For some reason, Samsung, LG, and Sony all ended up releasing their earnings this morning Asian time. As such, I spent some time earlier today updating all my models and charts, and tweeted out a few of them. There’s a full Samsung deck as part of the Jackdaw Research Quarterly Decks Service, which subscribers have already received, but I thought I’d do a quick roundup of key charts and the trends they represent as they relate to their respective smartphone businesses especially.

Samsung – recovery back on track

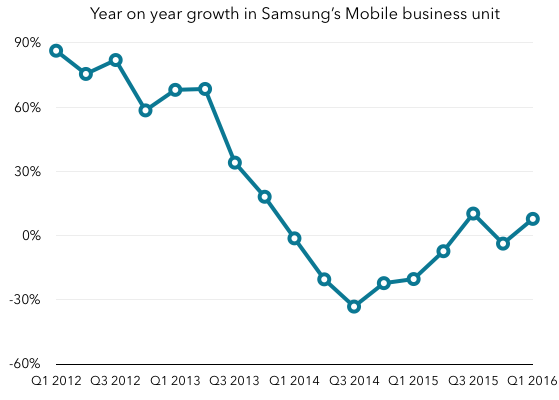

At Samsung, the mobile recovery appeared to falter a little last quarter, but is back on track this quarter, in large part thanks to the Galaxy S7 launch. Here are three key charts for Samsung.

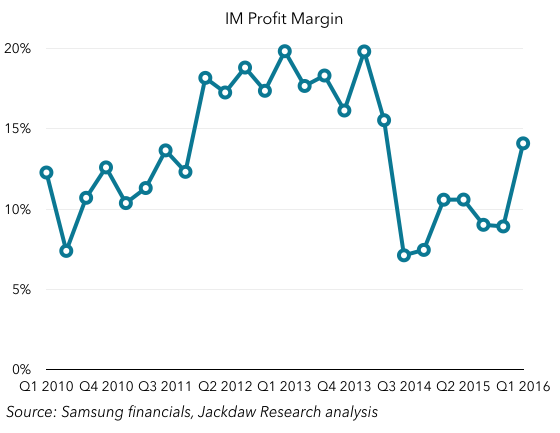

First off, year on year growth in the mobile business unit, which turned positive again after briefly dipping below zero last quarter: When it comes to margins, the IT and Mobile business unit did considerably better this quarter as well, with the best margins in almost two years:

When it comes to margins, the IT and Mobile business unit did considerably better this quarter as well, with the best margins in almost two years: And thanks to a combination of that increase at the IM unit as well as slightly weaker operating margins in semiconductors, IM became the biggest contributor to profits again for the first time in two years:

And thanks to a combination of that increase at the IM unit as well as slightly weaker operating margins in semiconductors, IM became the biggest contributor to profits again for the first time in two years: To what should we attribute all this? These were the bullet points from Samsung’s management for the quarter as relates to mobile:

To what should we attribute all this? These were the bullet points from Samsung’s management for the quarter as relates to mobile:

Earnings increased QoQ led by improved product mix with S7, and improved profitability of mid to low-end through streamlined line-up

Strong sales of S7 due to enhanced practical features as well as early introduction

Global sales expansion of 2016 A/J series.

The Galaxy S7 was both introduced earlier than the S6 last year, bringing the boost to revenues and margins forward, but it seems so far to be selling better, as it fixed some of the missteps with last year’s model. A pretty decent quarter for Samsung in smartphones overall, albeit still not close to its past glory days.

LG – Challenges Typical to Android Vendors

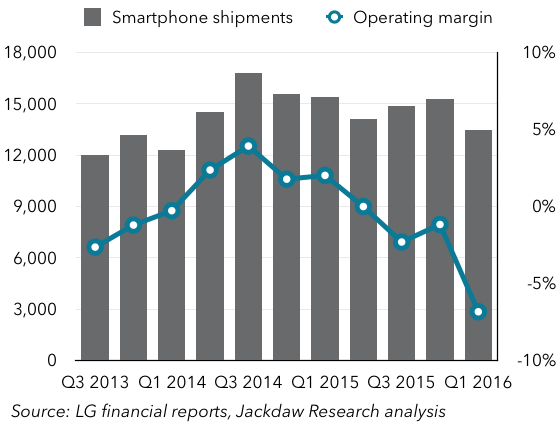

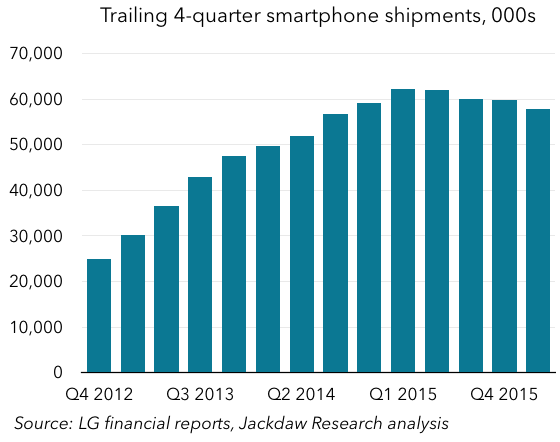

LG looked for a period in 2013 and 2014 as if it was finally figuring out smartphones – shipments were up, margins were briefly positive, and reviews of its flagship devices were too. But then things started to fall apart, and the trend since then hasn’t been so good: It’s harder to tell what’s going on there with the smartphone shipments line than the margin line, but over time it’s trending consistently downwards, as you can see in this trailing 4-quarter smartphone shipment chart:

It’s harder to tell what’s going on there with the smartphone shipments line than the margin line, but over time it’s trending consistently downwards, as you can see in this trailing 4-quarter smartphone shipment chart: LG appears to be suffering from much the same malaise as the other mid-tier Android smartphone vendors:

LG appears to be suffering from much the same malaise as the other mid-tier Android smartphone vendors:

- Increasingly strong competition at the high end from Apple and from Samsung’s resurgence as the dominant premium Android vendor

- Significant pressure from Chinese vendors producing increasingly good Android smartphones for far less

- A hollowing out of the mid-market by the introduction installment plans and the availability of both older flagship devices and budget premium devices from others.

There’s no real end in sight here – LG is failing to turn itself around as Samsung has, and the threat from Chinese vendors is only getting stronger. It needs a new strategy to fix things.

Sony: Fewer, More Expensive, Phones

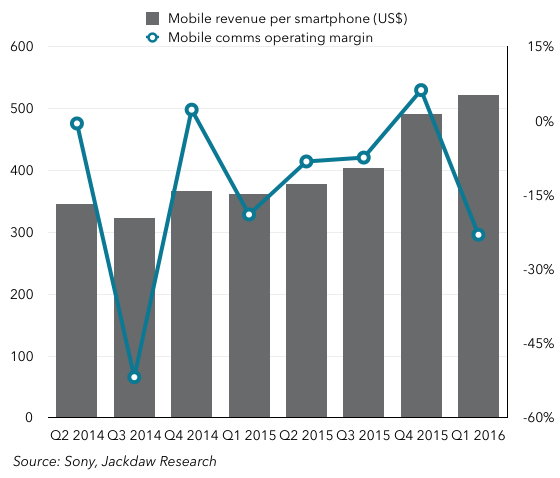

Speaking of new strategies, Sony’s was evident in its reporting this quarter. Its strategy is now to focus on the premium market only, which will see it sell far fewer phones at a far higher ASP. The chart below shows what’s happened to shipments lately, with both a quarterly and annualized perspective: As you can see, the strategy to sell fewer phones is clearly working – sales dropped off a cliff from Q4 to Q1, and the company hasn’t sold so few phones in many years. What about the other side of the strategy? Well, that seems to be working too – revenue per device sold is up:

As you can see, the strategy to sell fewer phones is clearly working – sales dropped off a cliff from Q4 to Q1, and the company hasn’t sold so few phones in many years. What about the other side of the strategy? Well, that seems to be working too – revenue per device sold is up: The problem, though, as you can also see from that chart, is that the higher ASPs aren’t – yet – leading to higher margins. In fact, margins fell this quarter, and that means an even bigger loss per device, given what happened to shipment numbers. It’s likely that the problem here is that it’s very hard to scale down the operation that produces smartphones as quickly as the number of smartphones sold scales down. Certainly, cost of sales should come down fairly rapidly, but all the other general costs of running a smartphone business aren’t as easy to cut, at least not quickly. It remains to be seen whether that other side of the strategy can fall in line too. If not, Sony will have just cut its business in half without seeing any of the margin benefits it should see from focusing on premium devices. It’s also not clear whether anyone can make money selling just 3 million smartphones a quarter.

The problem, though, as you can also see from that chart, is that the higher ASPs aren’t – yet – leading to higher margins. In fact, margins fell this quarter, and that means an even bigger loss per device, given what happened to shipment numbers. It’s likely that the problem here is that it’s very hard to scale down the operation that produces smartphones as quickly as the number of smartphones sold scales down. Certainly, cost of sales should come down fairly rapidly, but all the other general costs of running a smartphone business aren’t as easy to cut, at least not quickly. It remains to be seen whether that other side of the strategy can fall in line too. If not, Sony will have just cut its business in half without seeing any of the margin benefits it should see from focusing on premium devices. It’s also not clear whether anyone can make money selling just 3 million smartphones a quarter.