Lenovo reported this week that it had just concluded a tough quarter, and was going to be taking actions to streamline its business and operations, including laying off a significant number of employees and cutting costs in the mobile business in particular. This post runs through some of the components of Lenovo’s tough quarter and examines where the business is likely to go from here.

Note: this is my second post on Lenovo – the first was on its Q4 2014 results, the first it reported after acquiring Motorola. Please note also that in this post as elsewhere on this blog I use calendar quarters for ease of comprehension and comparison, even when companies’ fiscal years are different.

Motorola has been a great defense against shrinking sales in China

I believe the Motorola acquisition was originally contemplated as a way for Lenovo to build scale and especially to break into some new markets. However, it’s turned out to be a phenomenal defensive strategy against some significantly worsening trends in Lenovo’s largest smartphone market, China. As part of Lenovo’s quarterly results presentation, it shared these numbers – sourced to SINO – on smartphone sales in China, and they provide a great context for Lenovo’s problems domestically (this is my chart, based on the same numbers):

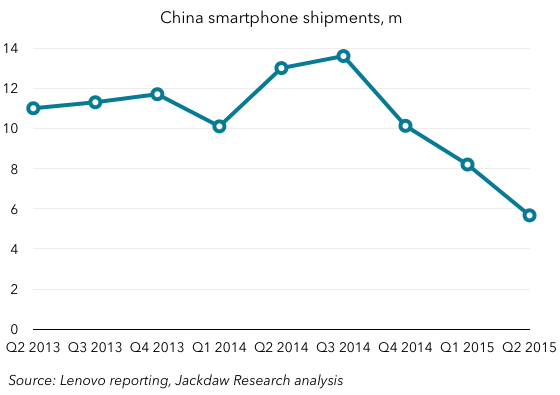

There are two important trends to note here: firstly, total sales (shown in red) have declined in the past year; secondly, subsidized sales (shown in blue) have declined even more strongly, and are shrinking as a share of total sales. The fact that the Chinese smartphone market is shrinking is bad enough, but Lenovo is particularly exposed to that carrier-subsidized segment, which is rapidly going away as carriers discontinue subsidies under pressure from the government. The result is that Lenovo’s Chinese smartphone sales are shrinking rapidly:

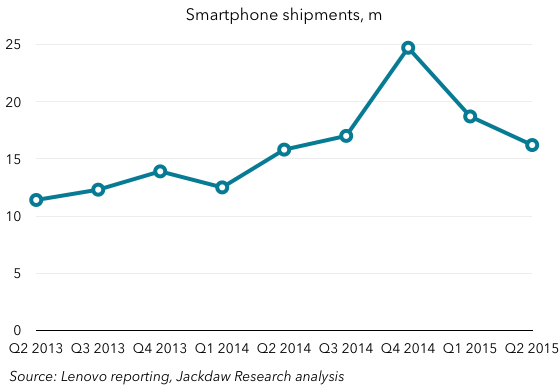

There are two important trends to note here: firstly, total sales (shown in red) have declined in the past year; secondly, subsidized sales (shown in blue) have declined even more strongly, and are shrinking as a share of total sales. The fact that the Chinese smartphone market is shrinking is bad enough, but Lenovo is particularly exposed to that carrier-subsidized segment, which is rapidly going away as carriers discontinue subsidies under pressure from the government. The result is that Lenovo’s Chinese smartphone sales are shrinking rapidly: Lenovo’s smartphone shipments in China peaked at almost 14 million in Q3 2014, and have fallen steadily since, to just under 5 million in Q2 2015. Were it not for the addition of Motorola’s smartphone sales, Lenovo would have seen a serious dent put in its overall sales. As it is, things don’t look quite so bad overall from a shipment perspective, though sales have still declined over the past two quarters:

Lenovo’s smartphone shipments in China peaked at almost 14 million in Q3 2014, and have fallen steadily since, to just under 5 million in Q2 2015. Were it not for the addition of Motorola’s smartphone sales, Lenovo would have seen a serious dent put in its overall sales. As it is, things don’t look quite so bad overall from a shipment perspective, though sales have still declined over the past two quarters: Without the Motorola business, Lenovo’s smartphone shipments overall would have fallen from 15.8 million in Q2 2014 to just 10.3 million a year later.

Without the Motorola business, Lenovo’s smartphone shipments overall would have fallen from 15.8 million in Q2 2014 to just 10.3 million a year later.

