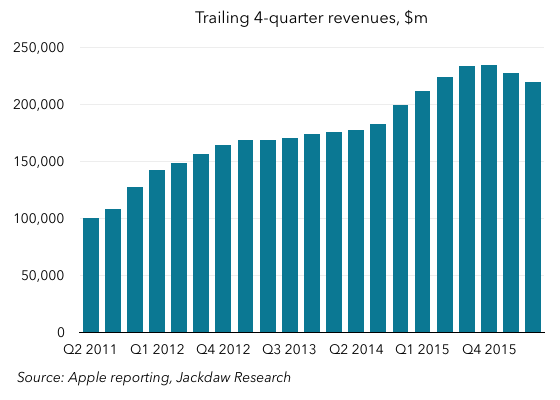

Let’s start with the corporate income statement. By any measure, Apple is simply a lot larger than it was five years ago. Here are trailing 4-quarter revenues:

Revenues in the four quarters before Tim Cook was appointed were $100 billion, whereas in the last four quarters they were over $200 billion. However, as you can see from the chart, it hasn’t been an inexorable rise up and to the right. Revenues grew very strongly in that first period, then began to level off somewhat throughout 2012 and 2013, then spiked following the iPhone 6 launch. And of course over the past year revenue growth has been negative for the first time in many years at Apple. The overall effect is still a more than doubling of total revenue, but the current trajectory is negative. As I’ve written previously, I continue to believe that we’ll see a reversal of this trend in the next few quarters as a combination of factors kicks in, but I’m betting Tim Cook would have rather his 5 year anniversary would have fallen either side of this lull instead of in the middle of it.

Meanwhile, margins have been up and down over time, with a bump in the early part of Tim Cook’s time at the helm, followed by a drop down to slightly lower levels, a steady rise, and then a drop off again:

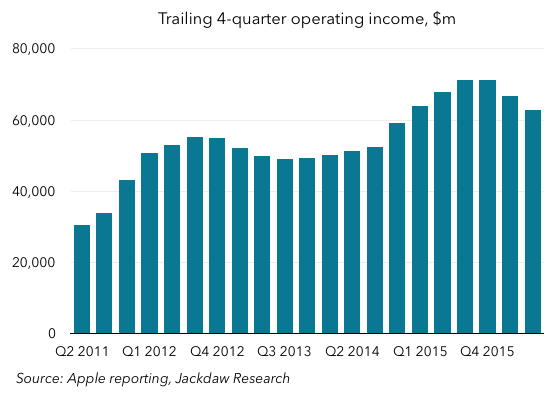

The ups and downs here largely correlate to overall growth rates for Apple, with higher revenue growth rates driving higher margins for a time as cost expansion takes a while to catch up with revenue growth, only to fall again as growth slows. On operating and net margin, Apple has ended these five years slightly below where it started, whereas on gross margin it’s in more or less the same place. But it’s worth noting that dollar profits are still way up on where they were, and that’s the metric that Apple and its investors are likely more focused on:

Yes, there’s the same up-and-down pattern, but again operating income on a twelve-month basis is roughly twice what it was five years ago over the past year.

