The next company in my series of “thoughts on earnings” pieces (see Google here, Apple here and Facebook here) is Microsoft. I’ll be doing something on Amazon next, most likely. Microsoft is a complicated business, with many parts to it, so I’ll focus mostly on the things I think most people overlook, because they’re rather buried in the earnings release or even the 10-Q. This involves making some estimates, calculations and assumptions, as well as interpolation, so please understand that many of the numbers are my best guesses rather than those reported by Microsoft (I try to be clear on which is which in each case).

Long story short: for all Microsoft’s talk about Mobile and Cloud, those two categories likely generate under 10% of Microsoft’s revenue today – something I’ll return to in the conclusion at the end of this post.

Windows Phone

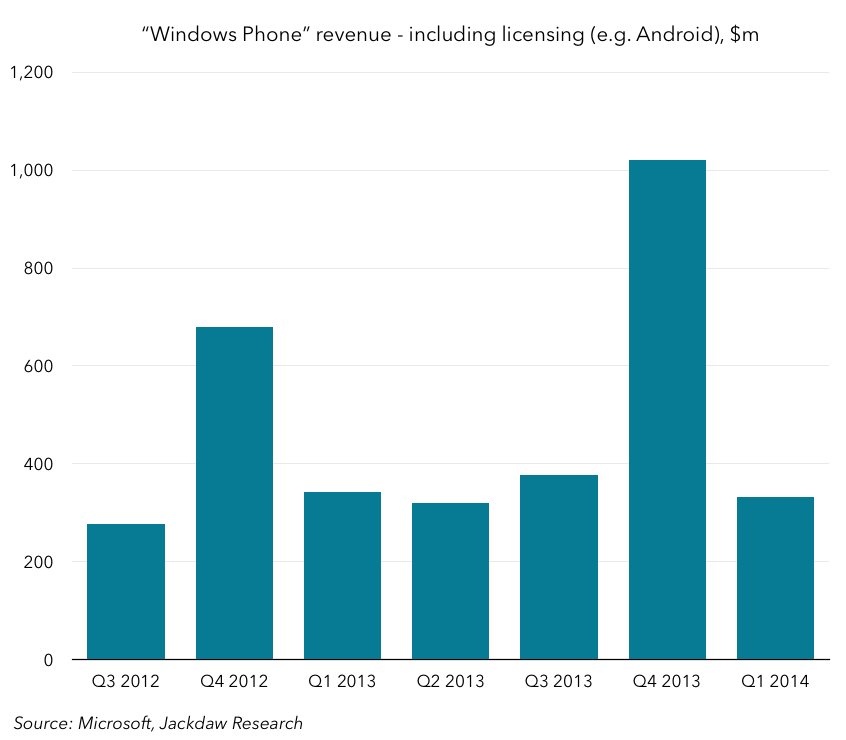

First, Windows Phone. I’ve written at length before about the methodology used here, but we got another couple of quarters’ worth of solid data so I’m providing some quick numbers off the back of that.

The key thing to note here is that, other than in the fourth quarter, this number stays a little under $400 million a quarter. And it’s worth reminding everyone that this number is not just Windows Phone licensing itself but also the rest of Microsoft’s mobile licensing activity (think patents licensed to Android OEMs). As such, as Microsoft executes on its new policy of not charging OEMs for Windows for devices under 9 inches, there’s only a very small amount of revenue at risk – likely $100-200 million per quarter. And of course Nokia was paying about 90% of that anyway, so it would have become an internal transfer starting today. Continue reading →

The key thing to note here is that, other than in the fourth quarter, this number stays a little under $400 million a quarter. And it’s worth reminding everyone that this number is not just Windows Phone licensing itself but also the rest of Microsoft’s mobile licensing activity (think patents licensed to Android OEMs). As such, as Microsoft executes on its new policy of not charging OEMs for Windows for devices under 9 inches, there’s only a very small amount of revenue at risk – likely $100-200 million per quarter. And of course Nokia was paying about 90% of that anyway, so it would have become an internal transfer starting today. Continue reading →