Apple’s earnings for its fiscal second quarter (which I will refer to from here out as Q1 2016, as is my custom) were rocky. As Tim Cook said, it was a challenging quarter. There was bad news not just in iPhone, where Apple had already suggested there would be, but in other areas too. It’s worth enumerating exactly what those sources of bad news are to understand what’s going on at Apple. But there was also some good news in the earnings, which is particularly important when looking at the longer term. This post outlines both, starting with the bad news.

All three major product lines shrinking

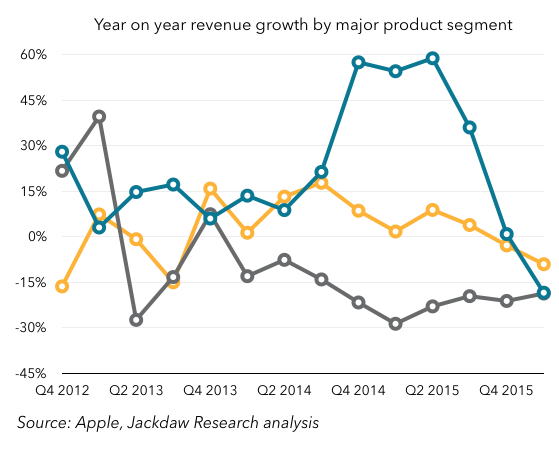

Yes, iPhone shipments and revenues dipped year on year for the first time, and that was a major cause of the overall problems. But what compounded it was that Apple’s other two major product lines were shrinking too in the quarter: The iPhone decline was new, but the trend line in Mac sales has been worsening consistently over the past year, and has now been below zero for the past two quarters. That’s significant, because for a time the Mac was offsetting shrinkage from the iPad, such that combined revenues from the two were rising or steady. Now that this aggregate number is also in the red, the declining iPhone sales just exacerbate the problem.

The iPhone decline was new, but the trend line in Mac sales has been worsening consistently over the past year, and has now been below zero for the past two quarters. That’s significant, because for a time the Mac was offsetting shrinkage from the iPad, such that combined revenues from the two were rising or steady. Now that this aggregate number is also in the red, the declining iPhone sales just exacerbate the problem.

iPhone ASPs falling

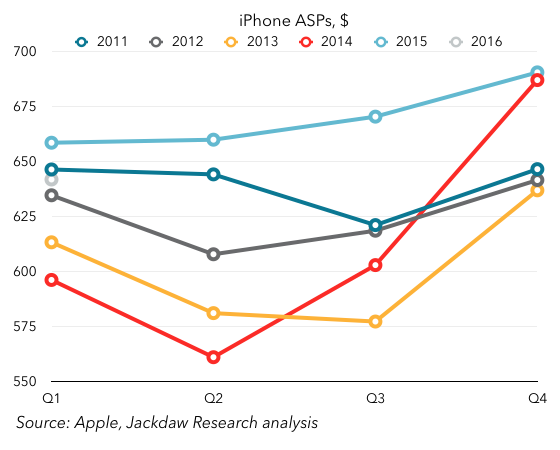

Besides the stellar growth in iPhone sales the iPhone 6 prompted, it (and the iPhone 6s) also helped drive significantly higher average selling prices. The chart below shows ASPs on a cyclical basis, so you can see the trend over the past several years and where Q1 2016 should have landed, and where it did land: As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.

As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.

Softness in China

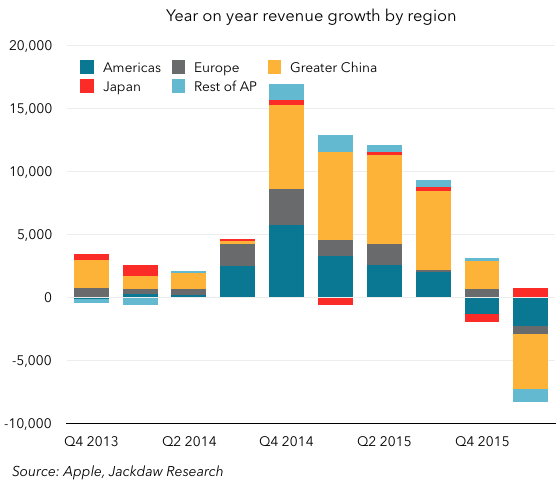

China has been a major driver of Apple’s growth over the past couple of years. The relationship with China Mobile, expansion of better cellular networks in China combined with expansion in Apple’s distribution, and then the launch of larger phones all contributed to outsized growth there. Over the last couple of quarters, though, things have changed dramatically: Whereas China accounted for half or more of the company’s revenue growth for several quarters, it’s now accounting for half its year on year shrinkage. One of Apple’s biggest drivers of growth has become a driver of decline. Again, the biggest culprit is iPhone sales and the massive iPhone 6 year, and the underlying decline in Mainland China is much less dramatic than reported results for the Greater China region, which includes Hong Kong. But for the time being, this is more bad news.

Whereas China accounted for half or more of the company’s revenue growth for several quarters, it’s now accounting for half its year on year shrinkage. One of Apple’s biggest drivers of growth has become a driver of decline. Again, the biggest culprit is iPhone sales and the massive iPhone 6 year, and the underlying decline in Mainland China is much less dramatic than reported results for the Greater China region, which includes Hong Kong. But for the time being, this is more bad news.

What you have overall, between the three major declining product lines, falling iPhone ASPs, and softness in Greater China, is a perfect storm of sorts that’s driving the current problems for Apple. What, then, is the good news in all this?

iPhone decline is temporary and cyclical

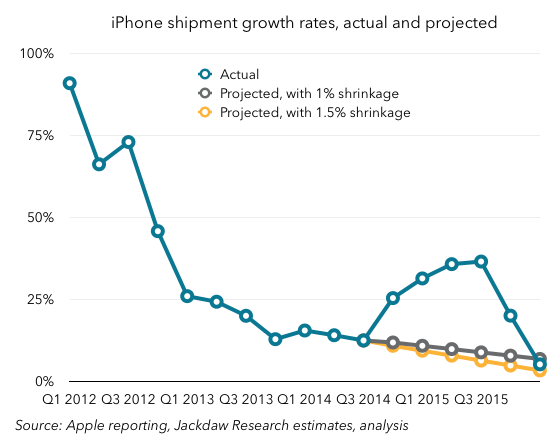

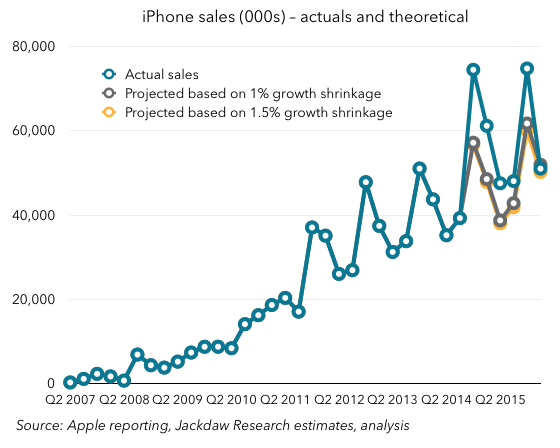

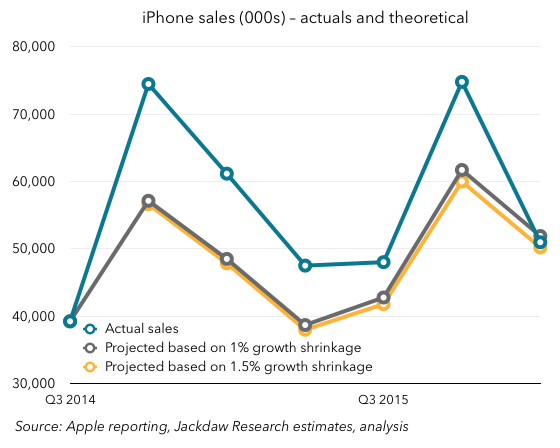

As I wrote earlier this week, the most important thing to understand about iPhone growth is that it’s temporary and cyclical. That is, the massive growth Apple experienced over the last 18 months or so was entirely down to the introduction of larger phones, and demand is now simply returning to its prior trajectory. The iPhone shipments number Apple reported was bang on with the projections I shared earlier this week and therefore also absolutely in line with the pre-iPhone 6 trend. That suggests (and Apple’s guidance for next quarter confirms) that iPhone growth should be back on track later this year, at high single digits or low double digits. The iPhone SE will depress margins, especially because it’s going to sell best during the annual trough in high-end sales, but for the same reasons, ASPs should recover by the end of the year when a new flagship phone launches. In the meantime, it should help fill that usual trough in sales a little, boosting sales above where they would otherwise be.

The other thing to bear in mind is that, though the iPhone 6 upgrade cycle was itself something of a one-off, all those who bought phones during that cycle will want to upgrade at some point. What was notable about this down quarter in iPhone sales was that Tim Cook said the last six months were the highest ever for Android switching. That implies that what fell short during that period was upgrades. That, in turn, suggests that when this base of iPhone 6 buyers finally does upgrade in large numbers – likely between 2-3 years from their purchase – we could see another big bump in sales, an aftershock of sorts. The biggest impact would hit in a roughly eighteen month period from this September through the following March, which provides more reason for optimism about longer term iPhone growth.

