Note: for previous posts on BlackBerry, click here. I’ve specifically addressed some of the same topics in this earlier post.

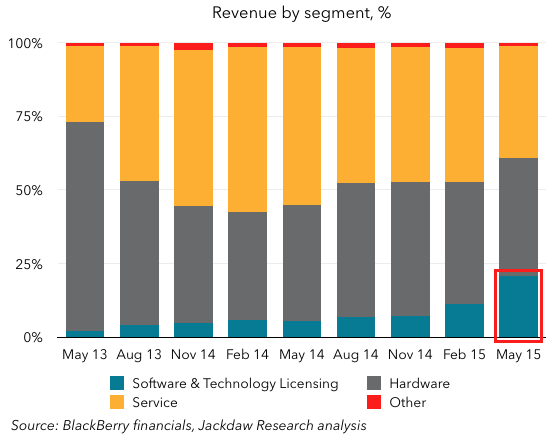

A little over a year ago, BlackBerry CEO John Chen said his goal was to double software revenue at the company from $250 million to $500 million in the company’s 2016 fiscal year, which ended in February. Today, the company reported results for that period, and even though the company moved the goalposts on that goal, it still missed its target. That’s important, because this software line is basically the future of the company, as hardware sales continue to tank, along with service access fees, the other historical mainstay of the company’s business.

Just to recap, the company first set its target for doubling software revenue back in late 2014, and at that point the goal was very much to double classic enterprise software revenue. In a meeting I attended with BlackBerry’s senior management in November 2014, we were told that each of BlackBerry’s roughly 250 sales reps was carrying a quota of $2 million for the year, which of course would add to $500 million if they all hit their quotas. So it was very clear that this target was for the enterprise software business BlackBerry then had.

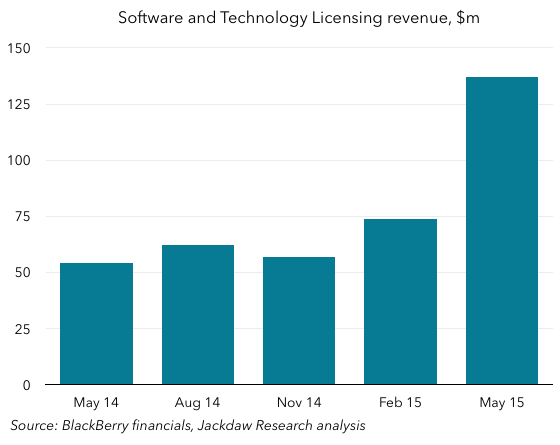

However, a few months later, BlackBerry announced its first patent license sales, outside the scope of those enterprise software quotas, but nonetheless reported in a new Software and Technology Licensing segment by BlackBerry in its financial results from that point onward (the name has since changed to Software & Services). Ever since then, BlackBerry has referred to this combined number and not the pure enterprise software number in measuring progress on hitting that $500 million goal in FY2016. Hence my comments about shifting the goal posts. In addition, the company has made several acquisitions, including a major one in the form of Good Technology, which have also contributed to the revenues reported in that segment.

Even with all that, the company just reported GAAP Software and Services revenue for the quarter of $494 million, $6 million shy of the $500 million target. In its press release, the only financial document available to analysts before today’s call, it listed only non-GAAP revenue for this segment, which brought the annual total to a little over $500 million and allowed the company to congratulate itself on meeting the goal. (The difference between the two is a fairly small amount of deferred revenue.)

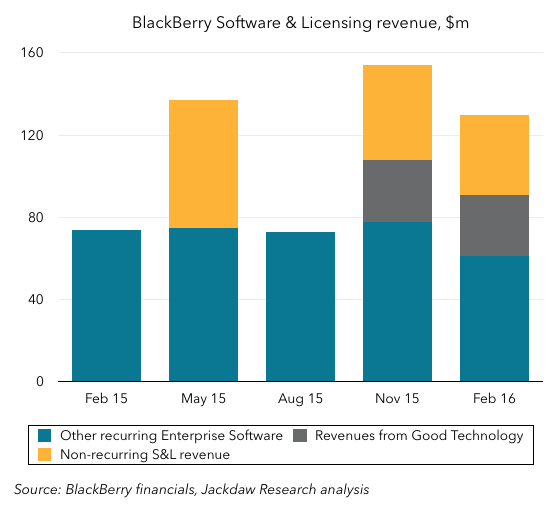

However, if we break down the revenues actually generated over the last five quarters in this segment into the part that represents the business that was originally supposed to hit that $500 million, and separate out the contribution from Good Technology and from patent and other licensing deals, we get a very different picture: As you can see, the portion of revenue that comes from recurring sources has remained roughly flat over that entire period, far from doubling. The company touted 106% growth in Software and Services revenue in Q4 and 113% for the entire fiscal year, but as the chart shows that growth was entirely made up by a combination of non-recurring revenue and revenue from the Good business, while the underlying business grew very little.

As you can see, the portion of revenue that comes from recurring sources has remained roughly flat over that entire period, far from doubling. The company touted 106% growth in Software and Services revenue in Q4 and 113% for the entire fiscal year, but as the chart shows that growth was entirely made up by a combination of non-recurring revenue and revenue from the Good business, while the underlying business grew very little.

The good news here, if there is some, is that for three of the last four quarters, BlackBerry has been able to generate very meaningful non-recurring revenue from licensing and other sales on top of enterprise software sales, which suggests that even if this business isn’t as predictable as recurring revenue, it’s still coming in fairly regularly. But only 70% of the segment’s revenues were recurring in the quarter, which makes future software revenues much less predictable. BlackBerry’s goal in FY2017 is much more modest than the doubling in revenue it aimed for in FY2016: it only wants to offset the decline in Service Access Fees, likely to be around $120-150 million in the year, but says nothing about offsetting the decline in Hardware, which declined by $90 million in FY2016 and is likely to continue to do so in FY2017.