Snap Inc (maker of Snapchat) finally made its long-awaited S-1 filing public on Thursday evening. I’ve been dying to get my hands on this filing for months, and spent some time diving into it last night and digesting some of the numbers and other information in it. Here’s a quick summary of what I’ve found and some of my conclusions about Snap’s prospects going forward. Below, I’ve embedded a slide deck which shares many of the individual charts in this post and several more – it’s part of the Jackdaw Research Quarterly Decks Service, which offers similar decks on the most important consumer tech companies each quarter to subscribers.

Massive revenue growth

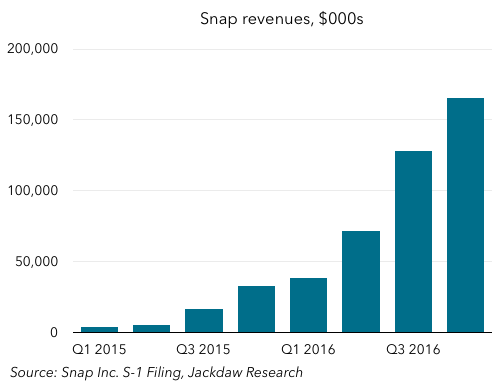

The first thing to note is that Snap is growing extremely fast from a revenue perspective. It showed its first ad in late 2014, and had its first meaningful revenue in 2015 (totaling $59 million), and then passed $400 million in revenue in 2016. The quarterly revenue picture is shown in the chart below.

That’s a very fast ramp, enabled by the fact that Snap held back on monetizing its base for several years following its founding in 2011. Facebook, by contrast, started to monetize the year it launched, and generated $382,000 in revenue in 2004. Its revenue ramp was slower ($9 million in 2005, $48 million in 2006, $153 million in 2007, $272 million in 2008, and $777 million in 2009), but it didn’t hit Snap’s current user scale until 2009. When Facebook turned on revenue generation, it had under 1 million MAUs, whereas when Snap showed its first ad it had 71 million daily active users.

ARPU growth a major enabler

The major driver of this ramp in revenues is rapid growth in average revenue per user (ARPU), as shown in the next chart:

Global ARPU has risen from 5 cents in Q1 2015 to $1.05 in Q4 2016, but the main driver has been revenue from North America, where ARPU was already $2.15 last quarter. The ARPU ramp in other regions has been much slower, with Europe generating just 28 cents per user per quarter in Q4, and the rest of world region just 15 cents. The one dollar ARPU isn’t far off Facebook’s global ARPU in Q1 2012, the last quarter it reported before its IPO, which was $1.21 globally. But its US & Canada ARPU was already up to $2.90 and its European ARPU at $1.40.

Still a very US-centric financial picture

The reality is that Snap’s business is still very US-centric when it comes to generating revenue. North America had 43% of its users, but generated 88% of its revenues in Q4 2016 (over 98% of that coming from the US). That could be seen as an opportunity for Snap to broaden its horizons and put more effort into monetizing Snapchat in other regions, driving up ARPU, but this may also be a sign that Snap simply hasn’t gained the same traction in other regions yet. It increased its sales and marketing headcount by 340% in 2016, so there’s a good chance it’s hiring in these other markets to drive higher ad sales there.

Profits are another story entirely

While Snap’s revenue picture is fairly clear, the bottom line is a lot less healthy – Snap is losing money by the truckload. This may be one of the first companies I’ve seen file for an IPO whose cost of revenue alone outweighs its revenue in the most recent financial year.

Most margins are literally off the charts

It literally makes no sense to include here one of my customary charts showing various margins over time, because both of the biggest ones – operating and net margins – have been at -100% or multiples of it throughout Snap’s reported history (the only time I’ve seen anything like it is when looking at Alphabet’s Other Bets segment). Gross margin is the only one which is anywhere near positive, and was positive in the second half of 2016:

Snap’s cost of revenue is made up of two larger buckets and some smaller ones – hosting costs are by far the largest, and those scale fairly directly with user growth. Snap doesn’t break these hosting costs out in detail, but they grew by $192 million in 2016, and total cost of revenue in 2016 was $452 million, so my guess is that hosting costs were around $300-350 million in 2016. Snap signed a deal in January with Google to extend its use of Google’s cloud infrastructure, which has a minimum revenue commitment of $400m for each of the next five years, so it’s a good bet Snap is expecting to spend at least that much in 2017.

The second largest, albeit much smaller, contributor to cost of revenues is Snap’s revenue share with its publisher partners. When Snap sells ads (which it did for 91% of its ad revenue in 2016), it gives publishers a cut, and this revenue share amounted to $58m in 2016, up from just under $10m in 2015. When partners sell the ads, they give Snap a cut, and it records only this net amount as revenue, so there’s no reported cost of revenue associated with that smaller chunk. The only other notable contributors to cost of revenue are content creation, where expenses rose $13m in 2016, and inventory for Spectacles, which only hit the books in late 2016.