Signs of iPad recovery

It’s easy to focus on the decline in iPad sales, which has been problematic for Apple over the last several years, especially as the Mac has stopped growing. But the reality is that there are signs of recovery in iPad, albeit not growth just yet. But the rate of year on year decline has been slowing steadily, and on the earnings call Apple took the unusual step of signaling where it thinks they’ll come in next quarter, at least directionally. Here’s the trend line for the past couple of years: That rate of decline has improved for three of the last four quarters. Apple’s guidance for Q2 2016 was that this would be the best year on year compare in two years. That suggests a shrinkage of less than 14% (since Q3 2014 was the previous low within that period, at 14% – I’m assuming the 8% it achieved in Q2 2014 is out of the 2-year window). (Update: I’m told by Jason Snell that it was “over two years” and the transcript confirms that, so the 8% might well be within the window after all). That’s obviously not stellar, but it continues and even improves the trend over the past year or so of slowing declines. As this decline slows, that puts Apple in less of a hole that it has to dig out of.

That rate of decline has improved for three of the last four quarters. Apple’s guidance for Q2 2016 was that this would be the best year on year compare in two years. That suggests a shrinkage of less than 14% (since Q3 2014 was the previous low within that period, at 14% – I’m assuming the 8% it achieved in Q2 2014 is out of the 2-year window). (Update: I’m told by Jason Snell that it was “over two years” and the transcript confirms that, so the 8% might well be within the window after all). That’s obviously not stellar, but it continues and even improves the trend over the past year or so of slowing declines. As this decline slows, that puts Apple in less of a hole that it has to dig out of.

Reasons to believe the Mac will recover

There isn’t anything in the recent Mac results that provides reasons for optimism – as I said above, the results show a steadily worsening trend in the case of the Mac. However, I believe at least part of the reason for the decline is that as of the end of the quarter, Apple hadn’t updated most of its Mac lineup in a long time. The Macrumors Buyer’s Guide listed the whole lineup as “don’t buy” because of the length of time since the last upgrade. Obviously, the MacBook has since been updated, but the rest of the lineup hasn’t. As with iPhones, the evidence is that new customers aren’t the problem here – Cook made much of the high “new to Mac” numbers this quarter. The issue is once again upgrades, and there we should see better numbers later this year as Apple upgrades the product line with new Intel Skylake chips. The timing of that change is hard to predict, but it should help the Mac revenue growth line turn positive again, helping to offset the smaller iPad decline.

Other new products driving growth

The Apple Watch isn’t broken out in Apple’s results explicitly, but it has contributed meaningfully to the overall revenue line over the past twelve months. The Other Products line where it sits includes both the iPod and accessories, which had been declining fairly significantly, but that segment’s revenues have been growing year on year since the Apple Watch launch. In the first part of this year, that growth is likely to be modest, but once again come the fall things should look better as Apple updates the hardware and drives new sales.

Another interesting new product that’s driving growth is Apple Music, which now has 13 million paying customers. That’s good for a run-rate of a little over $1.5 billion on an annualized basis, and the growth rate (around 25-30k new subscribers per day) should see Apple get close to 20 million by the end of the year, which in turn would drive annualized revenue of $2.3 billion. Given that iTunes Music generated around $4 billion at its peak, and is now generating much less, this new service is on track to begin driving meaningful growth for Apple in the music category again. More broadly, Services continues to be one of the drivers of growth at Apple, driven not just by Apple Music but to a great extent by the App Store too. The good thing about that growth is that it is driven by the growing base rather than sales of new devices, so to the extent that Apple is still adding new iPhone customers, it should continue to grow even as iPhone shipments slow down for a period.

All signs point to a return to growth in the fall

All of this taken together points to another couple of tough quarters for Apple as the perfect storm of declines across its three major product areas, its second most important region, and iPhone ASPs hits home. But it also points to reasons for optimism come the fall, when the iPhone should start to rebound, Mac sales should be stronger, a new Watch should drive sales there, and iPad shrinkage will be lower. The narrative Apple needs to be spinning is less about Services, though those are an important component of future growth, and more about the fact that the current dip in revenues is temporary. There were some references to that in the earnings call yesterday – Tim Cook used the phrase “pause in our growth,” suggesting that he believes this. But of course Apple doesn’t provide guidance beyond a single quarter. That may need to change if it wants to get investors back on board.