Note: Following something of a hiatus in late 2015 after the birth of our fourth child, I’m hoping to get back to a more regular publishing schedule here as we kick off 2016. Here’s my first post for the new year, which will hopefully be the first of many. You can see all previous posts on Apple from this site listed here.

Apple today released its customary end of year / holiday period App Store numbers in a press release. By themselves, these numbers are impressive, but it’s important to put them in context to really understand their significance. Today, I’ll share a few charts and other related numbers to evaluate the new numbers and their real meaning.

A quick word on sources

It’s important to note briefly before we start that App Store numbers are one of many data points Apple reports selectively and indirectly. We get these occasional milestone announcements at year end and in keynotes, but between those we’re left to extrapolate and interpolate based on other sources, including Apple’s financial reporting, which has historically provided some direct and indirect guidance on App Store sales. So please bear in mind that while some of the numbers below are based on announcements like today’s, many of them are based on these estimates, extrapolations, and interpolations. I believe they’re accurate, but I want readers to understand they’re not direct from the source.

Today’s numbers

Today’s numbers, in brief, were as follows:

- “In the two weeks ending January 3, customers spent over $1.1 billion on apps and in-app purchases”

- “January 1, 2016 marked the biggest day in App Store history with customers spending over $144 million. It broke the previous single-day record set just a week earlier on Christmas Day.”

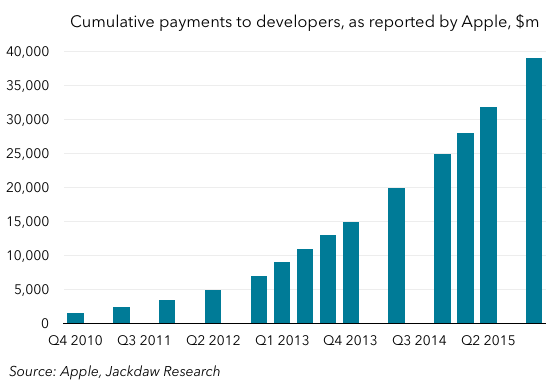

- Customers spent “over $20 billion” on the App Store in 2015

- The App Store has now paid out “nearly $40 billion” to developers since it launched in 2008, and over a third of that was paid out in the past year.

There were also some numbers about jobs and job creation, but those won’t be the focus of this post.

Putting the numbers in context

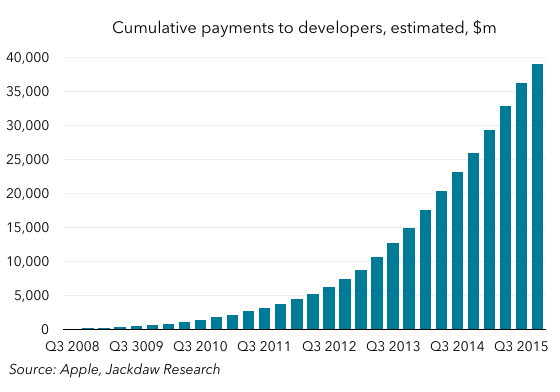

So let’s put those in context. Focusing just on the numbers Apple has reported directly, here’s the picture on the cumulative payments to developers, ending with today’s “nearly $40 billion” (which I’ve pegged at $39 billion): Using my estimates for the periods not directly reported, we get this smoother and less patchy version, which also goes back to the inception of the App Store in 2008:

Using my estimates for the periods not directly reported, we get this smoother and less patchy version, which also goes back to the inception of the App Store in 2008: As you can see, it’s a lovely curve, with what appears to be accelerating growth. In fact, we can look at that growth more easily by charting trailing four-quarter payments instead, as follows:

As you can see, it’s a lovely curve, with what appears to be accelerating growth. In fact, we can look at that growth more easily by charting trailing four-quarter payments instead, as follows: What you see here is that the growth has been fairly steady for the last few years, since about 2013, with the occasional bump here and there. Apple’s annual run-rate for payments to developers is now around $14 billion, which translates into the “over $20 billion” customer spend number in today’s press release. That’s an enormous revenue number for something which is effectively a feature in Apple’s platform.

What you see here is that the growth has been fairly steady for the last few years, since about 2013, with the occasional bump here and there. Apple’s annual run-rate for payments to developers is now around $14 billion, which translates into the “over $20 billion” customer spend number in today’s press release. That’s an enormous revenue number for something which is effectively a feature in Apple’s platform.

Longer-term patterns

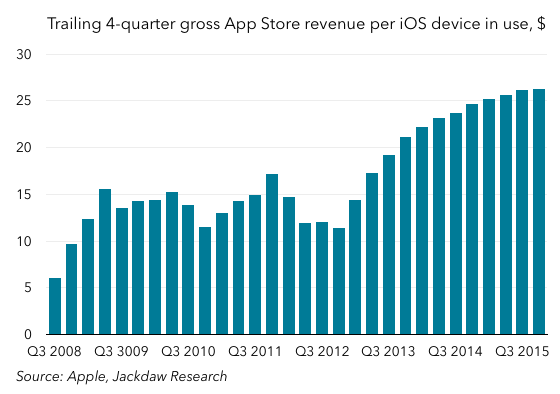

If you look again at that last chart, though, you’ll see that the early history is less consistent. There are some ups and downs in the early years, though they’re a little hard to make out in that chart because of the sheer scale of payments in the later years. One way to dive deeper into this and to look at the longer-term trends is to use another set of numbers – the base of iOS devices in use – to put these figures in context. Here, again, we have to make certain assumptions about the size of that base, but we have enough data points to be reasonably confident there too.

The chart below shows the average annual revenue per iOS device in use since the inception of the App Store: What you see in the chart is a series of different eras in the history of the App Store in which the trends were quite distinctive. In the early going, spend quickly leveled off at around $15 per year per iOS device, and it then began to falter a little. Apple introduced in-app purchases as a new feature in late 2009, and that seems to have sparked a slight renaissance in 2010, along with the launch of the iPad and some higher-priced apps which launched for that platform. However, by 2012, this number was back in decline, likely as the base of iOS devices diversified beyond early adopters and into new markets with lower spending power. In fact, that is the trend you’d expect to see over time, as existing users make do largely with apps they already own, and as new users in new geographies join the base.

What you see in the chart is a series of different eras in the history of the App Store in which the trends were quite distinctive. In the early going, spend quickly leveled off at around $15 per year per iOS device, and it then began to falter a little. Apple introduced in-app purchases as a new feature in late 2009, and that seems to have sparked a slight renaissance in 2010, along with the launch of the iPad and some higher-priced apps which launched for that platform. However, by 2012, this number was back in decline, likely as the base of iOS devices diversified beyond early adopters and into new markets with lower spending power. In fact, that is the trend you’d expect to see over time, as existing users make do largely with apps they already own, and as new users in new geographies join the base.

However, what you actually see is that, starting around late 2012, the number starts rising significantly, eventually leveling off again at around $25, significantly higher than in the early years of the App Store. What drove this growth? I mentioned already that in-app purchases launched in late 2009, but it wasn’t until late 2012 that Candy Crush Saga launched. Of course, one app didn’t change the trajectory of the whole App Store, but this app exemplifies a new business model that’s become increasing prevalent – even dominant – in the App Store, and in App Store revenues. Many others have followed a similar path to monetization since then, and I suspect it’s the rise of in-app purchases in games that’s driven that growth since late 2012. I’ve written about the rise of these games, and some of the unpleasant economics associated with them, elsewhere, but there’s no doubt they’ve had a significant impact on the App Store and its revenue composition.

There’s no doubt that games in general, and those featuring in-app purchases in particular, are a major driver for the App Store growth Apple trumpets on a regular basis. The two big questions that arise out of all of this are whether Apple wants to continue to rely so heavily on a model that has unsavory characteristics, and whether in focusing on this dominant category it’s neglecting other business models in the App Store. That latter topic is something we’ve discussed a couple of times recently on the Beyond Devices podcast, most notably in Episode 24.