Notes: this is part of a series on major tech companies’ Q4 2014 earnings. All past earnings posts can be seen here, and all earnings posts for Q4 2014 can be seen here. For the sake of easy comparisons and transparency, I always use calendar quarters in my analysis. Hence, Q4 2014 in this and every post on this blog means the quarter ending December 2014, even though some companies (Microsoft included) have fiscal years that end at other times of the year.

As usual, I’m going to run through a handful of charts and provide some analysis in this post. Subscribers to my quarterly company decks service will have received a slide deck with a much larger set of charts – this subscription is $10 per month for individual subscribers, and corporate subscriptions are also available.

The hardware business – some progress, some slippage

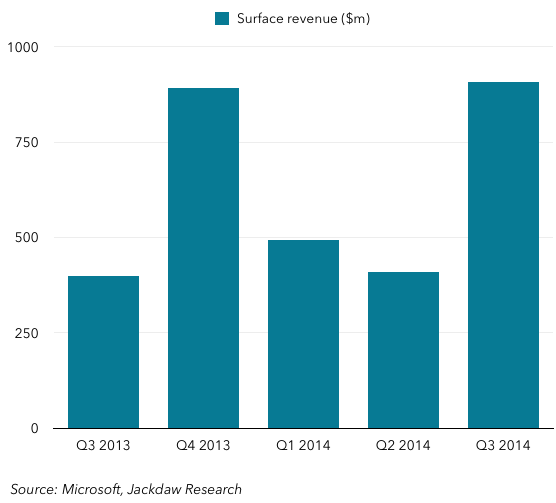

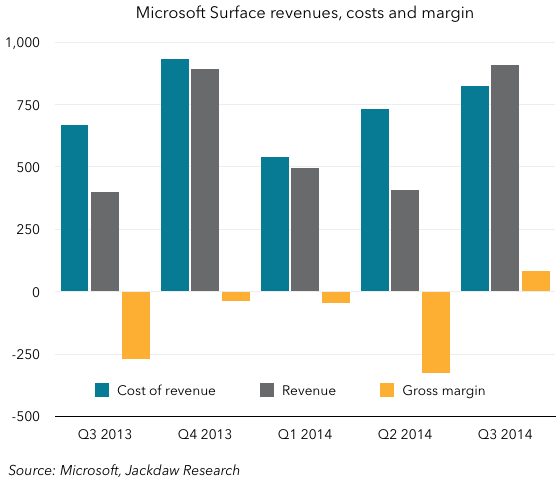

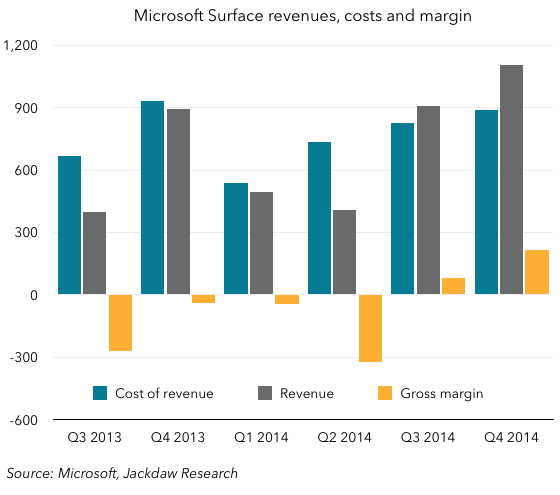

One of the themes last quarter was how the hardware business at Microsoft had progressed, and that’s a theme again this quarter. Surface revenues were the highest they’ve ever been in a quarter, crossing the $1 billion mark for the first time, and in addition the gross margins were not only positive for the second time, but significantly so if my calculations are correct:

I suspect that, on an operating basis, the Surface line still loses money because of all the marketing spend involved, but I would guess it’s not a million miles away from producing a positive contribution margin at this point, which is enormous progress from the early quarters. I suspect, with almost all the revenue this quarter coming from Surface Pro 3 sales, that ASPs were around $1,000, and that this represents around a million unit shipments, with some accessory spending rounding out the rest. Chances are that’s not much higher than previous quarters.