But Motorola is also dragging down profits

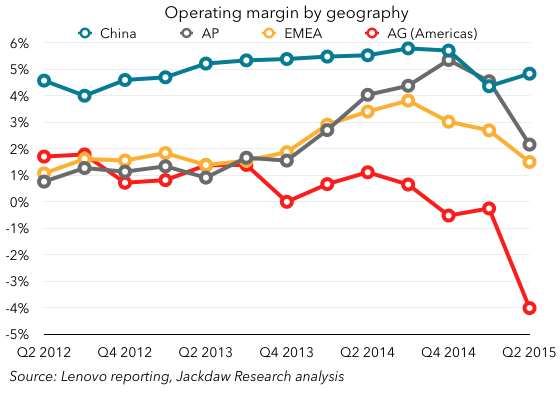

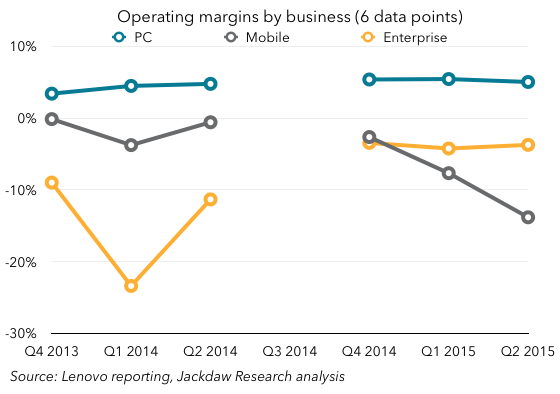

The problem is that, while Motorola’s shipment numbers have been a great benefit to overall shipments, its financials continue to be a drag on the business. It’s hard to isolate Motorola’s performance within the overall numbers reported by Lenovo, but there are hints when you look at Lenovo’s operating margins by geography and by segment, where Motorola’s results disproportionately affect the Americas and Mobile respectively:

Note: Lenovo changed its reporting segments in Q4 2014, and as such we’re missing operating income by segment for Q3 2014 until it reports them with Q3 2015 figures next quarter.

Note: Lenovo changed its reporting segments in Q4 2014, and as such we’re missing operating income by segment for Q3 2014 until it reports them with Q3 2015 figures next quarter.

As you can see, both the Americas and the Mobile segment saw significant declines over the last few quarters as Motorola joined the company. Economic conditions in Brazil particularly impacted the Motorola business but also affected other parts of the business, so that’s part of the reason for the sudden drop in Americas margins. However, Motorola was unprofitable when it joined, and it continues to be so. In fact, Lenovo just subtly changed its profitability target from having the Motorola business be profitable in 4-6 quarters after acquisition to having the total Mobile segment of which Motorola is a part be profitable, a recognition that it’s going to take longer to turn the Motorola business around.

In PCs and tablets, growing share in shrinking markets

I’m not going to spend as much time on PCs and tablets as on smartphones, but I did want to note that in these two categories Lenovo’s challenge is a bit different. The markets themselves are shrinking, so even though Lenovo’s share of both markets is growing, that’s not delivering strong growth overall. In fact, PC shipments dropped several percentage points year on year, while tablet shipments only grew modestly. If growth trends in the PC market continue to worsen, even Lenovo’s significant outperformance of the market won’t help it, while its tablet sales are too small to help offset the challenging conditions in smartphones and PCs.

Lenovo’s proposed solution is familiar

We’ve heard it so many times over the last several years from different Android vendors that Lenovo’s proposed solution to what ails it in in the smartphone market is very familiar: streamlining and simplifying the product portfolio, while making the smaller number of models more compelling and better differentiated. Samsung, HTC, LG, Sony and others have all embraced this strategy over the last few years, and while it’s likely a good idea, none of those companies have seen significant turnarounds as a result, and all continue to struggle to a greater or lesser extent in selling smartphones.

However, Lenovo is also taking some other steps to turn its performance around, cutting its workforce, and moving to what sounds like single sales and product organizations. Interestingly, it’s largely focused on the Lenovo sales organization (though it’ll presumably keep some Motorola staff on in key markets like North America where Lenovo has never had a presence), and the Motorola product design, development, and manufacturing organization. Earlier, it was cautious about consolidating the two manufacturing organizations in particular, and it’s intriguing to see the company consolidating around the Motorola function rather than the Lenovo equivalent. It will be interesting to see to what extent the Lenovo and Motorola brands continue to be marketed distinctly if both sets of devices are coming from the same team.

At the same time, Lenovo is also embracing new channels domestically, mimicking Xiaomi in its pursuit of the online model with the launch of the ShenQi online store this past quarter and the ZUK Z1 phone in August through that channel. This makes tons of sense given the shift in purchasing from one channel to the other, but it’s not yet clear that Lenovo has the competencies required to pull this model off.

There are also hints in Lenovo’s press release that it might seek to acquire other PC businesses as a way to further grow scale while driving cost efficiencies. The key quote here is:

Accelerating the drive for 30 percent share in PCs by better taking advantage of consolidation, while becoming even more efficient and reducing costs to ensure sustainable, profitable growth.

That may mean something else, but it certainly sounds as if it could be referring to an acquisition strategy in the PC market.

Where does Lenovo go from here?

