Square (finally) reported its Q4 2015 results today, and they demonstrate solid progress on the key things that matter. For a very quick primer on the keys to Square’s long-term success, see the video embedded below. For more detailed earlier analysis, see this piece and this piece.

Here’s an update on some key areas where Square is making progress. As a reminder, the core transaction processing business has pretty much fixed margins – Square takes a roughly 3% cut of transaction value, and keeps around a third of that (or 1%) as gross profit:

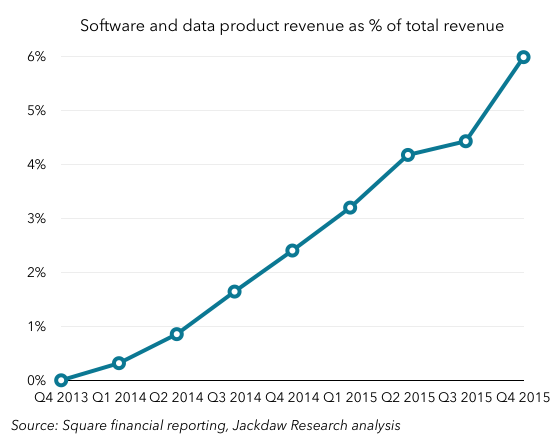

So, no matter how much Square grows this side of its business, its margins are capped according to standard payment industry rates. However, Square isn’t just sticking to this business, but instead seeks to build an ecosystem around it through software and data products, so far mostly Square Capital (loans to Square payments customers) and Caviar (restaurant services). That business is very highly profitable because it has few incremental costs, and has been growing rapidly:

So, no matter how much Square grows this side of its business, its margins are capped according to standard payment industry rates. However, Square isn’t just sticking to this business, but instead seeks to build an ecosystem around it through software and data products, so far mostly Square Capital (loans to Square payments customers) and Caviar (restaurant services). That business is very highly profitable because it has few incremental costs, and has been growing rapidly:

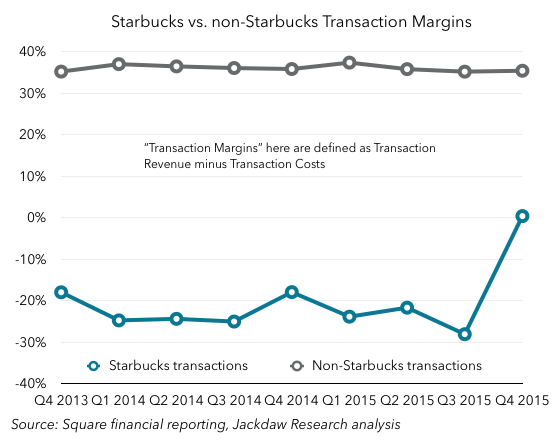

Another positive indicator this quarter was the fact that Square’s renegotiated contract with Starbucks, which was previously a heavy loss maker, broke even in Q4. This deal, which was originally done to drive scale for Square, has always been a drag on the business, but now promises to be much less of one:

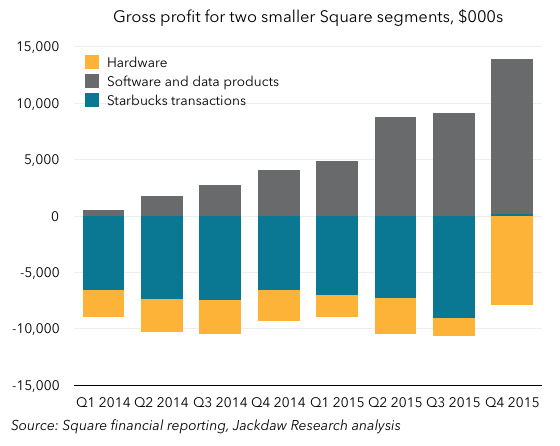

Another positive indicator this quarter was the fact that Square’s renegotiated contract with Starbucks, which was previously a heavy loss maker, broke even in Q4. This deal, which was originally done to drive scale for Square, has always been a drag on the business, but now promises to be much less of one: That also now means that Square’s three smaller reporting segments are collectively profitable on a gross margin level too:

That also now means that Square’s three smaller reporting segments are collectively profitable on a gross margin level too: To be sure, Square is still loss making overall by every measure but gross margin, but projects to be Adjusted EBITDA positive in 2016 and to start generating margins sometime beyond that. This quarter’s results suggest it’s very much on track for that goal, although it’s still a long way off.

To be sure, Square is still loss making overall by every measure but gross margin, but projects to be Adjusted EBITDA positive in 2016 and to start generating margins sometime beyond that. This quarter’s results suggest it’s very much on track for that goal, although it’s still a long way off.

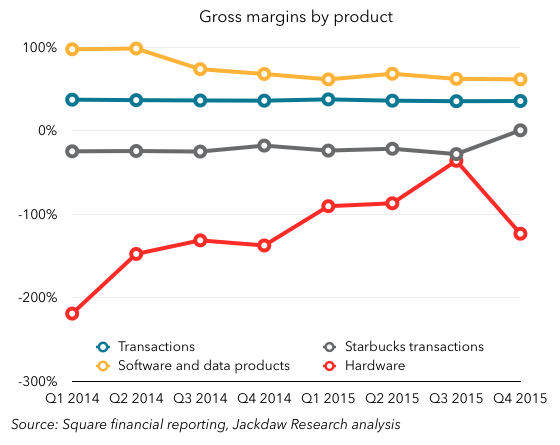

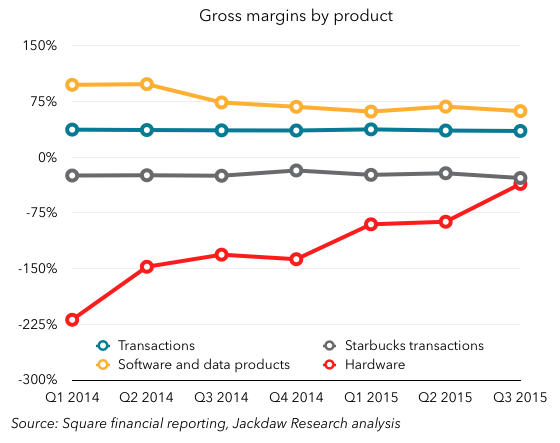

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.