Note: this blog is published by Jan Dawson, Founder and Chief Analyst at Jackdaw Research. Jackdaw Research provides research, analysis, and consulting on the consumer technology market, and works with some of the largest consumer technology companies in the world. We offer data sets on the US wireless and pay TV markets, analysis of major players in the industry, and custom consulting work ranging from hour-long phone calls to weeks-long projects. For more on Jackdaw Research and its services, please visit our website. If you want to contact me directly, you’ll find various ways to do so here.

Facebook and ad load have been in the news a bit the past few days, since CFO David Wehner said on Facebook’s earnings call that ad load would be a less significant driver of revenue growth going forward. I was listening to the call and watching the share price, and it was resolutely flat after hours until the moment he made those remarks, and then it dropped several percent. So it’s worth unpacking the statement and the actual impact ad load has as a driver of ad growth a bit.

A changing story on ad loads

First, let’s put the comments on ad load in perspective a bit. It’s worth looking at what’s been said about ad loads on earlier earnings calls to see how those comments compare. Here’s some commentary from the Q4 2015 call:

So, ad load is definitely up significantly from where we were a couple of years ago. And as I mentioned, it’s one of the factors driving an increasing inventory. Really one thing to kind of think about here is that improving the quality and the relevance of the ads has enabled us to show more of them and without harming the experience, and our focus really remains on the experience. So, we’ll continue to monitor engagement and sentiment very carefully. I mentioned that we expect the factors that drove the performance in 2015 to continue to drive the performance in 2016. So, I think that’s the color I can give on ad loads.

Here’s commentary from a quarter later, on the Q1 2016 call:

So on ad load, it’s definitely up from where we were couple of years ago. I think it’s really worth emphasizing that what has enabled us to do that is just improving the quality and the relevance of the ads that we have, and that’s enabled us to show more of them without harming the user experience at all. So that’s been really key. Over time, we would expect that ad load growth will be a less significant factor driving overall revenue growth, but we remain confident that we’ve got opportunities to continue to grow supply through the continued growth in people and engagement on Facebook as well as on our other apps such as Instagram.

Some of that is almost a carbon copy of the Q4 commentary, but note the second half of the paragraph, where Wehner goes from saying 2016 would be like 2015 to saying that over time ad load would be a less significant driver. This is something of a turning point. Now, here’s Q2’s commentary:

Additionally, we anticipate ad load on Facebook will continue to grow modestly over the next 12 months, and then will be a less significant factor driving revenue growth after mid-2017. Since ad load has been one of the important factors in our recent strong period of revenue growth, we expect the rate at which we are able to grow revenue will be impacted accordingly…

These remarks turn “over time” into the more specific “after mid-2017”. Now here’s the Q3 commentary that caused the stock drop:

I also wanted to provide some brief comments on 2017. First on revenue, as I mentioned last quarter, we continue to expect that ad load will play a less significant factor driving revenue growth after mid-2017. Over the past few years, we have averaged about 50% revenue growth in advertising. Ad load has been one of the three primary factors fueling that growth. With a much smaller contribution from this important factor going forward, we expect to see ad revenue growth rates come down meaningfully….

Again, it feels like there’s an evolution here, even though Wehner starts out by saying he’s repeating what he said last quarter. What’s different now is the replacement of “less significant factor driving revenue” with “much smaller contribution from this important factor”, and “the rate at which we are able to grow revenue will be impacted accordingly” to “ad revenue growth rates come down meaningfully“. Those changes are both a matter of degree, and they feel like they’re intended to suggest a stronger reduction in growth rates going forward.

Drivers of growth

However, as Wehner has consistently reminded analysts on earnings calls, ad load is only one of several drivers of growth for Facebook’s ad revenue. The formula for ad revenue at Facebook is essentially:

Users x time spent x ad load x price per ad

To the extent that there’s growth in any of those four components, that drives growth in ad revenue, and to the extent that there’s growth in several of them, there’s a multiplier effect for that growth. To understand the impact of slowing growth from ad load, it’s worth considering the contribution each of these elements makes to overall ad revenue growth at the moment:

- User growth – year on year growth in MAUs has been running in the mid teens, with a rate between 14 and 16% in the last year, while year on year growth in DAUs has been slightly higher, at around 16-17% fairly consistently

- Time spent – Facebook doesn’t regularly disclose actual time spent, but has said recently that this metric is also up by double digits, so at least 10% year on year and perhaps more

- Ad load – we have no metric or growth rate to look at here at all, except directionally: it rose significantly from 2013 to 2015, and continues to rise, but will largely cease to do so from mid-2017 onwards.

