Yesterday, I covered Twitter’s earnings, and today I’m following up with a post on Facebook’s earnings. The two companies are very different – one is a social network that’s first and foremost about connecting with people you know in real life, and the other is a communication platform that’s more about catching up with the news and public figures. The former now has just shy of 1.5 billion monthly users, while the latter seems to be stuck at around 300 million. I’m not going to focus on the direct comparisons here, but you’ll note some stark contrasts as I review some key numbers from Facebook’s results.

The importance of Asia

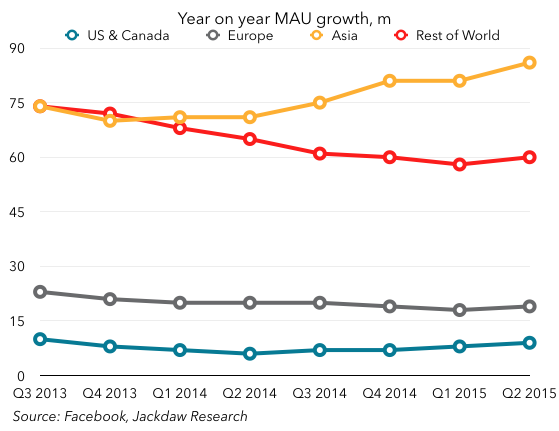

One of the most striking things to me from Facebook’s earnings is the importance of Asia. Firstly, user growth in Asia over the past year has been accelerating:

Other regions picked up a bit this quarter too, including the US & Canada (which is hard to see at this scale on the chart), but the Asian story is far more consistent.

Other regions picked up a bit this quarter too, including the US & Canada (which is hard to see at this scale on the chart), but the Asian story is far more consistent.

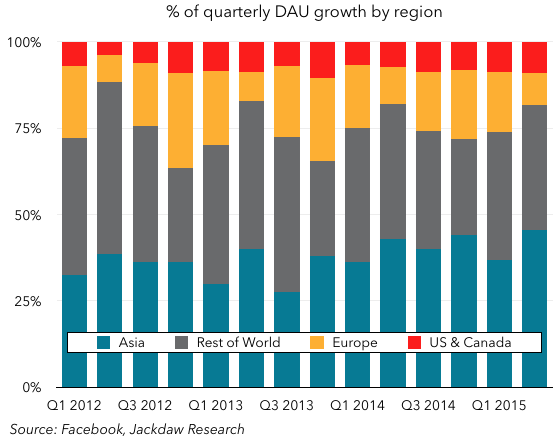

As a result, Asia also contributed in an outsized way to overall MAU growth, along with the “Rest of World” region, which obviously includes Africa as well as Latin America:

Asia and Rest of World combined accounted for 82% of the growth, with the US and Canada and Europe making up just 18%. Now, before you start ascribing all this growth to WhatsApp and other platforms that don’t monetize as well, no, those MAU numbers exclude WhatsApp, so this is all for the core Facebook platform. However, Asia is still monetizing at a much lower rate, with just 16% of ad revenues in the quarter, but a third of Facebook’s users. Part of that is because Asian users still engage with Facebook less than their peers in other regions, as measured by the DAU:MAU ratio:

Asia and Rest of World combined accounted for 82% of the growth, with the US and Canada and Europe making up just 18%. Now, before you start ascribing all this growth to WhatsApp and other platforms that don’t monetize as well, no, those MAU numbers exclude WhatsApp, so this is all for the core Facebook platform. However, Asia is still monetizing at a much lower rate, with just 16% of ad revenues in the quarter, but a third of Facebook’s users. Part of that is because Asian users still engage with Facebook less than their peers in other regions, as measured by the DAU:MAU ratio:

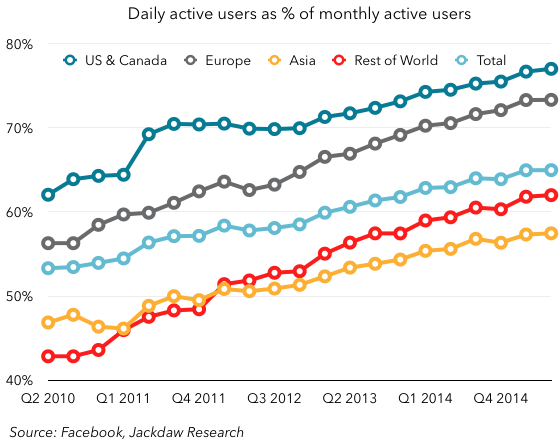

There are two ways to read that: Asian users continue to find less value in the platform, which is a bad thing, or the number is rising and Asian engagement today is almost where US engagement was five years ago, and will in time rise to similar levels. I’m inclined to believe the latter, though WhatsApp in particular but also things like allowing phone-number-based signup for Messenger are clearly moves to extend Facebook’s Asian base beyond its legacy product.

There are two ways to read that: Asian users continue to find less value in the platform, which is a bad thing, or the number is rising and Asian engagement today is almost where US engagement was five years ago, and will in time rise to similar levels. I’m inclined to believe the latter, though WhatsApp in particular but also things like allowing phone-number-based signup for Messenger are clearly moves to extend Facebook’s Asian base beyond its legacy product.

Mobile *is* Facebook today

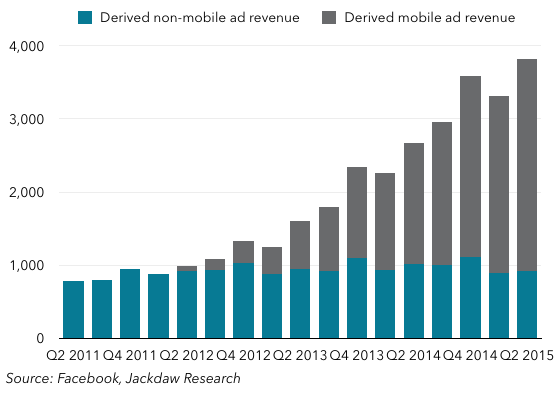

It’s not a new story, but mobile clearly *is* Facebook today, as it accounts for more than 100% of its growth as the desktop business declines. As an interesting thought experiment, imagine what might have happened to Facebook had it continued to dither on mobile ads back in 2012 rather than pursuing them aggressively as the IPO forced it to do:

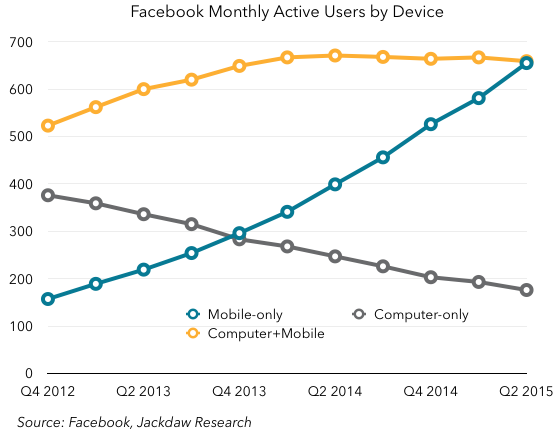

Essentially all of Facebook’s growth in the intervening period has come from mobile, propelling it from a billion dollar a quarter company to a four billion dollar a quarter company in the process, while non-mobile revenue declines. A big part of this is the transition in the way people use Facebook, as illustrated by its three major groups of users:

Essentially all of Facebook’s growth in the intervening period has come from mobile, propelling it from a billion dollar a quarter company to a four billion dollar a quarter company in the process, while non-mobile revenue declines. A big part of this is the transition in the way people use Facebook, as illustrated by its three major groups of users:

As you can see, mobile-only users just fell short of eclipsing mobile plus computer users as the largest single group by the end of Q2, but chances are they’re the biggest group by now, and the trend here is only going to accelerate. Both groups were about 44% of the total at the end of the quarter. One number Facebook doesn’t share is the split in time between computer and mobile usage for those users who spend time on both. But it did say that in the US Facebook accounts for 1 out of every 5 minutes people spend on smartphones, and that globally users spend 46 minutes per day on average across its properties (excluding WhatsApp). It’s likely that even for many of those multi-platform users, mobile dominates usage, which helps to explain the increasing dominance of mobile advertising.

As you can see, mobile-only users just fell short of eclipsing mobile plus computer users as the largest single group by the end of Q2, but chances are they’re the biggest group by now, and the trend here is only going to accelerate. Both groups were about 44% of the total at the end of the quarter. One number Facebook doesn’t share is the split in time between computer and mobile usage for those users who spend time on both. But it did say that in the US Facebook accounts for 1 out of every 5 minutes people spend on smartphones, and that globally users spend 46 minutes per day on average across its properties (excluding WhatsApp). It’s likely that even for many of those multi-platform users, mobile dominates usage, which helps to explain the increasing dominance of mobile advertising.

The new businesses

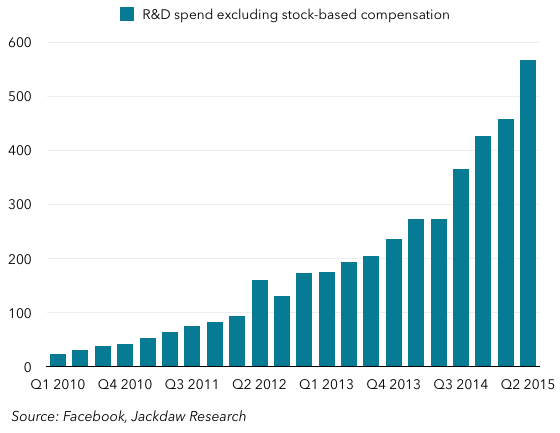

The only ongoing challenge at Facebook is these new businesses it has acquired or launched which aren’t yet generating revenue in meaningful numbers, while adding significantly to costs (especially in the R&D category). WhatsApp, Oculus, and Facebook’s search product are all generating very little revenue while costing a great deal to build. There’s apparently no urgency about monetizing search or WhatsApp better, while Oculus will ship its first consumer product early next year. But in the meantime R&D spend (which includes salaries for employees that aren’t working on monetized products) is skyrocketing:

A big part of that is hiring in R&D – of the 873 net new employees Facebook added in Q2, a majority were apparently in R&D. This, and the general investment in these new areas, is taking Facebook’s non-GAAP margins (which exclude stock based compensation) steadily downwards, though they’re still at fairly healthy levels. With the core business continuing to perform so well, I don’t think there’s any worry about this yet, but it’s something to watch going forward.

A big part of that is hiring in R&D – of the 873 net new employees Facebook added in Q2, a majority were apparently in R&D. This, and the general investment in these new areas, is taking Facebook’s non-GAAP margins (which exclude stock based compensation) steadily downwards, though they’re still at fairly healthy levels. With the core business continuing to perform so well, I don’t think there’s any worry about this yet, but it’s something to watch going forward.