Facebook’s announcement of person-to-person payments through Facebook Messenger last week has a lot of people scratching their heads. The most puzzling part? It’s not charging for these payments, even though there’s a cost to Facebook, which means it’ll lose money on every transaction. So why would Facebook do this, and what implications does it have for payments and other services at Facebook?

Take a step back for a minute and look at Apple. For years, signing up for an iTunes account was almost impossible unless you were willing to provide credit card details for potential music purchases. As such, Apple collected credit card information for hundreds of millions of users, which enabled the later introduction of purchases of other forms of content such as TV shows, books and movies, and much later enabled the easy introduction of Apple Pay. Having a payment method on file makes creating new paid-for services much easier and more seamless, but getting the credit card information for the first time is the big hurdle. Just look at Google – it’s struggled for years to get users to pay for apps and content. There are certainly other reasons for this, but one of the key reasons is the fact that users don’t provide credit card information when they sign up for either a Google account or an Android device. In markets where Google has added carrier billing as a payment option, app purchases rise significantly, according to one of the companies I’ve spoken to which provides the underlying technology.

So, back to Facebook. Other than its fairly limited previous payments play with partners such as Zynga, Facebook has never really given users a reason to add payment information to their accounts. And that’s been fine, because Facebook’s main business model has been advertising, with payments and other fees dwindling as a source of revenue. But as Facebook attempts for a second time to create a platform for developers and businesses, payment information will be a critical element of many of the potential implementations. The biggest barrier? Most of Facebook’s users don’t have payment information on file. How, then, to incentivize these users to add their credit card details? I suspect fee-free person-to-person payments may well be the trojan horse Facebook is using to catalyze users into adding their payment details to their accounts. Give users a compelling reason to add their details, and then you’ve got them for other purposes too. Now all it requires is getting their permission to use the same credit card for other transactions.

So, what transactions could we be talking about here? Well, last year Facebook trialled some basic commerce solutions, such as a Buy button, and at last year’s F8 conference it announced Autofill with Facebook, in partnership with several other payment providers. But at today’s F8 event we got a much better sense of what it has planned. The Buy button together with Facebook’s Messenger platform announcement highlight various ways in which Facebook could benefit from having users’ credit card details on file. If that platform is to make money, in fact, it’s almost certain that it’ll need some way to allow users to make payments for various products and services, of which Facebook would naturally take a cut. But even beyond the platform announcement, Facebook is planning to bring more video and news content into Facebook natively, and having ways for users to pay for such content on a subscription basis would also be attractive, just as Apple allows its users to do today. In fact, almost all of the ways in which Facebook could diversify away from advertising require it to have ways for users to pay for things through Facebook, and that requires getting their payment details.

All of this brings us back to Google, which we touched on briefly earlier. Google clearly plans to get into the payments business itself with Android Pay over the coming months, and it would obviously love to increase users’ spend on apps and content as well over time. But Google has struggled throughout its history to get users to pay for things, especially since it’s taught them so effectively that its most useful services will be free, supported by advertising. What will Google’s vehicle be for getting users to add their payment details to their profiles? It could arguably take a leaf out of Facebook’s book here – find a way to incentivize users to add their credit cards to their accounts through a service that’s compelling in its own right. Once that’s done, all kinds of new opportunities will open up.

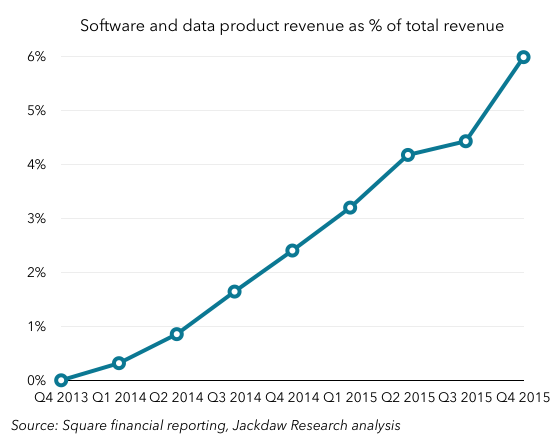

So, no matter how much Square grows this side of its business, its margins are capped according to standard payment industry rates. However, Square isn’t just sticking to this business, but instead seeks to build an ecosystem around it through software and data products, so far mostly Square Capital (loans to Square payments customers) and Caviar (restaurant services). That business is very highly profitable because it has few incremental costs, and has been growing rapidly:

So, no matter how much Square grows this side of its business, its margins are capped according to standard payment industry rates. However, Square isn’t just sticking to this business, but instead seeks to build an ecosystem around it through software and data products, so far mostly Square Capital (loans to Square payments customers) and Caviar (restaurant services). That business is very highly profitable because it has few incremental costs, and has been growing rapidly:

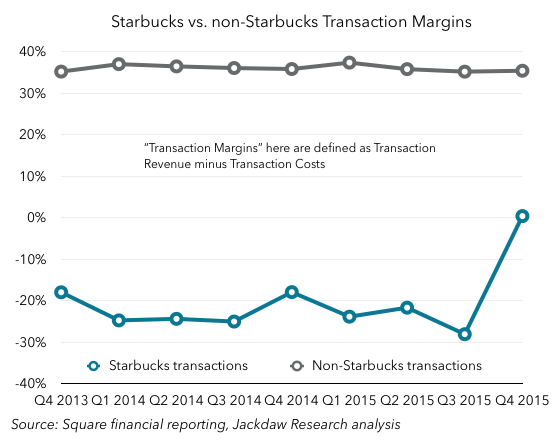

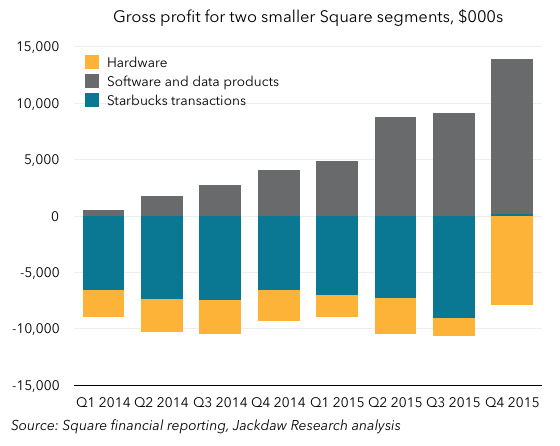

Another positive indicator this quarter was the fact that Square’s renegotiated contract with Starbucks, which was previously a heavy loss maker, broke even in Q4. This deal, which was originally done to drive scale for Square, has always been a drag on the business, but now promises to be much less of one:

Another positive indicator this quarter was the fact that Square’s renegotiated contract with Starbucks, which was previously a heavy loss maker, broke even in Q4. This deal, which was originally done to drive scale for Square, has always been a drag on the business, but now promises to be much less of one: That also now means that Square’s three smaller reporting segments are collectively profitable on a gross margin level too:

That also now means that Square’s three smaller reporting segments are collectively profitable on a gross margin level too: To be sure, Square is still loss making overall by every measure but gross margin, but projects to be Adjusted EBITDA positive in 2016 and to start generating margins sometime beyond that. This quarter’s results suggest it’s very much on track for that goal, although it’s still a long way off.

To be sure, Square is still loss making overall by every measure but gross margin, but projects to be Adjusted EBITDA positive in 2016 and to start generating margins sometime beyond that. This quarter’s results suggest it’s very much on track for that goal, although it’s still a long way off.

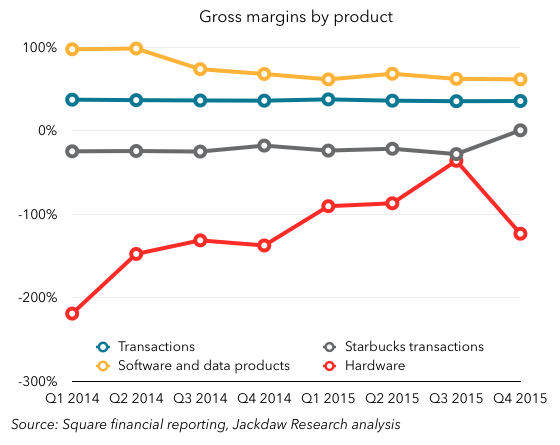

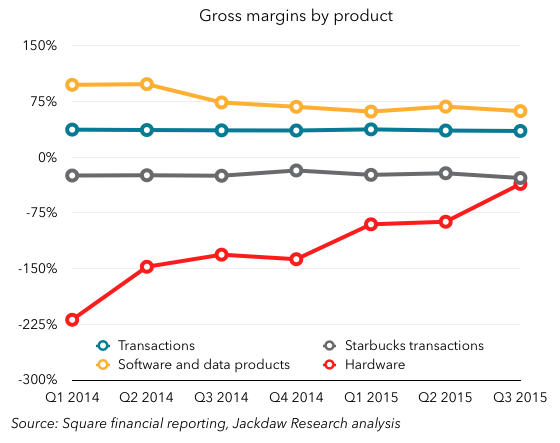

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.