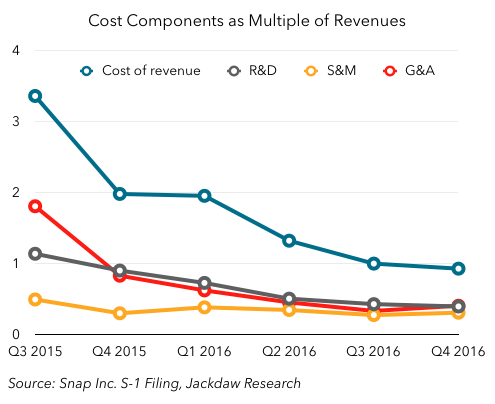

I usually like to include a chart on cost components as a percentage of revenue, but in Snap’s case it makes more sense to show them as a multiple of revenues, as for most of the company’s history that’s what they’ve been. The two charts below show first a zoomed out view over the whole of the reported period and then a slightly shorter-term view excluding total costs and expenses, to make it easier to see what’s happening in detail with some of these expense lines.

Because Snap is so early in its monetization effort, some of its cost components were multiple times its revenues even in late 2015, and its cost of revenue was still almost twice its revenue in Q1 2016. But as the charts above show, there’s been some real progress here, and R&D, Sales & Marketing, and General & Administrative costs are all under half of revenues now and falling. Snap still has a long way to go, though, before it can be profitable: cost of revenue needs to come down considerably as a percentage of revenue, and that means ramping up ARPU to better cover those massive hosting costs. The rest of the costs will continue to come down as a percentage of revenue as Snap scales, so profitability should improve steadily on that front assuming Snap can get back to strong growth (more on this below).

It’s worth remembering that, when Facebook IPO’d in May 2012, it had been net profitable for three years. Meanwhile, Snap’s prospectus says matter of factly, “We have incurred operating losses in the past, expect to incur operating losses in the future, and may never achieve or maintain profitability.” Though that profitability should come in time with scale and rising ARPU, it’s not a certainty. Twitter is another company which had its IPO at a time when it wasn’t profitable but it seemed a continuation of past rapid growth would carry it over the line soon, and yet it still isn’t in the black now (and in fairness, Twitter had a similar though slightly less bleak warning about its own profit prospects in its S-1).

User growth is a mixed bag

Snapchat reports only daily active users, and not monthly active users. That’s actually very sensible, and I always take it as a knock on Twitter that it refuses to give DAU figures – for an app that’s supposed to be a regular daily habit, monthly user numbers are a bit meaningless.

Linear annual growth

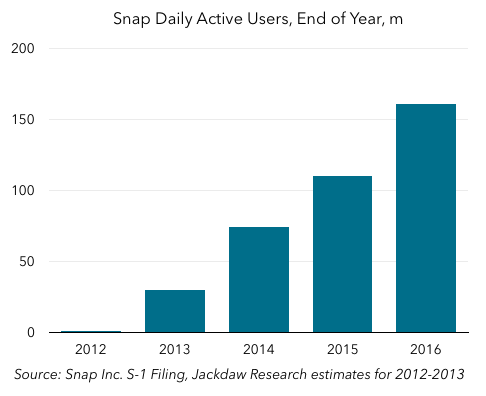

Daily active users have grown strongly over Snapchat’s history, as shown in the chart below, which shows the longer-term end of year picture, including some estimates based on milestones Snap provides in the S-1.

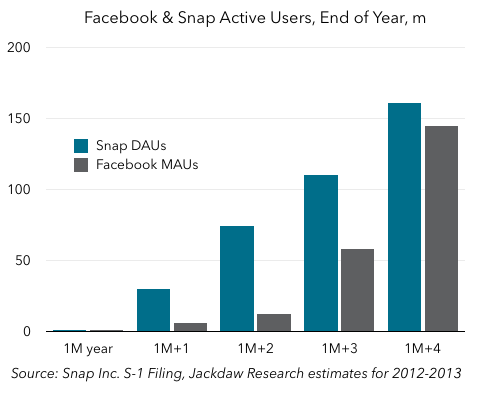

The annual picture is incredible – I don’t know when I’ve seen such a straight line for user growth from a base of almost zero (it was roughly a million at the end of 2012, and only a few thousand at the end of Snap’s first year, 2011). The chart below compares this growth to Facebook’s growth over a similar period. It’s worth noting that the Facebook number here is MAUs, whereas Snap’s is DAUs, but the comparison is striking:

I’ve aligned the timescales so that the years when the companies had 1 million users by their respective measures (2012 for Snapchat, and 2004 for Facebook) line up. As you can see, the start and end points are not far off from each other – 1m in the first year, and 161 versus 145 million in the fifth year, but the trajectory in-between is very different. Facebook saw the classic s-curve adoption, while Snap’s has been almost linear.