Given the tough domestic conditions, it’s going to be hard for Lenovo to turn its performance in China around dramatically, which makes its rest-of-world strategy all the more important. But though the addition of Motorola made for favorable year on year comparisons, the Motorola business itself actually shrank year on year in terms of shipments, from 7.7m in Q2 last year to 5.9m this quarter. Motorola has had real success with its low end devices, the Moto E and Moto G, but that success has come to a great extent in certain markets that are now facing challenging conditions too. Brazil is perhaps the best example – Lenovo sold just 167,000 smartphones there in Q2 last year, but the combined company sold around 2.5 million smartphones there in Q2 2015, and yet this turned out to be something of a liability this quarter as conditions worsened. Latin America as a whole accounted for 3.7 million shipments, and if the economies there continue to struggle, that likely doesn’t bode well for Lenovo.

With these headwinds in key markets like China and Latin America, Lenovo needs to do better in other regions, but those regions are relatively small for the company today, with just 1.4m shipments in North America and 2.8m in EMEA in Q2. Lenovo is heavily dependent on the BRIC countries, which account for over 60% of its smartphone shipments today. And yet the Motorola brand has been struggling in the US, its erstwhile stronghold, for several years now. What’s selling is the low-end smartphones, with an average selling price for Lenovo as a whole of a little over $100, and Motorola’s ASP around $200.

I’ve been quite bullish about Lenovo until now, but at the moment I’m less certain on its prospects for the short to medium term, especially if things don’t change domestically. But Lenovo isn’t alone in this – it’s been caught up in the perfect storm that’s affecting many of the major Android vendors, and that’s been causing a number of them to announce significant cuts in their businesses in recent weeks. The good news is that PC margins continue to be relatively healthy (at least in the context of the broader Windows PC market), and PCs represent the majority of Lenovo’s business today. But if Lenovo really wants to follow through on its strategy of becoming a major player across these device categories, it’s going to have to find a way to turn its smartphone performance around.

Why do I bring this up? Well, given Andromeda is also the name of the hybrid OS due to be announced next week by Google, there are some interesting parallels. This past weekend Hiroshi Lockheimer, who owns Android and ChromeOS at Google, tweeted as follows:

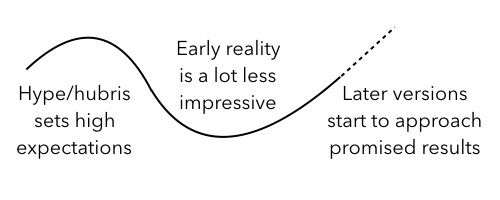

Why do I bring this up? Well, given Andromeda is also the name of the hybrid OS due to be announced next week by Google, there are some interesting parallels. This past weekend Hiroshi Lockheimer, who owns Android and ChromeOS at Google, tweeted as follows: My worry with Lockheimer’s remarks is that, in September 2008, Android wasn’t obviously going to be the hit it has since become. In hindsight, the launch of Android was enormously important, and helped create today’s smartphone market, but at the time the G1 launched it was a clunky and marginal bit of hardware. The concern is that whatever Google announces next week will be received – at least initially – in the same way. Perhaps some will see in it the promise of amazing things to come, but I suspect the initial impact will be marginal, and it will take years to see the true impact. And it’s entirely possible that the impact won’t be nearly as impressive as Google clearly thinks it will be. Although Lockheimer is saying that we’ll look back on October 4th as being a milestone event, he’s saying it ahead of time, and that’s where the hubris comes in. Interestingly, the mythological Andromeda’s personal trajectory fits rather nicely onto that curve above too – her mother’s hubris has her flying high, only to be brought low by Poseidon’s wrath and her parents’ intended sacrifice of her, though eventually she’s rescued by Perseus and things start looking up again. Google’s Andromeda might well go through the same curve too – overhyped up front by company executives, only to fail to meet expectations in its early versions, though perhaps redeemed as the vision plays out over time.

My worry with Lockheimer’s remarks is that, in September 2008, Android wasn’t obviously going to be the hit it has since become. In hindsight, the launch of Android was enormously important, and helped create today’s smartphone market, but at the time the G1 launched it was a clunky and marginal bit of hardware. The concern is that whatever Google announces next week will be received – at least initially – in the same way. Perhaps some will see in it the promise of amazing things to come, but I suspect the initial impact will be marginal, and it will take years to see the true impact. And it’s entirely possible that the impact won’t be nearly as impressive as Google clearly thinks it will be. Although Lockheimer is saying that we’ll look back on October 4th as being a milestone event, he’s saying it ahead of time, and that’s where the hubris comes in. Interestingly, the mythological Andromeda’s personal trajectory fits rather nicely onto that curve above too – her mother’s hubris has her flying high, only to be brought low by Poseidon’s wrath and her parents’ intended sacrifice of her, though eventually she’s rescued by Perseus and things start looking up again. Google’s Andromeda might well go through the same curve too – overhyped up front by company executives, only to fail to meet expectations in its early versions, though perhaps redeemed as the vision plays out over time.