- Price per ad – Facebook has regularly provided directional data on this over the last few years, but it’s been a highly volatile metric unless recently, with growth spiking as mobile took off, and then settling into the single digits year on year in the last three quarters.

So, to summarize, using our formula above, we have growth rates as follows: 16-17% user growth plus 10%+ growth in time spent plus an unknown growth in ad load, plus 5-6% growth in price per ad.

The ad load effect

Facebook suggests that ad load is reaching saturation point, so just how loaded is Facebook with ads today? I did a quick check of my personal Facebook account on four platforms – desktop web, iOS and Android mobile apps, and mobile web on iOS. I also checked the ad load on my Instagram account. This is what I found:

- Desktop web: an ad roughly every 7 posts in the News Feed, plus two ads in the right side bar. The first ad was the first post on the page

- iOS app: an ad roughly every 12 posts, with the first ad being the second post in the News Feed

- iOS web: An ad roughly every 10 posts, with the first ad being the fourth post in the News Feed

- Android app: an add roughly every 10-12 posts, with the first ad being the second post in the News Feed

- Instagram on iOS: the fourth post and roughly every 10th post after that were ads.

That’s pretty saturated. You might argue that Facebook could raise the density of ads on mobile to match desktop density (every 7 rather than every 10-12), but of course on mobile the ad takes up the full width of the screen (and often much of the height too), which means the ceiling is likely lower on mobile. I’m sure Facebook has done a lot of testing of the tipping point at which additional ads deter usage, and I would imagine we’re getting close to that point now. So this is a real issue Facebook is going to be dealing with. I did wonder to what extent this is a US issue – in other words, whether ad loads might be lower elsewhere in the world due to lower demand. But on the Q2 earnings call, Facebook said that there aren’t meaningful differences in ad load by geography, so this is essentially a global issue.

So, then, if this ad load issue is real, what are the implications for Facebook’s ad revenue growth? Well, Facebook’s ad revenue has grown by 57-63% year on year over the past four quarters, and increasing ad load is clearly accounting for some of the growth, but much of it is accounted for by the other factors in our equation. Strip that ad load effect out and growth rates could drop quite a bit, by anywhere from 10-30 percentage points. Facebook could then be left with 30-50% year on year growth without a contribution from ad load. Even at the lower end of that range, that’s still great growth, while at the higher end it’s amazing growth. But either would be lower than it has been recently.

Of course, it’s also arguable that capping ad load would constrain supply of ad space, which could actually drive up prices if demand remains steady or grows (which Facebook is certainly forecasting). Facebook has dismissed suggestions in the past that it would artificially limit ad load to drive up prices, but this is a different question. Supply constraints could offset some of the slowing contribution from ad load itself, though how much is hard to say.

Ad revenue growth from outside the News Feed

Of course, Facebook isn’t limited to simply showing more ads in the Facebook News Feed. While overall impressions actually fell from Q4 2013 to Q3 2015 as usage shifted dramatically from desktop to mobile, where there are fewer ads, total ad impressions have been up by around 50% year on year in the last three quarters. Much of that growth has been driven by Instagram, which of course has ramped from zero to the significant ad load I just described over the course of the last three years. Multiplied by Instagram user growth (which isn’t included in Facebook’s MAU and DAU figures) and that’s a significant contribution to overall ad growth too. As I understand it, the ad load comments apply to Instagram too, but there will still be a significant contribution to overall ad revenue growth from user growth.

And then there are Facebook’s other properties which until today haven’t shown ads at all: Messenger and WhatsApp. As of today, Facebook Messenger is going to start showing some ads, and that will be another potential source of growth going forward. WhatsApp may well do something similar in future, too, although Zuckerberg will have to overcome Jan Koum’s well-known objections first.

Growth beyond ad revenue

And then we have growth from revenue sources other than ads. What’s been striking about Facebook over the last few years – even more than Google – is how dominated its revenues have been by advertising. The proportion has actually risen from a low of 82% of revenue in Q1 2012 all the way back up to 97.2% in Q3 2016. It turns out that the increasing contribution from other sources was essentially down to the FarmVille era, with Zynga and other game companies generating revenues through Facebook’s game platform. What’s even more remarkable here is that these payments are still the bulk of Facebook’s “Payments and other fees” revenues today, as per the 10-Q:

…fees related to Payments are generated almost exclusively from games. Our other fees revenue, which has not been significant in recent periods, consists primarily of revenue from the delivery of virtual reality platform devices and related platform sales, and our ad serving and measurement products.

As you can see in the second half of that paragraph, Facebook anticipates generates some revenue from Oculus sales going forward, though it hasn’t been material yet, and later in the 10-Q the company suggests this new revenue will only be enough to (maybe) offset the ongoing decline in payments revenue as usage continues to shift from desktop to mobile.

Of course, Facebook now has its Workplace product for businesses too, which doesn’t even merit a mention in this section of the SEC filing. Why not? Well, it would take 33 million active users to generate as much revenue from Workplace in a quarter as Facebook currently generates from Payments and other fees. It would take 12 million active users just to generate 1% of Facebook’s overall revenues today. And that’s because Facebook’s ad ARPU is almost $4 globally per quarter, and $15 in the US and Canada. Multiplied by 1.8 billion users, it’s easy to see why Workplace at $1-3 per month won’t make a meaningful contribution anytime soon.

Conclusion: a fairly rosy future nonetheless

In short, then, Facebook is likely going to have to make do with ad revenue for the vast majority of its future growth. That’s not such a bad thing, though – as we’ve already seen, the other drivers of ad revenue growth from user growth to price per ad to time spent by users are all still significant drivers of growth in the core Facebook product, and new revenue opportunities across Instagram, Messenger and possibly WhatsApp should contribute meaningfully as well. That’s not to say that growth might not be slower, and possibly quite a bit slower, than in the recent past. But at 30% plus, Facebook will still be growing faster than any other big consumer technology company.

