This is, and isn’t, part of my series on tech companies’ Q2 2014 earnings. It is, because it uses Samsung’s Q2 earnings as a jumping off point, but it isn’t because it’s more of a think piece about where Samsung goes from here than being specifically about one quarter’s earnings.

The importance of Samsung’s mobile business

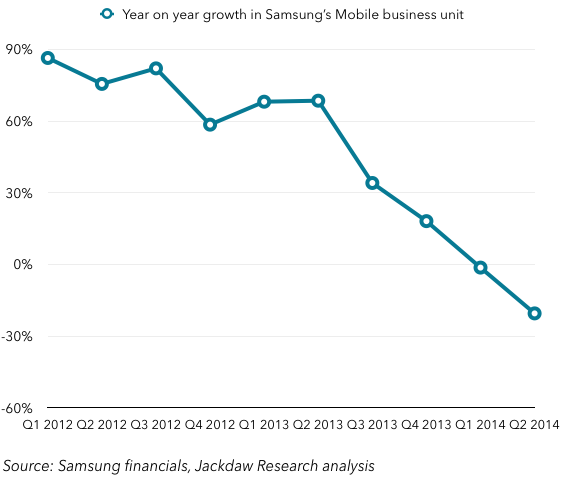

Having said that, let’s start with those Q2 earnings. Here’s the growth rate in mobile sales specifically (this is part of Samsung’s IT & Mobile (IM) business unit):

As you can see, growth has slowed dramatically over the last few quarters and dipped into the red in the last two. That trajectory isn’t looking good at all. Now, here’s the operating margin for the IM business unit as a whole (this includes Samsung’s much smaller PC business as well as tablets and smartphones):

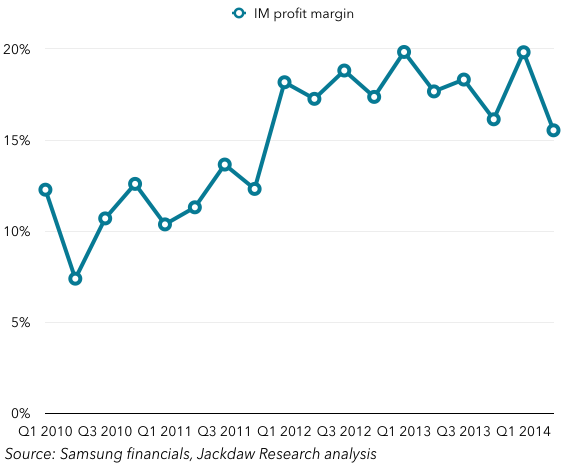

As you can see, growth has slowed dramatically over the last few quarters and dipped into the red in the last two. That trajectory isn’t looking good at all. Now, here’s the operating margin for the IM business unit as a whole (this includes Samsung’s much smaller PC business as well as tablets and smartphones):

The margin is bouncing around a bit but definitely dropped in the last quarter or so. Longer term, it was somewhat consistently between about 17-20%, but this quarter it dropped to just over 15%. Let’s now put this in the context of Samsung Electronics overall: the two charts below show that IM business unit as a percentage of revenues and operating profits:

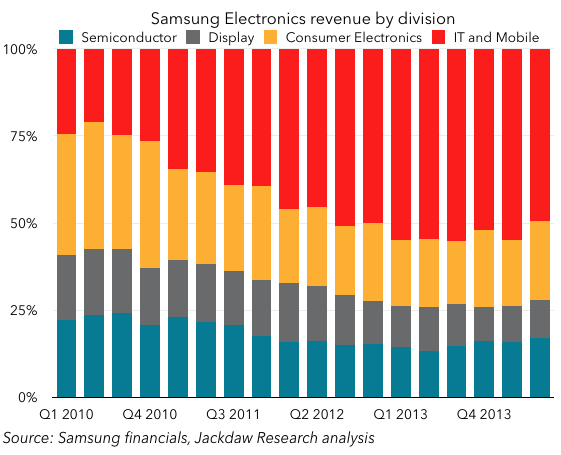

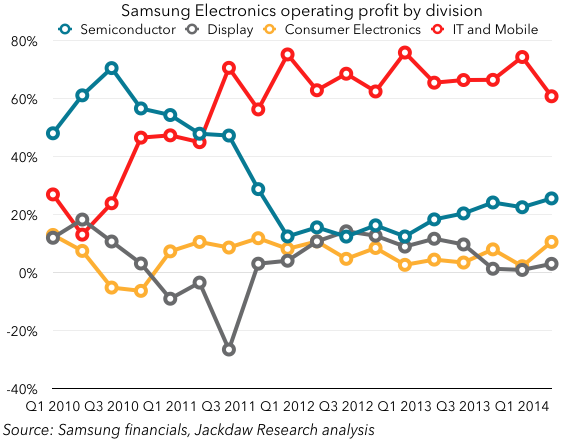

The margin is bouncing around a bit but definitely dropped in the last quarter or so. Longer term, it was somewhat consistently between about 17-20%, but this quarter it dropped to just over 15%. Let’s now put this in the context of Samsung Electronics overall: the two charts below show that IM business unit as a percentage of revenues and operating profits:

As you can see, since 2010 the IM business unit has come to represent about 50% of Samsung Electronics overall, but it has also been between 60% and 80% of the company’s operating profits. In addition, the two components divisions (semiconductors and displays) likely generate a significant amount of their revenue from making parts for Samsung’s own products.

As you can see, since 2010 the IM business unit has come to represent about 50% of Samsung Electronics overall, but it has also been between 60% and 80% of the company’s operating profits. In addition, the two components divisions (semiconductors and displays) likely generate a significant amount of their revenue from making parts for Samsung’s own products.

To sum up, then, trends in Samsung’s mobile business are not good, and that’s important because the mobile business is about half of revenues, well over half of operating profits, and drives revenue and scale for the other divisions of Samsung Electronics. If mobile starts to go seriously south, then the whole of Samsung Electronics will suffer with it.

Margins in consumer electronics

The question then becomes, is Samsung’s mobile business going to go south, and what does that actually mean? In a recent column on Techpinions I talked about the challenges Samsung faces at this time, and the fact that its chickens are now finally coming home to roost. I won’t re-hash all that here, but to summarize, Samsung’s failure to differentiate on software and services has left it vulnerable to competition from Chinese vendors able to create compelling hardware at much lower prices (and margins).

It’s worth a quick history lesson here to understand the implications of what happens when you’re a consumer electronics vendor in a competitive market, and you can’t truly differentiate your product. First, a short-term view of margins for other consumer electronics businesses, across smartphones, PCs, TVs and gaming:

I normally like to make my charts as clean and easy to read as possible, and this one is noisy, but that’s deliberate. It’s the overall effect rather than any individual line that’s important here. And the overall effect is that for the last two years, none of these companies or divisions has posted even a single quarter of operating margins above 10%. And for the vast majority of the three year period shown almost none of the companies has posted any quarters above 5%. This, then, is the reality of today’s consumer electronics business, across multiple sectors. All those articles about Samsung and Apple claiming ninety plus percent of the profits in smartphones? You can extend that to consumer electronics more broadly too, as they’re the only two major companies whose results aren’t shown in the chart. Everyone else makes paltry margins in this business, and many of them are unprofitable (see the noise below the 0% line in the chart as well as the clustering just above it).

I normally like to make my charts as clean and easy to read as possible, and this one is noisy, but that’s deliberate. It’s the overall effect rather than any individual line that’s important here. And the overall effect is that for the last two years, none of these companies or divisions has posted even a single quarter of operating margins above 10%. And for the vast majority of the three year period shown almost none of the companies has posted any quarters above 5%. This, then, is the reality of today’s consumer electronics business, across multiple sectors. All those articles about Samsung and Apple claiming ninety plus percent of the profits in smartphones? You can extend that to consumer electronics more broadly too, as they’re the only two major companies whose results aren’t shown in the chart. Everyone else makes paltry margins in this business, and many of them are unprofitable (see the noise below the 0% line in the chart as well as the clustering just above it).

You’ll notice that there are a couple of companies whose margins are above 10% in the early quarters of the chart above. So, now let’s take a longer-term view of a particular segment of the consumer electronics market, the one we’re talking about here: the mobile phone market:

This chart is also a bit noisy, but it’s a little easier to see the individual components on this one. (Note that the figure for Apple is for the whole company rather than phones specifically, since Apple doesn’t report operating margins at segment level, but Apple’s smartphone profits are significantly higher.) Here, we can see a number of other companies which spent some time with operating margins above 10%, including Nokia, HTC and BlackBerry (then RIM). None of them remains there today, of course, but what was different then? I theorize that there are four factors that allow consumer electronics vendors to make these unusually high profit margins:

This chart is also a bit noisy, but it’s a little easier to see the individual components on this one. (Note that the figure for Apple is for the whole company rather than phones specifically, since Apple doesn’t report operating margins at segment level, but Apple’s smartphone profits are significantly higher.) Here, we can see a number of other companies which spent some time with operating margins above 10%, including Nokia, HTC and BlackBerry (then RIM). None of them remains there today, of course, but what was different then? I theorize that there are four factors that allow consumer electronics vendors to make these unusually high profit margins:

- very rapid growth (allowing growth-sustaining cost increases to lag revenue increases)

- very high scale, driving economies, competitive leverage through buying up inventories, and so on

- premium products, which command higher prices and margins

- significant differentiation, which allows the vendor to charge higher prices because there is no direct competition.

Nokia benefited from huge scale and rapid growth in its heyday, HTC benefited from premium pricing (it is the only vendor other than BlackBerry and Apple ever to have maintained an average selling price over $300), and BlackBerry benefited from both premium pricing and differentiation. But none of them were able to maintain these advantages: Nokia stopped being competitive once smartphones took off, and saw rapid shrinkage and with it a decline in scale; HTC was unable to maintain its premium positioning and also lost what scale it had; and BlackBerry’s differentiation ceased to matter as iPhones and Androids became good enough.

On Samsung’s future

Samsung has benefited from three of these factors over the last few years, enjoying both rapid growth and huge scale and strong sales of its Galaxy S and Note smartphones at the premium end of the market. However, its differentiation was always its weakest suit (made up for by some extent by its massive marketing spend), and the other three factors are being eroded rapidly. Its growth has turned negative, as its growth reverses its scale benefits will suffer, and it is likely to start losing share in the premium market as its lack of differentiation causes loss of market share. At this point, I see three possible futures for Samsung:

- It continues as it has been, with minimal differentiation, attempting to compete at all levels of the market but finding it increasingly challenging to do so. It will face increasing competition at the bottom end from players willing to take more typical margins, and at the high end it will increasingly be butting its head against Apple’s dominance in an increasingly saturated market. In this scenario, Samsung’s operating margins in smartphones will rapidly retreat to the norm for consumer electronics vendors below 10%, a significant drop from where Samsung sits today. Revenue will fall too, and the combination of these two factors will dramatically reduce dollar operating profits. And with all this, the other divisions which sell parts to make Samsung’s mobile phones will suffer as well.

- Samsung doubles down on hardware but accepts lower margins, preferring instead to leverage the advantages conferred by its scale and vertical integration. It competes on price at the low and mid end, joining the Chinese vendors at their own game, and preserves share better than it is currently able to do. It attempts to compete at the high end too and has some success, but its star begins to fade here.

- Samsung finally begins to take software and services seriously, creating a layer of value on top of Android which consumers find compelling rather than merely annoying, and creating true differentiation in this manner. This is a hugely steep hill to climb, and I remain skeptical that Samsung is culturally able to embrace this route to success. A fuller embrace of Tizen is also potentially part of this picture, but recent moves suggest Samsung is moving away from, rather than towards, such a strategy.

- Lastly, Samsung could consider something totally different: Stefan Constantinescu made a fascinating suggestion on the Tab Dump blog today, to wit: Samsung should “do a Qualcomm” and focus more aggressively on making parts for other vendors. It’s definitely thinking outside the box, but I’m starting to think that thinking a little laterally might not be a bad thing for Samsung at this point.

Whatever the future for Samsung, it’s going to look a lot less like the last four years and a lot more like the fate of other consumer electronics vendors which failed to differentiate.