A much less straight line for quarterly growth

Things get a loss less linear when you look at quarterly growth numbers, as shown below.

There’s something of the s-curve in the first two thirds or so of the chart above, where growth appears to accelerate through late 2015 and early 2016, but it tapers off significantly in late 2016. What happened there depends on who you believe, as there are two possible explanations:

There’s something of the s-curve in the first two thirds or so of the chart above, where growth appears to accelerate through late 2015 and early 2016, but it tapers off significantly in late 2016. What happened there depends on who you believe, as there are two possible explanations:

- Snap’s own explanation is that a number of product improvements in late 2015 and early 2016 accelerated growth and brought forward some of the growth it would have seen later anyway, while in late 2016 it launched a version of its Android app which had some bugs and caused slower growth

- Third party data suggests that Snapchat began to slow down after Instagram launched its Stories feature, a clone of Snapchat’s own, which drove faster growth at Instagram and sucked usage and growth from Snapchat.

In fairness, Snap does acknowledge strong competition in the second half of 2016, but not Instagram specifically. Which explanation you believe is critically important for your view of Snap’s future prospects: if user growth really did slow down because of the competitive threat from Instagram, that isn’t going away, and in fact will only strengthen as Facebook brings Stories to the News Feed. If Snap can’t defend itself against such competitive threats, and if those threats cause an ongoing stagnation in user growth, it becomes a lot less appealing as an investment. On the other hand, if the issues really were a temporary combination of lumpy growth across the year and some Android glitches, that’s a much less gloomy statement about Snap’s future.

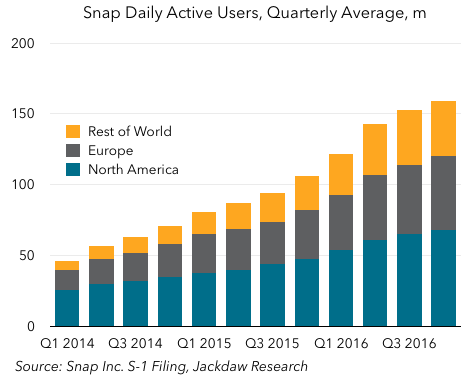

Differences by region

Where things get interesting is when you look at the regional breakdown of DAUs which Snap provides in the S-1 – the first of the charts below shows actual DAUs, while the second shows sequential growth in DAUs, both by region.

As you can see, there was an acceleration in late 2015 and early 2016 as Snap says, but there was also a slowdown in late 2016, though to very different extents in the regions. In North America and Europe, sequential growth in Q3 and Q4 was similar to its growth in the early part of the chart, but in the Rest of World region it dropped down to zero in Q4. Now, these figures are inherently lumpy – though they’re stated in whole millions of DAUs, the underlying numbers could be moving more subtly than these zigzag lines suggest, but there does seem to have been a meaningful slowing in Q3 and Q4, and that is worrying.

Terrible timing for the IPO

We won’t really know whether Snap’s explanation or the external explanation (or some combination of the two) is correct until we see another quarter or two of data from Snap on its user base. If it returns to strong growth in Q1 and Q2 of this year, investors can breathe a sigh of relief, but if it doesn’t, then the worries will continue, If I were a potential investor, I’d be very wary of making big commitments to Snap in a March IPO, before any of those figures are known.

The broader worry with Snap’s data here is that it really only provides DAU numbers as a measure of engagement. That’s better than MAUs, as I said above, but it still doesn’t tell you how engaged users are. This recent article in Bloomberg talks about the ways in which Snapchat fosters “streaks” by users, which drive them to open the app at least once a day, but which don’t necessarily drive meaningful engagement. The only deeper engagement stats Snap does provide relate to time spent and the number of times the app is opened – time spent across its base is 25-30 minutes on average, while the app is opened 18 times on average, with younger users skewing higher and older users skewing lower. But as Snap provides no longitudinal reporting on these data points, we have no idea how they’re trending over time and what that might tell us about real engagement.

For both investors and advertisers, knowing what engagement really looks like is critical, but that data is missing here. Snap badly needs user growth along with rising ARPU if it’s to make progress towards profitability, and at this point the user growth side of the equation is uncertain, though ARPU looks to be on a healthier trajectory. Put another way, the timing of this IPO couldn’t be worse – rather than coming at a time of strong, consistent growth, it comes at the first time in Snap’s history when it’s showing signs of significant weakness.