After a couple of weeks on vacation, I’m still playing catchup with some of the tech earnings reports that came out while I was gone. Today, I’m tackling an interesting aspect of Alphabet’s earnings, which is the increasing dominance of ad revenue from Google’s own properties versus revenue from third party sites as a proportion of its total ad revenues. The charts I’m using here are largely taken from the Alphabet deck in the Jackdaw Research Quarterly Decks Service, which you can sign up for here. We also discussed Alphabet earnings along with those of other major tech companies on this week’s Beyond Devices Podcast.

Some quick definitions

First off, some quick definitions. Google divides its ad revenue into two categories:

- Google websites – this includes all revenue from Google’s own websites, including AdWords revenue that is generated on Google.com, advertising revenue generated on YouTube, and advertising revenue generated from other Google owned and operated properties like Gmail, Finance, Maps, and Google Play.

- Google Network Members’ websites – this includes AdSense,

AdExchange, AdMob, All DoubleClick-related revenues including DoubleClick Bid Manager revenues, and Other Network products including AdSense for Domains.

Within the core Google segment, these two divisions plus the “Other” category make up the entirety of revenue, and ad revenue from these two sources makes up 90% of Google segment revenue.

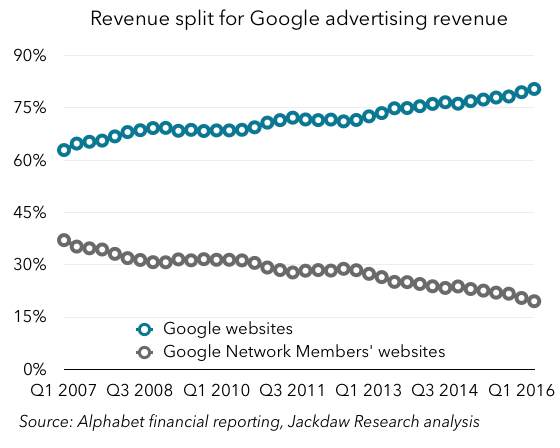

Very different growth rates lead to increasing dominance by Google’s own sites

These two segments have been growing at very different rates over the last several years, with Google’s own site revenue growing much faster than its Network Members’ ad revenues, as shown in the chart below:

Though there have been a couple of brief periods (in 2009-2010 and 2012) when Network revenue grew faster than Google website revenue, the pattern has otherwise been fairly consistent: Google’s revenue from its own sites has grown faster. Over the last three years, the gap has been significant – Google website revenue is up 74% over that period, while Network Members’ revenue is up just 17% over three years. That leads to a business that’s increasingly lopsided in favor of Google’s own sites:

In Q2 2016, Google sites passed 80% of total Google ad revenue for the first time. That’s up from 70% in 2011, and 60% around 2006.

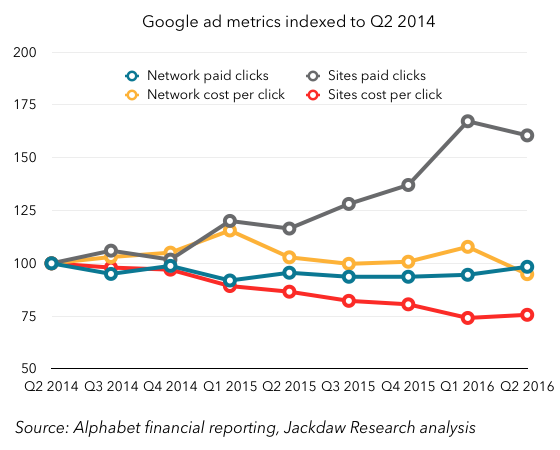

Paid clicks growth is the driver

The reason for this discrepancy becomes abundantly clear when you look at the ad metrics Google provides. Every quarter, it reports growth in the number of paid clicks and the cost-per-click (i.e. price) for both the Google sites business and the Network Members business. These numbers bounce around quite a bit, but I find it’s often helpful to index the numbers to a certain point in the past to see the longer-term trends. The chart below shows these figures indexed to the quarter two years ago, Q2 2014:

As you can see, there’s a stark contrast between the two businesses here. Let’s start with the number of paid clicks:

- Google sites paid clicks are up 61% over two years (the number was 67% last quarter)

- Network paid clicks are at 98% of where they were two years ago, and this number has been relatively flat over that whole period.