R&D spend has ballooned

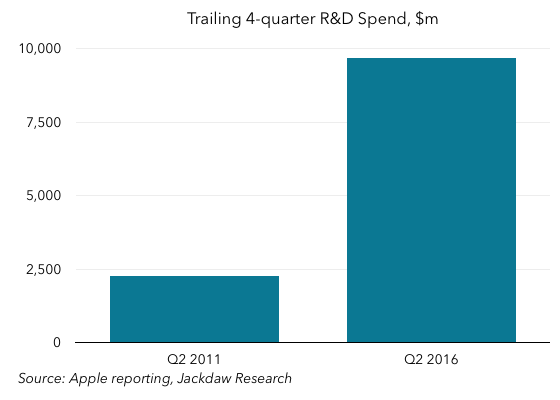

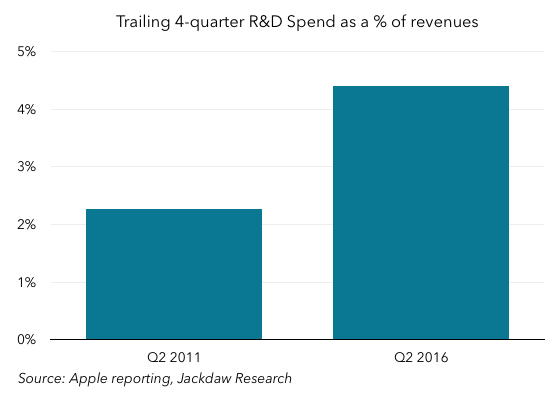

The only other line from the income statement I want to zero in on is research and development spending, because there’s been a fairly dramatic change here over the past five years. Here’s total R&D spend in dollars on a twelve-month basis, and spending as a percentage of revenue:

R&D spend was under $2.5 billion the four quarters before Tim Cook took over, but it was almost $10 billion five years later, a roughly fourfold increase. And that’s not just because Apple’s revenue has grown during that time – R&D has actually grown significantly as a percentage of revenue over the same period, going from just over 2% to just over 4%, or almost doubling as a percentage. That’s interesting, because R&D actually fell fairly consistently as a percentage of revenue during most of Steve Jobs’ second stint as Apple CEO, from a peak of 8% in 2001 and 2002 all the way down to 2% just before Cook took over. That’s largely a function of the massive iPod- and iPhone-driven revenue growth during that period – dollar R&D spend rose from around $400 million a year to over $2 billion a year during the same time period – but it’s interesting to note that Cook has reversed the trend and significantly increased R&D spend even above and beyond the rate at which revenue has grown. Interestingly, that 2 percentage point increase in R&D spend is roughly equal to the 2 percentage point drop in margins during the Tim Cook era.

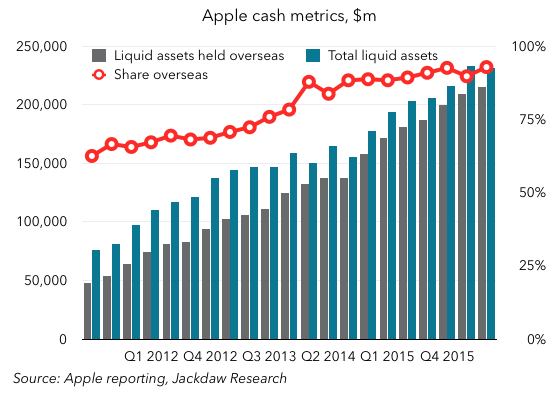

The cash hoard grows

The other major corporate financial metric that’s worth a quick look is cash. Apple’s cash and investment assets have grown enormously over the past five years, as the two charts below show:

The starting and ending totals are easier to see in the second chart, but the steady growth is perhaps easier to see in the first. Regardless, Apple ended calendar Q2 2011 with a total balance of cash and investments of $76 billion, while it ended Q2 2016 with a balance of $231.5 billion. In other words, it has added over $155 billion to its coffers over this time. Meanwhile, an increasing proportion of this cash and investments has been held overseas – the percentage was 63% five years ago, but was 93% at the end of Q2 2016.

Of course, the other cash-related metric worth noting during the first five years of the Cook era is the way Apple has been using that cash to pay dividends and buy back stock. Steve Jobs famously refused to pay dividends, but around a year into his tenure, Tim Cook instituted both these programs to return cash to shareholders. As of April of this year, Apple said it had “returned over $163 billion to shareholders, including $117 billion in share repurchases.” That makes the increase in its overall pile of cash and investments all the more remarkable.

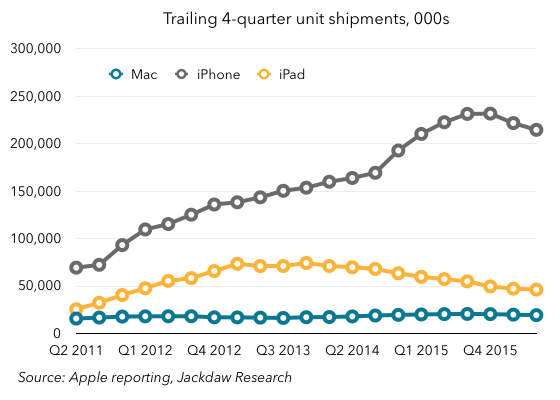

Unit shipments are up for iPhone, less so for other products

One of the most interesting things to look at in regard to the last five years is what’s happened to unit shipments for Apple’s three major product lines. The long-term trend is shown in this first chart:

Again, we’re all familiar with the trajectory of iPhone sales over recent years, so let’s be brief here. It’s worth noting that Tim Cook’s appointment coincided with the decision to move the launch date for new iPhones from June to the Fall, with the iPhone 4s launching in October of 2011. That explains the flat part at the beginning of the iPhone chart above. Following that shift, though, the iPhone saw strong growth in 2012 and 2013, but began to flatten out, only to spike in late 2014 and into 2015 thanks to the iPhone 6, then slumping a little in late 2015 and the first half of 2016. But again, it’s worth looking at the total numbers here. Apple shipped 69 million iPhones in the four quarters to Q2 2011, and shipped 214 million in the most recent four quarters. That’s a massive expansion of Apple’s business here, despite the recent lull (shipments peaked at 231.5 million on a twelve month basis in Q4 2015).

It’s also interesting to note that Apple has shipped 859 million iPhones during the Tim Cook era, compared with just 130 million in the pre-Cook era. In other words, roughly 87% of the almost one billion iPhones Apple has ever sold have been sold during Tim Cook’s time as permanent CEO.

What’s almost more interesting, though, is what’s happened to Mac and iPad sales, which performed roughly the same in the most recent quarter as they did five years ago:

As you can see, both Mac and iPad sales were up just a few hundred thousand on those from five years earlier, despite the doubling of iPhone sales over the same period. As the earlier chart shows, for iPads that’s because sales first grew significantly, peaking at 26 million quarterly and 74 million over twelve months in Q4 2013 and falling since. Mac sales, too, have had better quarters than the most recent one, though the peak was not much higher than today. Both products are due for something of a rebound in the coming quarters, as new Mac are (hopefully) finally introduced and the iPad Pro trend continues to help sales. And it’s worth noting that 300 of the roughly 330 million total iPads sold to date have been sold under Tim Cook, along with almost 112 million Macs.

Of course, we don’t have official shipment numbers for the Apple Watch, though there are various estimates out there. But it would be inappropriate to skip over that product entirely – it was the first brand-new product introduced in the Tim Cook era, and likely sold around 15 million units in its first year on the market. That’s a much faster run-rate than the iPhone, but down a little at this point on iPad sales in their first year. But it’s interesting that, as Tim Cook marks his five year anniversary, we’re seeing another product whose launch timeframe is being moved from the first half to the second half of the year, causing something of a lull in sales in the meantime.

A changing mix of segment revenues

All that movement in unit shipments obviously flows through to product revenues too. The revenue split by segment has changed fairly significantly over Tim Cook’s tenure. Apple’s financial reporting by segment has also changed over the last five years, with the iPod no longer separated out as its own reporting line, the Accessories bucket being merged with iPod, Apple Watch, Apple into “Other Products” and “iTunes, Software, and Services” becoming just “Services”. In the chart below, I’ve collapsed these segments for comparability:

The iPhone, which was already a very significant portion of Apple’s overall revenue, has only become more dominant over the past five years, rising from 45% of revenue in the twelve months to Q2 2011 to 64% in the year to Q2 2016. But other components have also risen or fallen – iPad has dropped from 16% to 9% and Mac from 20% to 11%, while the combination of iPod, accessories, and various other hardware products has dropped quite a bit too. The only other segment that’s risen as a portion of the total during this time – despite the rapid growth of iPhone revenues – is Services. An increase from 9% to 10% of revenue doesn’t look like much, but it’s much more impressive when you look at the dollar amounts instead:

What’s now the Services segment has grown from under $10 billion in the twelve months to Q2 2011 to well over $20 billion in the most recent twelve months, with the trajectory actually steepening in recent quarters. Yes, it’s still just 10% of total revenue over the past year, but it’s actually Apple’s fastest-growing segment at the moment.

The other interesting thing to look at in the context of segment revenue is the difference between unit shipments and revenue performance, which is driven by changing average selling prices (ASPs). You can see it a little in iPhone revenues:

By now, that iPhone trajectory should be familiar, but it’s worth noting the growth – from just over $40 billion on a twelve-month basis to $140 billion. It’s subtle, but the 3.1x growth in shipments has translated into a 3.5x growth in revenue, and that’s largely down to ASPs. Here are average selling prices on a trailing 4-quarter basis for the three major product lines at the beginning and end of Tim Cook’s first five years – note that because of changes in reporting structures I’ve used Q3 rather than Q2 2011 as the starting point here:

By now, that iPhone trajectory should be familiar, but it’s worth noting the growth – from just over $40 billion on a twelve-month basis to $140 billion. It’s subtle, but the 3.1x growth in shipments has translated into a 3.5x growth in revenue, and that’s largely down to ASPs. Here are average selling prices on a trailing 4-quarter basis for the three major product lines at the beginning and end of Tim Cook’s first five years – note that because of changes in reporting structures I’ve used Q3 rather than Q2 2011 as the starting point here:

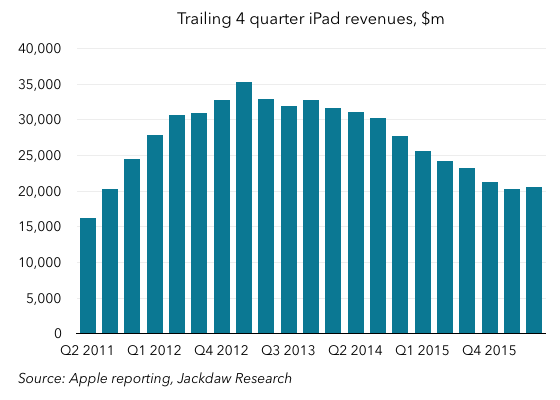

As you can see, iPhone ASPs have risen over the five years despite the increasing maturity of the product and the introduction of two cheaper models (the iPhone 5c and more recently the iPhone SE). Mac ASPs have dropped, but only slightly, while iPad ASPs have dropped fairly significantly, driven by the launch of the iPad Mini in 2012 and the increasing tendency to keep older devices in the lineup for longer at lower prices. But something interesting has been happening to iPad revenues in recent quarters, even as shipments continue to fall year on year:

This flattening of revenues, and the growth this past quarter, has been driven by the iPad Pro, which has raised ASPs considerably. iPad ASPs bottomed out at around $415 a year ago, but were $490 in Q2 2016, up $60 from Q1, putting them back at late 2012 levels.

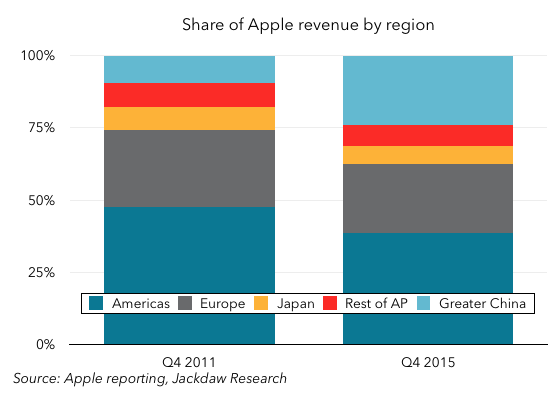

Regional trends and the rise of China

One of the most dramatic changes at Apple in the Tim Cook era has been the rise of China as one of its two major markets. Here, again, unfortunately, we’re thwarted a little by a change in Apple’s reporting a few years back, in which it eliminated Retail as a separate segment and rolled it into the individual regions, so we’re going to use Q4 rather than Q2 2011 as our starting point, and for comparability we’ll use Q4 2015 as the end point. As such, we’re measuring a four-year rather than five-year period, but the changes are still very visible. Here’s the share of Apple’s revenue by region at those two points in time:

As you can see, Greater China has increased massively as a proportion of revenue over this period, going from 10% to 24% of revenues, while every other region has shrunk in percentage terms. In Q4 2015, Greater China contributed the same percentage of revenue as Europe. Looking at the dollar amounts is again helpful – here’s actual revenue by region for those two quarters:

It’s worth noting first that every region has grown during these four years, but Greater China has clearly grown far faster than any other region, from $4.5 billion to over $18 billion during this time. That’s massive growth, and I’d say it’s one of Tim Cook’s great achievements during his tenure. It’s also clearly something he hasn’t given up on, given his recent frequent visits to China and the investments in Didi and in an R&D center to be built there. It’s also worth looking at operating income by geography, because here too China has made a significant contribution:

Retail is far more international

I want to close out with Apple’s retail business, which gets less attention in Apple’s official reporting than it used to, since Retail has been wrapped into the regions, but is as important to Apple’s strategy as ever. And Tim Cook has been instrumental in expanding the Retail footprint, especially overseas, though Retail has also been the focal point of arguably Cook’s biggest blunder as CEO – the appointment of John Browett to run the business. However, Angela Ahrendts’ appointment seems to have more than made up for that mistake.

Here are a couple of charts about Apple’s retail footprint:

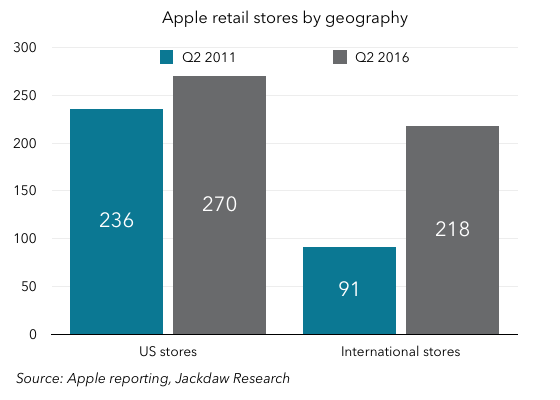

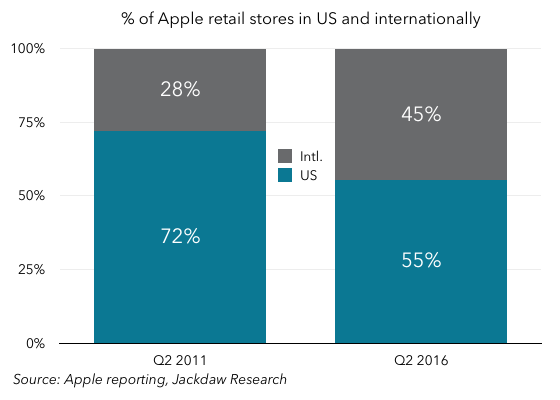

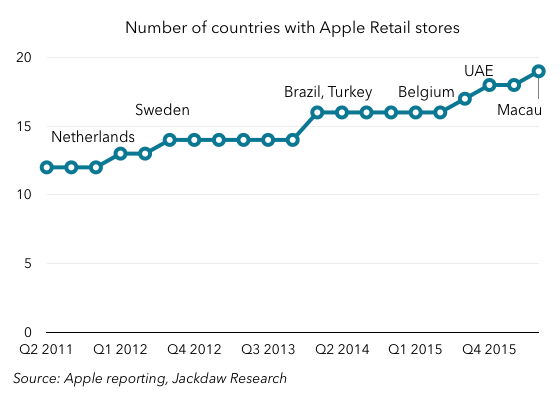

At the end of Q2 2011, Apple had a total of 327 retail stores, of which 270 or 72% were in the US. By the end of Q2 2016, Apple had 488 stores globally, of which 218 or 45% were now overseas. Tim Cook’s time as CEO has seen Apple stores opened in seven new countries across four continents: But of course it’s also seen a massive expansion in the number of Apple stores in China, which had 36 stores as of the end of July, up from single digits when Tim Cook took over.

But of course it’s also seen a massive expansion in the number of Apple stores in China, which had 36 stores as of the end of July, up from single digits when Tim Cook took over.

Conclusions

I’ve deliberately made this more of a factual post than an evaluation of Tim Cook’s tenure – as I said up front, this week will see lots of this sort of stuff, and I’ve already talked to several reporters doing their best to sum up five years of work in a few hundred words. But I think it’s worth noting several things here, some of which I’ve mentioned in the text:

- Apple under Tim Cook has sold far more iPhones and iPads than it ever did under Steve Jobs – 87% of total iPhones sold and 90% of iPads ever sold. Though Steve Jobs launched these products, it was always Tim Cook who ensured the supply chain met demand as well as possible, and it’s been Tim Cook who’s overseen the massive expansion in that supply chain over the last five years as the scale has grown to something unprecedented.

- Tim Cook has made the decision to increase Apple’s spending on research and development not just in dollar terms commensurate with revenue growth but actually doubling it as a percentage of revenue during his tenure despite the massive growth in revenue. That reversed the trend under Steve Jobs, and the increased investment in R&D is roughly equivalent to the drop in margins during this time – Cook has made a massive bet on R&D and by implication on future products.

- Cook has made China a special focus, and this focus has paid off in a big way, with a roughly fourfold increase in revenue from Greater China and an equivalent increase in operating income. Greater China has grown from 10% of revenues to roughly a quarter, and Apple’s retail footprint there has also grown dramatically. That growth in China has been a major contributor to Apple’s overall growth in the last five years, and Cook clearly remains committed to China as a focus for Apple as evidenced by his recent investments there. He’s begun to talk more about India and its potential, but I remain skeptical that India can be much more than a rounding error for Apple over the next few years.

- Only one entirely new hardware product has launched under Tim Cook, and yet we have almost no official data to go on to evaluate the performance of the Apple Watch so far. Opinion remains divided about how to evaluate the Watch, but I’m on the side of those who considers it a modest success in Apple terms and a smash hit in the context of the market into which it was launched. Like the iPhone the year Tim Cook took over, it’s going through an interesting transition as its release moves from the first half to the second half of the year, but I suspect that like the iPhone in late 2011, the Watch is due for big growth in late 2016 and beyond.

- I suspect the transformation we’ve seen in Services, driven largely to date by the App Store and latterly by Apple Music, is just the start of what we’ll see under Tim Cook. He’s already hinted several times at additional services to come, and TV is an obvious focus here. But I also think some of the rhetoric about Services has been overblown – it’s still only 10% of revenue, and unlikely to grow massively past that point unless Apple decouples services from its devices, which I think would be a mistake.

Perhaps one of the most significant contributions Tim Cook has made at Apple can’t be seen in any of these charts, because it’s about the changes to Apple’s culture that have happened under his leadership. The increased openness, best exemplified by the frequent interviews Cook and other executives now regularly grant to various publications (and even podcasters), is one element of this, though Apple’s secrecy about future products remains as tight as ever. But an increased sense of social responsibility, especially as regards the environment and contributions to social causes is another major change. This doesn’t have a direct financial impact, but it’s made a positive contribution nonetheless, and no evaluation of Cook’s tenure would be complete without a recognition of that fact.

{kind=link}