This is something I’ve though about quite a bit, and even wrote about briefly as part of a much longer piece ahead of the launch of Apple Music, but I feel like no-one is really talking about. But it’s potentially quite significant for the economics of Apple Music, and especially the per-stream payout rate Apple will end up passing on to labels and artists. Note: it’s already clear that Apple will have a higher per-stream payout simply based on the fact that it’s a paid-only service, whereas Spotify and other large services mix paid and free users. But I’m talking about an additional impact on top of that.

Integration of owned music is the key

The big factor here is Apple’s integration of the music you already own and store in iTunes into the Apple Music experience and into a single app. I think that’s huge for usability, and that was the key point in that earlier piece, but I think it could also be quite significant for the economics of the service. Why is that? Well, with almost any other subscription streaming service, you as the user tend to start from scratch in terms of your existing library. Perhaps you hop back and forth between apps when you play the music you own versus the music you’re streaming, but I’d guess many people just stick to a single app and play all their music from there, even the stuff they may have purchased somewhere along the way, because it’s all available in the streaming service and it’s easier to play it there than switch apps. Services like Spotify will pay out to artists regardless of whether the user already owns the track somewhere else (unless the user has imported their owned music). But when the user’s owned music is also available in the app, Apple won’t have to pay out when the user plays that music.

What’s really hard to know here is the balance between owned versus streamed music the average user plays during the course of a typical month. I know my own usage is heavily skewed towards the music I own and am familiar with, along with a few tracks or albums I don’t own and stream instead. Perhaps others are different, but I’d guess almost all users would spend a significant amount of time playing music they already own. With other services, the provider still has to pay out on this music because it all looks the same, but with Apple Music there will be a clear line between the music the subscriber owns and the music he or she is streaming through the service (even if it’s presented together in the context of the app). If the amount that’s played from the library rather than streamed is significant, this could substantially reduce the number of plays for which payments need to be made.

A higher per-stream rate on Apple Music

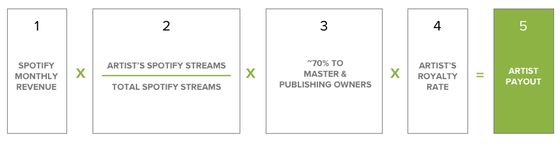

At this point, it’s worth thinking about how the economics of streaming music work. Although we often see per-stream rates used in discussions of how much artists get paid through these services, the reality is that there are no set per-stream rates. Rather, these services share some proportion of their overall revenue from subscribers and/or advertisers with those labels and artists whose music their subscribers listen to. The total pot is divided up with labels and artists according to a standard formula, and I’ve pasted the graphic Spotify uses to illustrate this formula below:

Once you understand that it’s a matter of dividing up the total pot, it becomes very relevant how many songs are streamed and therefore get to share in that pot. If Apple Music has fewer songs streamed through the service (because a significant proportion are played instead from users’ libraries), that in turn could dramatically increase the per-stream payout for those artists whose music is streamed. That will likely disproportionately benefit new artists and music over older artists and albums, which could be particularly good for those discovered through the service.

Of course, over time, this advantage will be mitigated as the balance between owned and streamed music shifts towards streamed music, as people will likely buy far less music (if any) going forward. But as the first Apple Music subscribers get past their trial periods and Apple starts paying out on its long-term formula, this could result in significantly higher payments per stream than other services. Add this to the existing advantage Apple has over competing services because of the paid-only nature of the service. Over time, that could have a really interesting impact on artists’ willingness to continue to work with other services. If, as an artist, you’re getting paid several times more on Apple Music per stream than on Spotify, Rdio, or Deezer, would you eventually consider pulling at least some of your music from those other services?

Note: I’m making a fundamental assumption here, which is that Apple will only pay out on plays of music the user doesn’t play from his or her own library. That seems a reasonable assumption, but I haven’t confirmed it. I can’t see why Apple would pay out on that music (unless it’s played through iTunes Match, which shares 70% with artists too), but it’s a remote possibility that it will, in which case the argument falls apart.