Note: this blog is published by Jan Dawson, Founder and Chief Analyst at Jackdaw Research. Jackdaw Research provides research, analysis, and consulting on the consumer technology market, and works with some of the largest consumer technology companies in the world. We offer data sets on the US wireless and pay TV markets, analysis of major players in the industry, and custom consulting work ranging from hour-long phone calls to weeks-long projects. For more on Jackdaw Research and its services, please visit our website.

I recently spent a couple of days with AT&T as part of an industry analyst event the company holds each year. It’s usually a good mix of presentations and more interactive sessions which generally leave me with a pretty good sense of how the company is thinking about the world. Today, I’m going to share some thoughts about where the consumer parts of AT&T sit in late 2016, but I’m going to do so with the shadow of a possible Time Warner merger looming over all of this – something I’ll address at the end. From a consumer perspective the two major themes that emerged from the event for me were:

- AT&T now sees itself as an entertainment company

- AT&T is doubling down on the ampersand (&).

Let me explain what I mean by both of those.

AT&T as an entertainment company

The word “entertainment” showed up all over the place at the event, and it’s fair to say it’s becoming AT&T’s new consumer identity. From a reporting perspective, the part of AT&T which serves the home is now called the Entertainment Group, for example, and CEO Randall Stephenson said that was no coincidence – it’s the core of the value proposition in the home now. But this doesn’t just apply to the home side of the business – John Stankey, who runs the Entertainment Group, said at one point that “what people do on their mobile devices will be more and more attached to the emotional dynamics of entertainment” too.

That actually jibes pretty closely with something I wrote in my first post on this blog:

There are essentially five pieces to the consumer digital lifestyle, and they’re shown in the diagram below. Two of these are paramount – communications and content. These are the two elements that create emotional experiences for consumers, and around which all their purchases in this space are driven, whether consciously or unconsciously.

What’s fascinating about AT&T and other telecoms companies is that the two things that have defined them throughout most of their histories – connectivity and communications – are taking a back seat to content. People for the most part don’t have emotional connections with their connectivity or their devices – they have them with the other people and with the content their devices and connectivity enable them to engage with. AT&T seems to be betting that being in the position of providing content will create stickier and more meaningful relationships which will be less susceptible to substitution by those offering a better deal. And of course video is at the core of that entertainment experience.

The big question here, of course, is whether this is how consumers want to buy their entertainment – from the same company that provides their connectivity. AT&T is big on the idea that people should be able to consume the content of their choice on the device of their choice wherever they choose. On the face of it, that seems to work against the idea that one company will provide much of that experience, and I honestly think this is the single biggest challenge to AT&T’s vision of the future and of itself as an entertainment company. But this is where the ampersand comes in.

Doubling down on the ampersand

One of the other consistent themes throughout the analyst event was what AT&T describes as “the power of &”. AT&T has actually been running a campaign on the business side around this theme, but it showed up on the consumer side of the house too at the event. Incidentally, I recalled that I’d seen a similar campaign from AT&T before, and eventually dug up this slide from a 2004 presentation given by an earlier incarnation of AT&T.

But even beyond this ad campaign, AT&T is talking up the value of getting this and that, and on the consumer side this has its most concrete instantiation in what AT&T has done with DirecTV since the merger. This isn’t just about traditional bundling and the discounts that come with it, but about additional benefits you get when you bundle. The two main examples are the availability of unlimited data to those who bundle AT&T and DirecTV, and the zero-rating of data for DirecTV content on AT&T wireless networks. Yes, AT&T argues, you can watch DirecTV content on any device on any network, but when you watch it on the AT&T network it’s free. The specific slogan here was “All your channels on all your devices, data free when you have AT&T”.

The other aspect here is what I call content mobility. What I mean by that is being able to consume the content you have access to anywhere you want. That’s a given at this point for things like Netflix, but still a pretty patchy situation when it comes to pay TV, where rights often vary considerably between your set top box, home viewing on other devices, and out-of-home viewing. The first attempts to solve this problem involved boxes – VCRs and then DVRs for time shifting, and then the Slingbox for place shifting. But the long term solution will be rooted in service structure and business models, not boxes. For example, this content mobility has been a key feature of the negotiations AT&T has been undertaking both as a result of the DirecTV merger and in preparation for its forthcoming DirecTV Now service. It still uses a box – the DirecTV DVR – where necessary as a conduit for out-of-home viewing where it lacks the rights to do so from the cloud, but that’s likely temporary.

AT&T’s acquisition of DirecTV was an enabler of both of these things – offering zero rating as a benefit of a national wireless-TV bundle, and the negotiating leverage that comes from scale. It also, of course, gained access to significantly lower TV delivery costs relative to U-verse.

Now, the big question is whether consumers will find any of this compelling enough to make a big difference. I’m inherently skeptical of zero rating content as a differentiator for a wireless operator – even if you leave aside the net neutrality concerns some people have about it, it feels a bit thin. What actually becomes interesting, though, is how this allows DirecTV to compete against other video providers – in a scenario where every pay TV provider basically offers all the same channels, this kind of differentiation could be more meaningful on that side of the equation. If all the services offer basically the same content, but DirecTV’s service allows you to watch that content without incurring data charges on your mobile device, that could make a difference.

Context for AT&T&TW

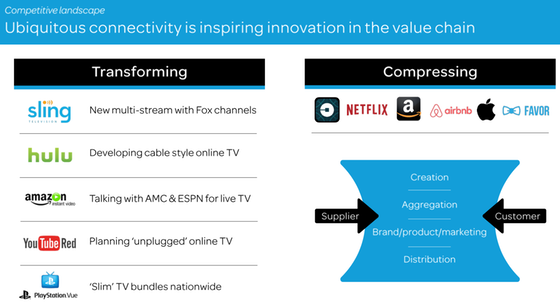

So let’s now look at all of this as context for a possible AT&T-Time Warner merger (which as I’m finishing this on Saturday afternoon is looking like a done deal that will be announced within hours). One of the slides used at the event is illustrative here – this is AT&T’s take on industry dynamics in the TV space:

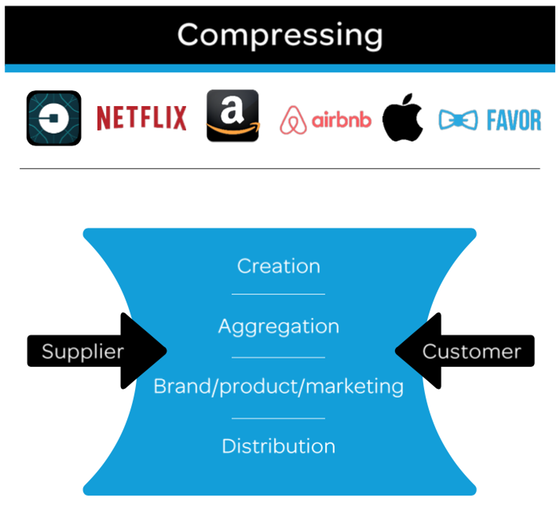

Now focus in on the right side of the slide, which talks about the TV value chain compressing:

The point of this illustration was to say that the TV value chain is compressing, with distributors and content owners each moving into each other’s territory. (Ignore the logos at the top, at least two of which seem oddly out of place). The discussion around this slide went as follows (I’m paraphrasing based on my notes):

In addition, AT&T executives at the event talked about the fact that the margins available on both the content and distribution side would begin to collapse for those only participating on one side as players increasingly play across both.

The rationale for a merger

I think a merger with Time Warner would be driven by three things:

- A desire to avoid being squeezed in the way just described as other players increasingly try to own a position in both content ownership and distribution – in other words, be one of those players, not one of their victims

- A furthering of the & strategy – by owning content, AT&T can offer unique access to at least some of that content through its owned channels, including DirecTV and on the AT&T networks. This is analogous to the existing DirecTV AT&T integration strategy described above

- Negotiating leverage with other content providers and service providers.

Both the second and third of these points would also support the content mobility strategy I described earlier, providing both leverage with content owners and potentially unique rights to owned content.

How would AT&T offer unique content? I don’t think it would shut off access to competitors, but I could see several possible alternatives:

- Preserving true content mobility for owned channels – only owned channels get all rights for viewing Time Warner content on any device anywhere. Everyone else gets secondary rights

- Exclusive windows for content – owned channels like DirecTV and potentially AT&T wireless would get early VOD or other access to content, for example immediate VOD viewing for shows which don’t show up for 24 hours, 7 days etc on other services

- Exclusive content – whole existing shows and TV channels wouldn’t go exclusive, but I could see exclusive clips and potentially new shows go exclusive to DirecTV and AT&T.

The big downside with all this is that whatever benefits AT&T offers to its own customers, by definition it would be denying those benefits to non-customers. That might be a selling point for DirecTV and AT&T services, but wouldn’t do much for Time Warner’s content. The trends here are inevitable, with true content mobility the obvious end goal for all content services – it’s really just a matter of time. To the extent that AT&T is seen to be standing in the way of that for non-customers, that could backfire in a big way.

On balance, I’m not a fan of the deal – I’ve outlined what I see as the potential rationale here, but I think the downsides far outweigh the upsides. Not least because the flaws in Time Warner’s earlier mega-merger apply here too – since you can never own all content, but just a small slice, your leverage is always limited. What people want is all the relevant content, not just what you’re incentivized to offer on special terms because of your ownership structure. I’ll wait and see how AT&T explains the deal to see if the official rationale makes any more sense, but I suspect it won’t change much.

{kind=link}

{kind=link}