I’ve just sent my Twitter deck to subscribers (screenshot at the bottom of this post). This analysis picks a few of the key charts from that deck. As always, you may want to read my previous posts on Twitter, as a lot of the themes here are ones I’ve touched on before.

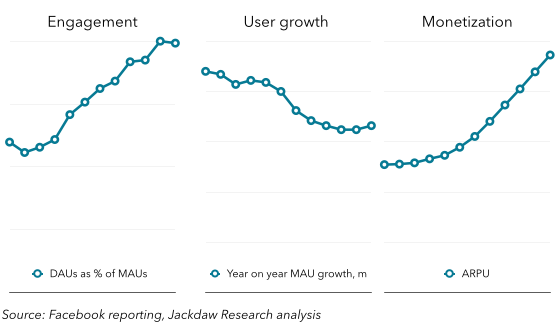

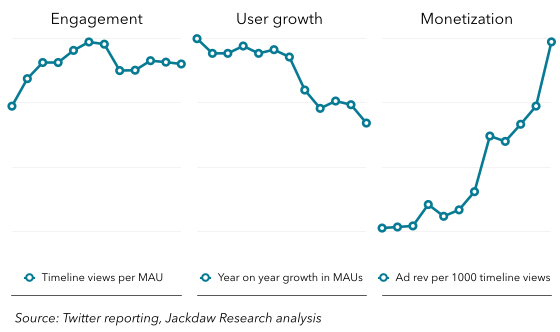

As I’ve talked about before in relation to both Twitter and Facebook, there are three main growth drivers for these companies: user growth, increased engagement, and better monetization of that engagement. Twitter’s problem continues to be that only one of these three is going in the right direction:

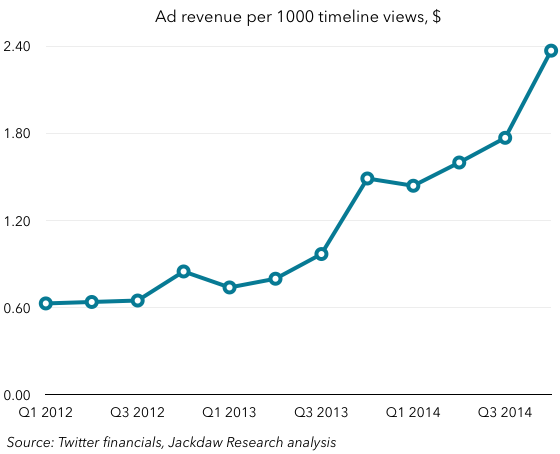

User growth has been slowing significantly over the past two years, and especially over the last few quarters. This quarter the company added just 4 million MAUs (or 8 if you’re charitable and give them back the 4 million additional MAUs they claim they lost to an iOS 8 bug). Even at 8 million, that’s by far the slowest growth in several years. Engagement, meanwhile, as measured by timeline views per MAU, has also been stagnant or falling for several quarters. The only metric moving in the right direction is monetization, and boy is it moving in the right direction! Here’s that chart broken out by itself, with the numbers:

User growth has been slowing significantly over the past two years, and especially over the last few quarters. This quarter the company added just 4 million MAUs (or 8 if you’re charitable and give them back the 4 million additional MAUs they claim they lost to an iOS 8 bug). Even at 8 million, that’s by far the slowest growth in several years. Engagement, meanwhile, as measured by timeline views per MAU, has also been stagnant or falling for several quarters. The only metric moving in the right direction is monetization, and boy is it moving in the right direction! Here’s that chart broken out by itself, with the numbers:

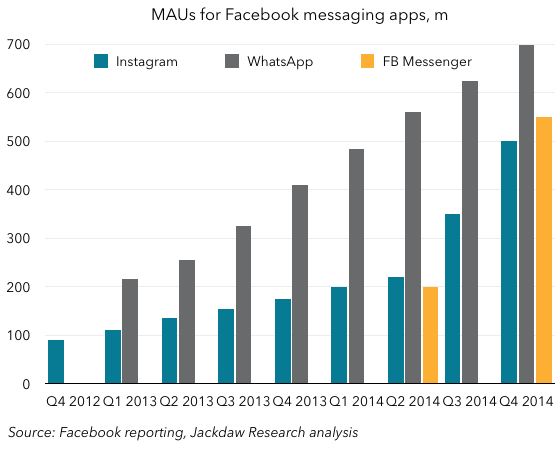

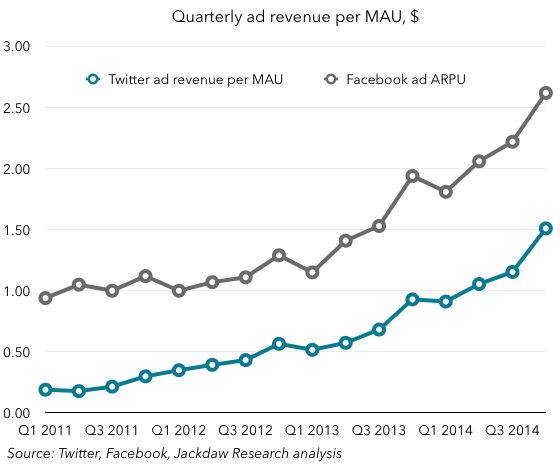

As you can see, the number has risen from 60 cents to almost $2.40 in the last three years, and it’s rising rapidly. In the US, this number is now almost $6 on a quarterly basis. The challenge with this number, though is that it’s unique to Twitter and therefore not comparable to anyone else’s metrics. However, since we know total ad revenue and we also know the number of MAUs, we can do a rough calculation for ad revenue per MAU for Twitter, and then compare it with the equivalent figure for Facebook:

As you can see, the number has risen from 60 cents to almost $2.40 in the last three years, and it’s rising rapidly. In the US, this number is now almost $6 on a quarterly basis. The challenge with this number, though is that it’s unique to Twitter and therefore not comparable to anyone else’s metrics. However, since we know total ad revenue and we also know the number of MAUs, we can do a rough calculation for ad revenue per MAU for Twitter, and then compare it with the equivalent figure for Facebook: What you can see is that the two lines are following a very similar trajectory, with Facebook quite a bit ahead of Twitter. I think what investors were so heartened about today was that Twitter demonstrated this ability to grow revenues significantly without growing users much at all, which suggests there’s still significant headroom on this ARPU measure. That means that, even if the other two growth drivers are underperforming, Twitter can still get good growth through the one lever that’s performing well. If it can get MAU growth going again as it promised to on today’s call, that will simply have a multiplier effect on that ARPU number, which will be so much the better.

What you can see is that the two lines are following a very similar trajectory, with Facebook quite a bit ahead of Twitter. I think what investors were so heartened about today was that Twitter demonstrated this ability to grow revenues significantly without growing users much at all, which suggests there’s still significant headroom on this ARPU measure. That means that, even if the other two growth drivers are underperforming, Twitter can still get good growth through the one lever that’s performing well. If it can get MAU growth going again as it promised to on today’s call, that will simply have a multiplier effect on that ARPU number, which will be so much the better.

The problem is, of course, that there is a ceiling here at some point – we just don’t know how high it is yet. Google generates between $30 and $50 per user annually in ad revenue from its own properties, so that could be a ceiling. But that’s based largely on one very effective form of advertising: search. There’s no guarantee that Twitter will ever be able to achieve that level of spend. Which brings us back to the question of the logged-out user. What was heartening both on today’s earnings call and in the last couple of weeks of news is that Twitter is finally really making some progress in telling the story of how it will grow this number. Though it refused to spell out the details of the Google agreement, it’s clear that Twitter hopes to drive significantly more traffic to Twitter.com in this way, for example. And then there’s the logged-out homepage it demoed this past week.

Despite all this, my two big questions for Twitter remain the same:

- How will it monetize all this activity from logged-out users? It’s said very little about this, even on today’s call, and all this usage has to be monetized for it ultimately to do Twitter any good.

- What are the new metrics by which we should measure Twitter’s progress on its new goals? It hasn’t established a consistent metric for measuring logged-out user activity (the 500m visitor number mentioned on today’s call was unchanged from three months ago). It’s abandoning its timeline views metric for engagement but won’t give us a different one. And ad revenue per 1000 timeline views only measures monetization of logged-in users, so how should we measure progress on monetizing the logged-out user? Twitter continues to try to steer everyone away from the metrics it does provide, but won’t supply metrics that support the new story it’s trying to tell.

Here’s a screenshot of the Twitter deck that went to subscribers earlier this evening: