Last quarter, I provided an overview of trends among the major US wireless providers in Q1 2014, and I’m repeating that analysis here for Q2 2014. A short preview including some analysis has been available on FierceWireless for the past week. I’m now providing additional analysis (below) and a detailed set of slides on Slideshare (also embedded below). Last quarter’s analysis is here, and a recent post on Sprint and T-Mobile, which provides further analysis is here.

This analysis covers five providers: AT&T, Sprint, T-Mobile, Tracfone and Verizon Wireless. Four of these are the largest carriers in the US market, and Tracfone is the fifth-largest provider, though not a carrier but an MVNO. There are other MVNOs in the US market, but none of them comes close to Tracfone in scale, and that’s why it’s included in this analysis. It’s also the largest prepaid provider in the US by some margin. These five providers between them make up the vast majority of the US market, especially since the acquisitions of Leap Wireless and MetroPCS in the last couple of years by AT&T and T-Mobile.

A tale of two markets

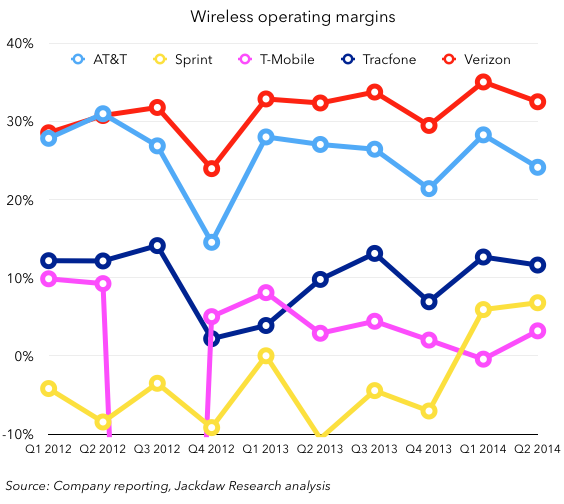

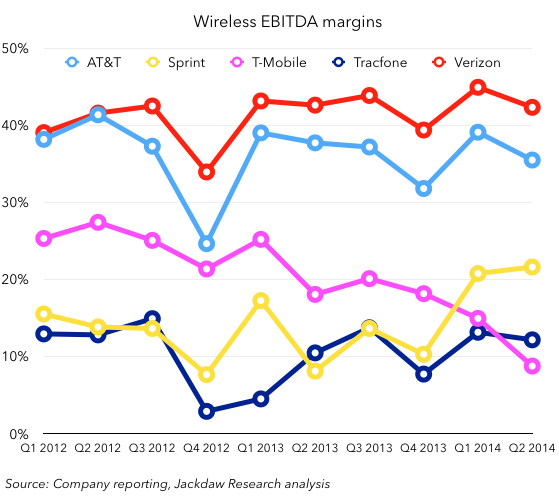

In many ways, the US wireless market is in fact still two separate markets, with AT&T and Verizon in one half, and the other players operating in the other. This is evident in total subscribers and revenues, margins, churn rates and other metrics, with AT&T and Verizon either larger or performing significantly better than the rest of the players. Here, for example, is a chart showing total subscribers for the five players: And here is a chart showing EBITDA margins:

And here is a chart showing EBITDA margins:

These carriers’ relative scale and profitability are related, as I’ve discussed previously, and most recently in last week’s post on Sprint and T-Mobile. This is perhaps the most important fact to understand about the US market, and one that isn’t likely to change anytime soon, as the gulf between the two largest players is far too great for any of the smaller players to bridge in the near future, at least organically. Continue reading

These carriers’ relative scale and profitability are related, as I’ve discussed previously, and most recently in last week’s post on Sprint and T-Mobile. This is perhaps the most important fact to understand about the US market, and one that isn’t likely to change anytime soon, as the gulf between the two largest players is far too great for any of the smaller players to bridge in the near future, at least organically. Continue reading