Having not written about BlackBerry for months, I’m now doing two posts in one week! Normal service will resume shortly. But I did want to quickly cover BlackBerry’s earnings today, because as usual many of the people covering them are misunderstanding what’s happening and focusing on the headlines instead of the underlying trends.

First off, BlackBerry’s results look horrible on the face of them. It’s losing money, it’s shrinking, it’s hardly selling any devices, and so on and so forth. If you compare them to almost any other handset vendor out there, they come off looking pretty bad. But looking at BlackBerry as just another handset vendor is making the very mistake I warned against in my post earlier in the week. BlackBerry’s future involves devices, to be sure, but it goes well beyond them. So here’s a quick take on what I see by way of underlying trends at BlackBerry.

Device shipments

Since so many people are fixated on device shipments, let’s start there. The headline here is that shipments fell significantly year on year, which is usually the best comparison to make to avoid focusing on seasonal trends. However, when a company is in turnaround mode, it’s worth looking at quarter on quarter trends too. In addition, the real number to focus on is sell through and not shipments, because that reflects what the company is actually selling without the effect of reductions in inventory. The chart below shows three key metrics related to the company’s device sales for the last few quarters:

Taking each of those lines in turn:

Taking each of those lines in turn:

- Shipments have actually been improving for two straight quarters, leading to actual growth in hardware revenues (as we’ll see below). This is the official financial metric, but it represents sales into the channel, not sales to end users, which means that it can be influenced by channel stuffing.

- Sell-through has also been stabilizing a little after several quarters of declines. It’s now a little over 2 million per quarter, which is tiny by the standards of other device vendors, but reflects BlackBerry’s niche appeal. I would not expect this number to grow very significantly going forward, perhaps peaking at 4-5 million at a maximum per quarter.

- Inventory reductions: the difference between the two previous numbers is the reduction in inventory – to the extent the company ships more devices than it sells through, inventories are growing, and to the extent is sells more than it ships, inventories are shrinking. For the past year, inventories have indeed been shrinking, though the pace of shrinkage is now slowing. That means that shipments and sell-through will likely soon be in alignment.

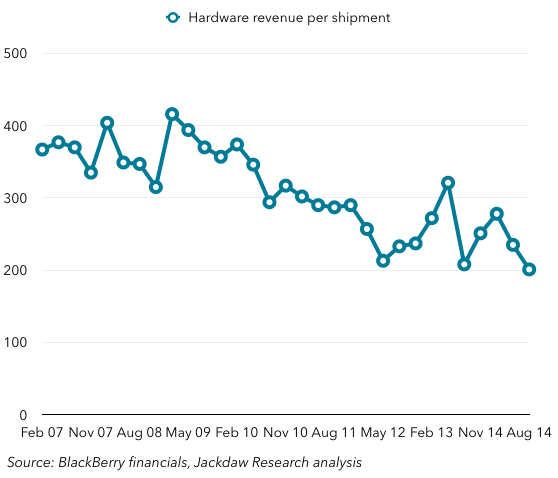

At the same time, the type of devices BlackBerry now sells, and the average price at which it sells them, continues to change significantly. The company no longer reports average selling prices, but it does report hardware revenue and the number of shipments, and so we can calculate an average price per shipment, as shown below:

As you can see, the average selling price has fallen significantly since 2007 and 2008, when it briefly went over $400. In this past quarter, the average price was just over $200. This reflects partly the mix of devices sold, which is heavily skewed towards the cheaper devices sold in emerging markets in particular, and partly the heavy discounts on some devices as BlackBerry sought to clear out inventory on the initial BB10 devices ahead of new devices launching this year. It will be very interesting to watch what happens as the inventory shedding comes to an end and new devices such as the Passport and Classic launch.

As you can see, the average selling price has fallen significantly since 2007 and 2008, when it briefly went over $400. In this past quarter, the average price was just over $200. This reflects partly the mix of devices sold, which is heavily skewed towards the cheaper devices sold in emerging markets in particular, and partly the heavy discounts on some devices as BlackBerry sought to clear out inventory on the initial BB10 devices ahead of new devices launching this year. It will be very interesting to watch what happens as the inventory shedding comes to an end and new devices such as the Passport and Classic launch.

Margins affected by one-time items

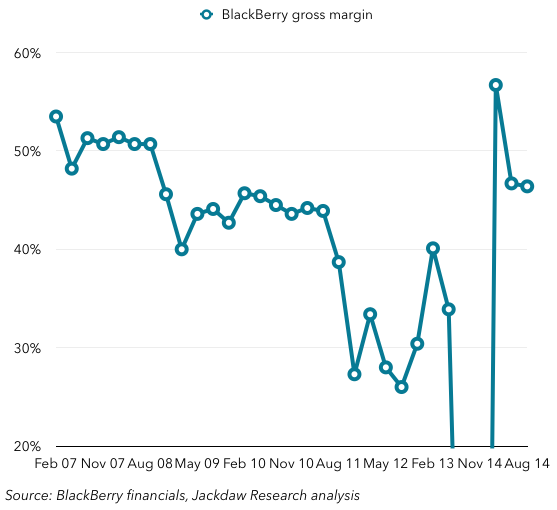

I’ve seen some pieces this morning saying that margins worsened quarter over quarter. This is true on a reported basis, but it ignores the fact that the company had a one-time gain last quarter from the sale of some assets and a tax refund. If you strip that out, profitability actually improved quarter on quarter. And that’s because of two things: gross margins have bounced back to where they were long ago, while operating costs have been reduced significantly, largely due to the significant restructuring initiated by previous CEO Thorsten Heins and recently completed under John Chen. Here’s the gross margin line (which I’ve clipped at 20% because there were two quarters when margins were literally off the charts, which distort the whole picture):

What you can see is that gross margins are now back up where they were in 2010, at what was to be BlackBerry’s peak in many ways. And they haven’t just been there for one quarter, but several quarters now. That’s a significant recovery, and BlackBerry specifically reported that hardware gross margins were positive in this quarter. Getting back to positive gross margins on hardware is a huge achievement given the massive reduction in the number of shipments. But it needs to go much further, so that hardware is generating significant margins for the company again in addition to those it garners from software and services.

What you can see is that gross margins are now back up where they were in 2010, at what was to be BlackBerry’s peak in many ways. And they haven’t just been there for one quarter, but several quarters now. That’s a significant recovery, and BlackBerry specifically reported that hardware gross margins were positive in this quarter. Getting back to positive gross margins on hardware is a huge achievement given the massive reduction in the number of shipments. But it needs to go much further, so that hardware is generating significant margins for the company again in addition to those it garners from software and services.

Revenue growth is improving though still negative

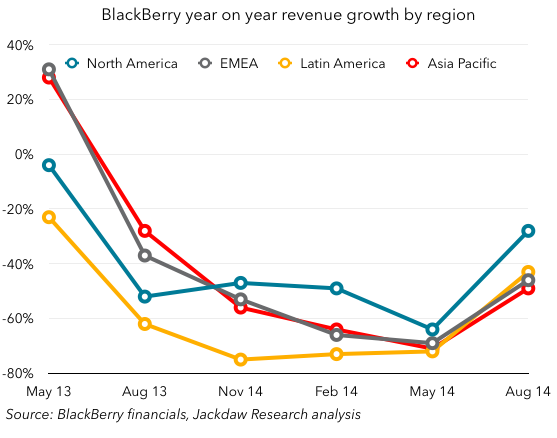

Again, revenue growth is negative, but the underlying trends are positive. Following quite a few quarters of dramatic declines as the hardware business imploded, BlackBerry is starting to turn things around. Below are quarter on quarter and year on year revenue growth trends by region:

You can see that both have turned around in recent quarters, though they’re both still negative in almost all regions. But North American revenues actually grew quarter on quarter this time, and year on year the rate of shrinkage is much slower in all regions. There’s still a way to go to get to positive growth again, but things are moving in the right direction. Again, the BlackBerry story at present is not about absolute results but about the trajectory.

Revenue mix has shifted and continues to shift

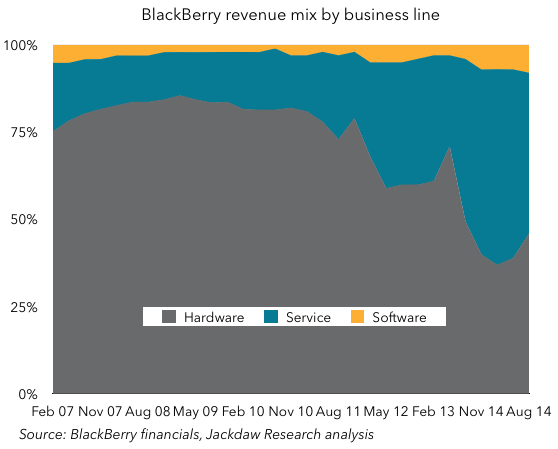

BlackBerry’s revenue mix has shifted significantly as hardware revenues have declined and services revenue has held up better.  As you can see, devices revenue is now less than half the company’s overall revenue, while services represents about the same proportion in its own right (both were at 46% this quarter). This is the shape of things to come, though I would expect device revenue to continue its slow recovery to over 50% in the short term, as sales improve and since service revenues are something of a lagging indicator.

As you can see, devices revenue is now less than half the company’s overall revenue, while services represents about the same proportion in its own right (both were at 46% this quarter). This is the shape of things to come, though I would expect device revenue to continue its slow recovery to over 50% in the short term, as sales improve and since service revenues are something of a lagging indicator.

Service revenues today are dominated by enterprise device management services, heavily tied to the company’s sales of BES (both in its former and current instantiations). But that revenue stream will need to diversify over time as well. BBM is one source of revenue which should start to grow as the company increasingly seeks to monetize that. On that front, one promising metric from the latest results was that monthly BBM users actually rose by 6 million from 85m to 91m in the quarter. That’s impressive as BlackBerry’s device installed base is likely under 50 million at this point, so almost half of those are on non-BlackBerry devices. Monetizing those will be key, though, if this business is to be worth pursuing.

Final thoughts

Lest anyone misunderstand me, I’m not suggesting that all is hunky dory at BlackBerry, or that it’s an imminent threat or likely future success story in the devices market. The company still faces very significant challenges, both in turning around its devices business and in expanding beyond devices into software and services that aren’t directly tied to BlackBerry handsets. Its financials are still rocky, and could still take a turn for the worse. But I believe that John Chen understands the challenge ahead of it, he seems impressively candid about BlackBerry’s prospects, and he has a great handle on what the company needs to do to turn itself around. None of the opportunities ahead of BlackBerry – M2M, BBM or enterprise managed mobility (EMM) – are straightforward or guaranteed home runs. Strong competitors exist in each of those markets, and BlackBerry’s value proposition is still nascent in each of them. But the underlying trends suggests BlackBerry is indeed starting to turn a corner, and is gearing up for the next phase in its history.