I suspect that, on an operating basis, the Surface line still loses money because of all the marketing spend involved, but I would guess it’s not a million miles away from producing a positive contribution margin at this point, which is enormous progress from the early quarters. I suspect, with almost all the revenue this quarter coming from Surface Pro 3 sales, that ASPs were around $1,000, and that this represents around a million unit shipments, with some accessory spending rounding out the rest. Chances are that’s not much higher than previous quarters.

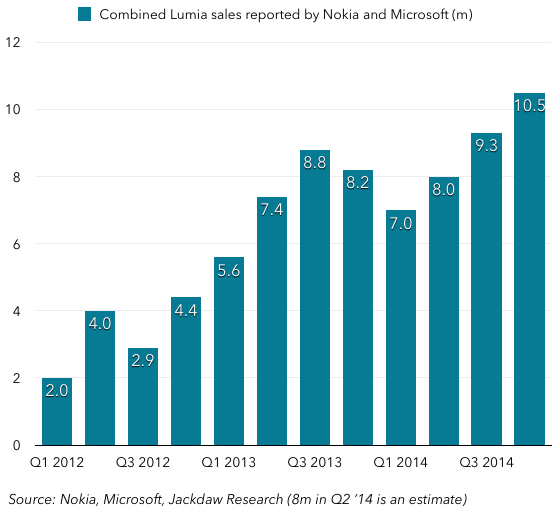

Lumia sales also hit a milestone this quarter, crossing 10 million for the first time:

Microsoft also reports non-Lumia phone sales, which dipped below 40 million for the first time in almost 10 years (including the former Nokia devices business). That business is now dropping fast. It’s hard to tell because Microsoft doesn’t provide ASPs for these two product lines, but based on my calculations, I suspect Lumia ASPs dropped from about $140 to closer to $120, reflecting the company’s focus on the low-end market. I continue to question the rationale for pursuing this end of the market, however. Microsoft’s thinking is that if it can capture these users, it can slowly migrate them up to more expensive devices along with Microsoft services, but I suspect that only a very small proportion of the users it’s capturing here will do so. They’re largely attracted by the low price and are also overwhelmingly in low-income demographics, making future revenue prospects poor.

Microsoft also reports non-Lumia phone sales, which dipped below 40 million for the first time in almost 10 years (including the former Nokia devices business). That business is now dropping fast. It’s hard to tell because Microsoft doesn’t provide ASPs for these two product lines, but based on my calculations, I suspect Lumia ASPs dropped from about $140 to closer to $120, reflecting the company’s focus on the low-end market. I continue to question the rationale for pursuing this end of the market, however. Microsoft’s thinking is that if it can capture these users, it can slowly migrate them up to more expensive devices along with Microsoft services, but I suspect that only a very small proportion of the users it’s capturing here will do so. They’re largely attracted by the low price and are also overwhelmingly in low-income demographics, making future revenue prospects poor.

Insight into Windows Phone financials

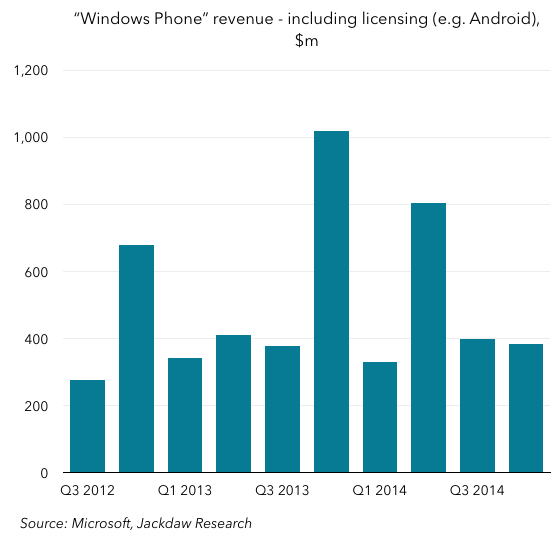

The “Windows Phone” reporting line has always been a fascinating one at Microsoft, and one I’ve dug into quite a bit in the past in search of nuggets of data. Two new nuggets came this time around, highlighting a couple of interesting points. Here’s my best estimate of the Windows Phone revenue line for the past two years or so, based on various statements in Microsoft’s SEC filings:

What’s interesting here is the extent to which this revenue dropped when Microsoft folded Nokia’s devices unit into the company. Q4 last year saw over $1 billion in revenue reported in this line, but this quarter it was under $400 million. The vast majority of that drop – around 60% – was said to be related to the Nokia acquisition. That, in turn, suggests that Android licensing revenue was less than half of total revenues in this reporting line, contrary to many people’s belief that Microsoft derived more revenue from Android licensing than Windows Phone licensing.

What’s interesting here is the extent to which this revenue dropped when Microsoft folded Nokia’s devices unit into the company. Q4 last year saw over $1 billion in revenue reported in this line, but this quarter it was under $400 million. The vast majority of that drop – around 60% – was said to be related to the Nokia acquisition. That, in turn, suggests that Android licensing revenue was less than half of total revenues in this reporting line, contrary to many people’s belief that Microsoft derived more revenue from Android licensing than Windows Phone licensing.

The other interesting tidbit was that Microsoft reported a fall in cost of revenue for the Devices & Consumer Licensing business related to the Nokia acquisition as follows:

D&C Licensing cost of revenue decreased, mainly due to a $224 million decline in traffic acquisition costs, primarily driven by prior year costs associated with our joint strategic initiatives with Nokia.

The only thing I can think of here is that this relates to some combination of Windows Phone and online advertising, since TAC is a metric usually associated with online advertising businesses, and D&C Licensing houses those Windows Phone revenues we just looked at. It seems as though Microsoft may have paid Nokia a fee for the traffic it sent to Bing and other Microsoft online properties, and this was somehow reported in D&C Licensing as a cost related to the Windows Phone revenues. The scale of that fee is pretty significant – $224 million in a single quarter, or almost $1 billion per year, which should improve the margins for the online advertising business significantly.

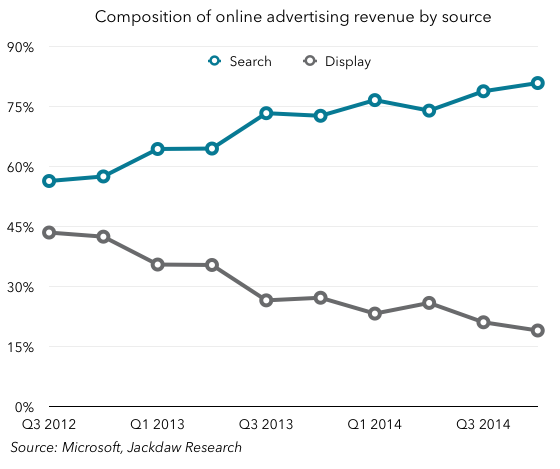

Online advertising continues to diverge

Speaking of online advertising, the trends there continue to diverge, as they do at other major online advertising companies, between search and display revenues. I’m presenting below the percentage of online advertising revenues that comes from each of these sources, according to my calculations:

As you can see, search advertising is now well over 75%, while display advertising is rapidly approaching 15%. I’ve talked before about these businesses, and my conviction that at this point Microsoft should simply pull out of the display advertising business, sacrificing a small amount of revenue but in the process bolstering its claim to be more sensitive to users’ data privacy concerns than Google, and this just reinforces the case. Bing is, at any rate, far more strategically important to Microsoft, especially given the integration with Cortana that’s critical to Windows Phone today and Windows 10 going forward.

As you can see, search advertising is now well over 75%, while display advertising is rapidly approaching 15%. I’ve talked before about these businesses, and my conviction that at this point Microsoft should simply pull out of the display advertising business, sacrificing a small amount of revenue but in the process bolstering its claim to be more sensitive to users’ data privacy concerns than Google, and this just reinforces the case. Bing is, at any rate, far more strategically important to Microsoft, especially given the integration with Cortana that’s critical to Windows Phone today and Windows 10 going forward.

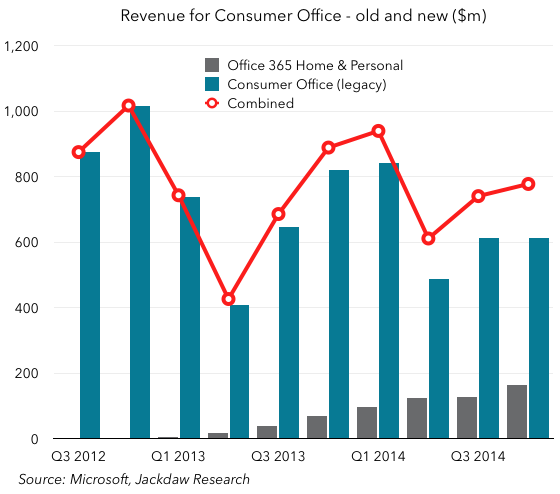

Office Consumer transition continues

Another data point I’ve picked up on in the past is the performance of Consumer Office, which comes in two parts: the legacy Office model, and Office 365 Home and Personal. The two continue to move in opposite directions, but with the overall impact of falling revenues from this business:

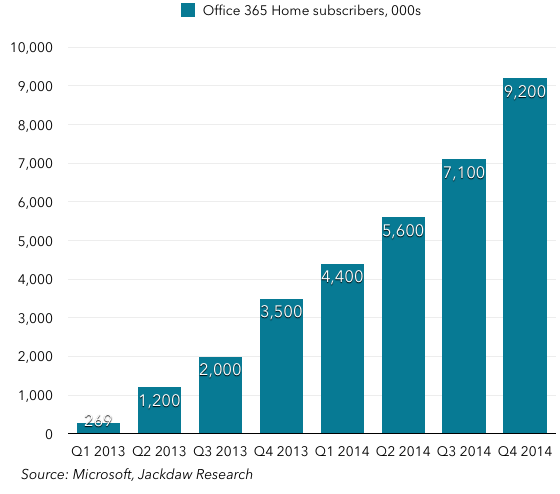

The red line shows total revenues from these two, which continues to fall year on year as Microsoft goes through this transition. As Microsoft gives away more and more of the core functionality of Office for free in the consumer market, however, this trend will accelerate. One bright point in this area, however, was the bump in Office 365 users this past quarter. I’m not yet sure what to attribute that too, but it’s likely that a combination of Office on the iPad and the new, slightly cheaper, Personal option (launched in Q3 but available for the whole of Q4) both had an impact:

The red line shows total revenues from these two, which continues to fall year on year as Microsoft goes through this transition. As Microsoft gives away more and more of the core functionality of Office for free in the consumer market, however, this trend will accelerate. One bright point in this area, however, was the bump in Office 365 users this past quarter. I’m not yet sure what to attribute that too, but it’s likely that a combination of Office on the iPad and the new, slightly cheaper, Personal option (launched in Q3 but available for the whole of Q4) both had an impact:

As the previous chart shows, the revenue stream associated with these subscribers is still small, but this is the future of Office in the Consumer market, so it’ll be well worth watching what happens to both the subscriber numbers and the revenue associated with them as Microsoft’s changing business model for Office kicks in (especially with the launch of Windows 10 later this year).

As the previous chart shows, the revenue stream associated with these subscribers is still small, but this is the future of Office in the Consumer market, so it’ll be well worth watching what happens to both the subscriber numbers and the revenue associated with them as Microsoft’s changing business model for Office kicks in (especially with the launch of Windows 10 later this year).

Lots more slides in the deck

Again, this is just a sampling of the data I collect and analyze on Microsoft on an ongoing basis. The deck that’s part of the subscription service has the full set, and is available now to subscribers. Sign up here if you’re interested (Paypal and credit card payment options available). A screenshot of the slides in the deck is below:

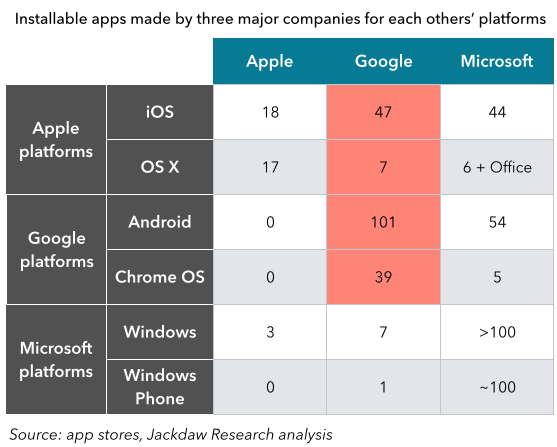

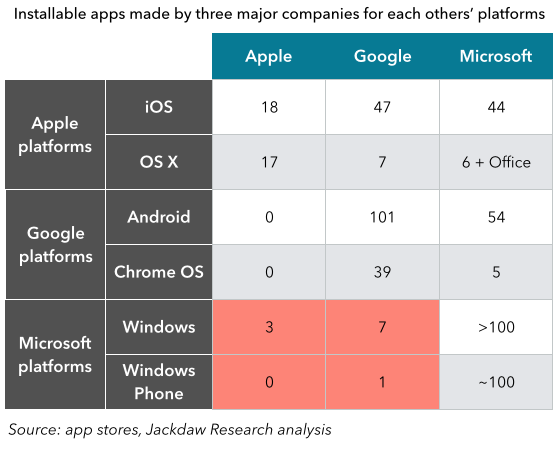

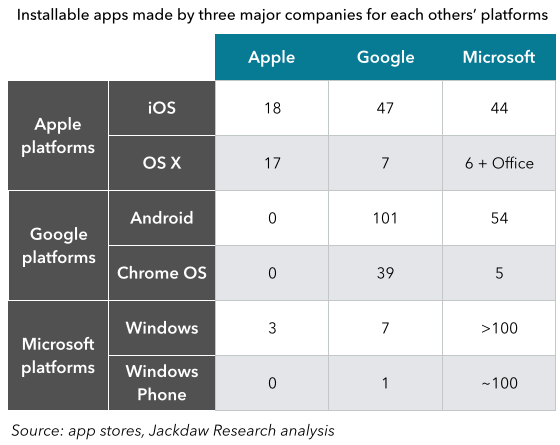

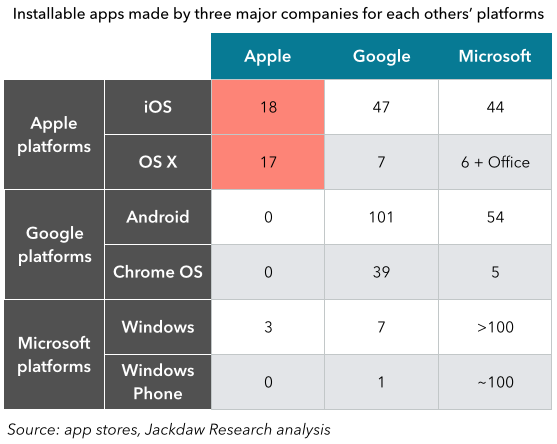

The key conclusion here is that Apple has focused very much on its own platforms, developing a little over a dozen apps for both iOS and OS X beyond those pre-installed on devices, but barely touching the other platforms at all. Where it does so, it’s exclusively to support major Apple services for iPhone and iPad users who also use Windows: iCloud Drive and iTunes are two of the three apps, while QuickTime – necessary for playing Apple-generated video files – is the third. Development of Safari on Windows – arguably a departure from Apple’s usual rules for a time – has been discontinued. It’s also worth noting that, even on its own platforms, Apple isn’t developing dozens of apps – there’s a small, focused number, which reflects another key Apple principle: keeping things simple, and focusing on what it does best.

The key conclusion here is that Apple has focused very much on its own platforms, developing a little over a dozen apps for both iOS and OS X beyond those pre-installed on devices, but barely touching the other platforms at all. Where it does so, it’s exclusively to support major Apple services for iPhone and iPad users who also use Windows: iCloud Drive and iTunes are two of the three apps, while QuickTime – necessary for playing Apple-generated video files – is the third. Development of Safari on Windows – arguably a departure from Apple’s usual rules for a time – has been discontinued. It’s also worth noting that, even on its own platforms, Apple isn’t developing dozens of apps – there’s a small, focused number, which reflects another key Apple principle: keeping things simple, and focusing on what it does best.