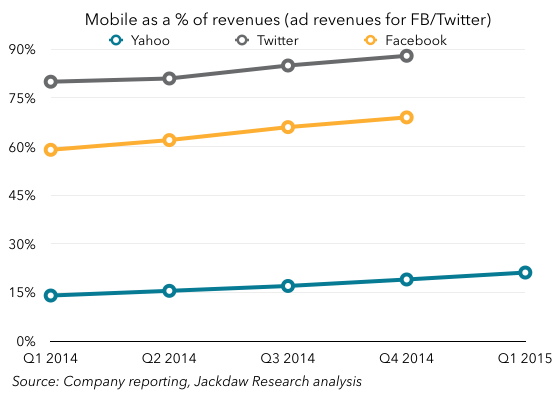

We’ll have to wait for the transcript to be sure, but Marissa Mayer must have described Yahoo as a mobile-first business a dozen times or so on the earnings call this afternoon. However, as Yahoo has also been quantifying its mobile business lately, we have some hard numbers to evaluate this claim by, and they’re not all that good at backing up her repeated claim.

First, here’s mobile as a share of revenues for Yahoo, as compared with Facebook and Twitter. Yahoo’s number is expressed as a percentage of what it calls “traffic-driven revenue”, while Facebook and Twitter’s are as a percentage of ad revenue, which likely means much the same thing:

Yahoo’s percentage is clearly growing somewhat, but not very fast, and it’s clearly light years behind Facebook, which began life as very much a desktop business, or Twitter, which has arguably always had a mobile-centric approach, especially to advertising. Those are mobile-first businesses: it’s hard to argue on this basis that Yahoo is.

Yahoo’s percentage is clearly growing somewhat, but not very fast, and it’s clearly light years behind Facebook, which began life as very much a desktop business, or Twitter, which has arguably always had a mobile-centric approach, especially to advertising. Those are mobile-first businesses: it’s hard to argue on this basis that Yahoo is.

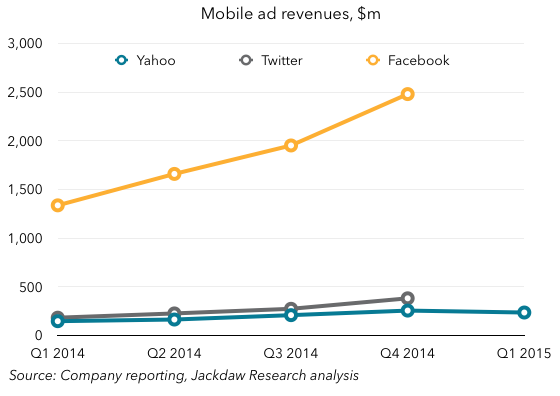

Another way to look at things is revenue:

Here, fledgling Twitter, which had just $20 million in revenue in Q1 2011, has already passed Yahoo and seems to be lengthening its lead. Facebook, meanwhile, is in a whole different league, and also growing much more rapidly. Again, Yahoo is clearly no mobile powerhouse just yet, and at these growth rates it’s just going to get left further and further behind.

Here, fledgling Twitter, which had just $20 million in revenue in Q1 2011, has already passed Yahoo and seems to be lengthening its lead. Facebook, meanwhile, is in a whole different league, and also growing much more rapidly. Again, Yahoo is clearly no mobile powerhouse just yet, and at these growth rates it’s just going to get left further and further behind.

If Yahoo is taking a mobile-first approach to product development, that’s clearly a good thing, and it certainly seems to be the case. But a company that has over 80% of its business tied to the legacy desktop world has a long way to go before it can call itself a mobile-first company.