Google says that growth in clicks on its own sites has been driven by a combination of growth in the adoption of YouTube engagement ads, improvements in ad formats and delivery, and expansion of products, advertisers and user bases across all platforms, particularly mobile. There simply aren’t similar drivers for the Network business, which Google obviously doesn’t control as directly, and which is in some ways much more mature.

Looking at the cost per click:

- Google sites CPC in Q2 2016 was only 76% of the CPC for two years earlier

- Network CPC was 95% of two years earlier, and again this number has been relatively flat over the period, with modest growth in the first year, followed by slight shrinkage since.

The reason for the falling cost per click on Google’s own sites is largely due to growth in YouTube engagement ads where cost-per-click is lower than on Google’s other platforms, as well as changes in property and device mix, product mix, geographic mix, and ongoing product changes, with a smaller impact from currency exchange rates. Some of the same factors drove the modest recent decline in Network CPC as well.

Traffic Acquisition Costs and margins

This all matters a great deal for a couple of reasons, the second of which we’ll come onto in a moment. But the single most obvious reason is that the economics of ad revenue from Google’s own sites is radically different from the economics for Network sites, and that’s because of how Google pays for traffic. On third-party sites, Google pays out most of the revenue to the site owner, whereas on its own sites it keeps the vast majority of the revenue. Google breaks out the traffic acquisition costs (TAC) for both these segments, and the stark differences are shown in the chart below:

As you can see, in the Network business, Google pays out at a rate very similar to the economics of the major app stores, at about 70% of revenue. For its own sites, however, Google’s TAC is a fraction of that, at around 9% in Q2 2016. These payments go to the sources of traffic to Google’s various websites, principally makers of browsers including Apple’s Safari which feature Google as a default search engine.

Interestingly, Network TAC had come down quite a bit for several years, but has recently spiked back up a little, though it’s been within a range from 67-71% for the last five years. Conversely, Google’s TAC for its own sites has been steadily rising, as its cut of revenues under various placement deals has been shrinking. With competition from Yahoo and Microsoft in particular rising over recent years, Google has had to pay more to retain its prime placement in various browsers.

Regardless of the recent changes, TAC remains far higher for third party sites than for Google’s own, though that’s not to say that this somehow translates directly into margins. Obviously, Google’s other costs for running its own sites are much higher than its cost for running ads on other people’s websites. But I suspect the increasing dominance of Google’s own sites as a source of ad revenue is driving the steady improvement in margins we’ve seen over recent years.

The downside of all this

Let’s turn now to the second reason all this matters. Though I’ve just said that the increasing dominance of Google’s ad revenues by money from its own sites is likely good for margins, there’s a downside here too. The problem with this dominance is that Google has to be responsible for essentially all the growth itself, largely by growing its direct audience and finding ways to sell more ads at higher prices. As we’ve already seen, YouTube has been a huge help here in recent years as monetization has really taken off, but I wonder how sustainable that growth will be over time. Google is already attempting to drive revenue through alternative business models like YouTube Red and other subscriptions, and I suspect we’ll see more of this.

But as long as Google is so heavily dependent on revenue from its own sites, it’s going to have to find new sources of revenue which it owns, which might well drive it to make acquisitions (Twitter, perhaps?) and organic investments in new properties. That may be challenging over time, especially as more and more online activity takes place on mobile devices, where there’s simply less room for ads. Better targeting and more lucrative formats like app install ads should help offset that a bit, but it may still be tough to sustain over time. Though Alphabet and Google’s recent results have been very positive, there is here still the core of a bear case against continued growth along the same lines.

Also published on Medium.