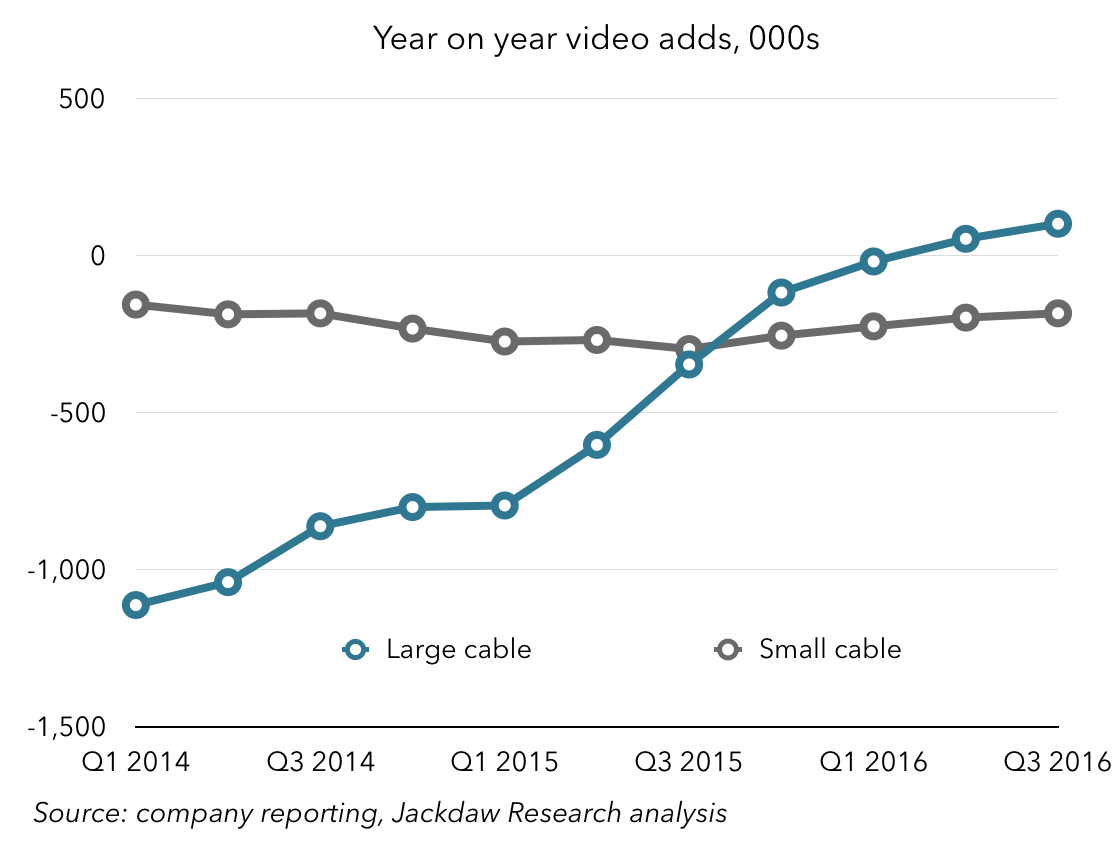

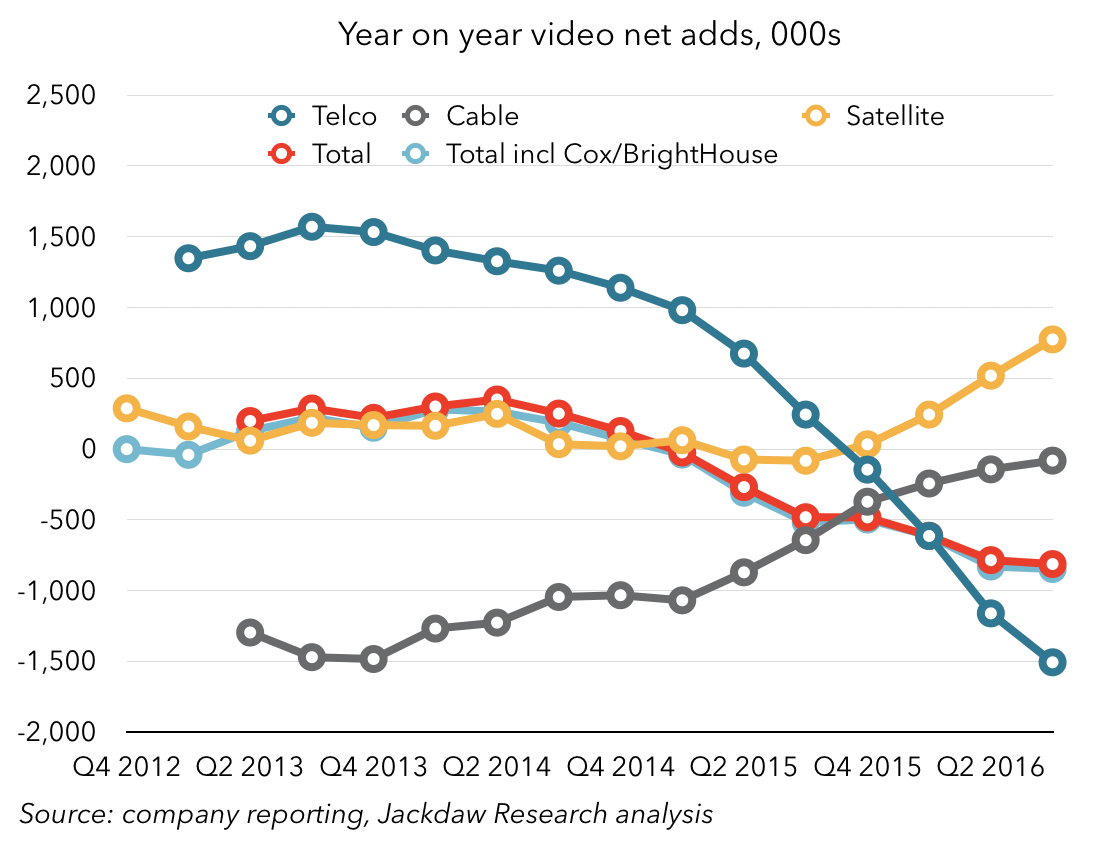

Cable, on the other hand, has been recovering somewhat, likely benefiting from the reduced focus by Verizon and AT&T on the space with their telco offerings. The cable operators I track collectively lost only 81k subscribers year on year, compared with well over a million subscribers annually throughout 2013 and 2014. Once again, that cable line masks differences between the larger and smaller operators, which saw distinct trends:

Cable, on the other hand, has been recovering somewhat, likely benefiting from the reduced focus by Verizon and AT&T on the space with their telco offerings. The cable operators I track collectively lost only 81k subscribers year on year, compared with well over a million subscribers annually throughout 2013 and 2014. Once again, that cable line masks differences between the larger and smaller operators, which saw distinct trends: