I’m continuing my look at consumer tech companies’ earnings with a quick review of Netflix’s results released today. The whole series is available here, and last quarter’s analysis is here.

DVD by mail: Netflix’s dial-up business

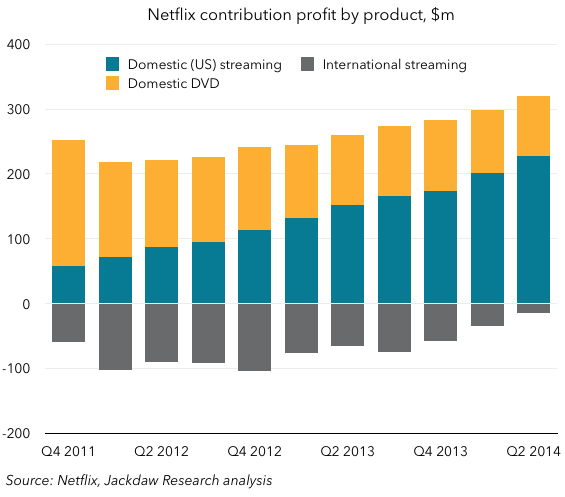

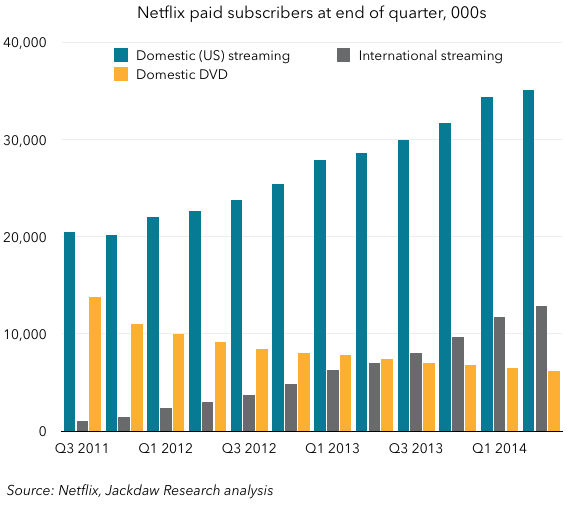

Netflix has three products, with very different characteristics: domestic streaming, domestic DVD by mail, and international streaming. Domestic DVD is to Netflix what the dial-up business is to AOL, which is to say it’s a legacy business in which the company is no longer investing, and which therefore has very steady fixed costs and essentially zero sales and marketing cost. As such, it’s very profitable:

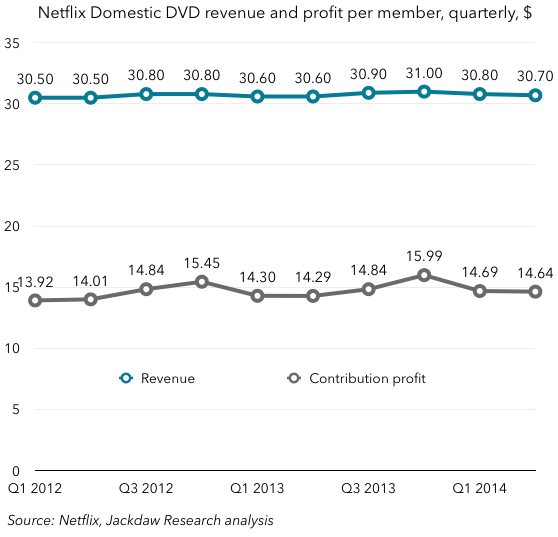

Netflix generates a very predictable $10 or so per month from these subscribers, and half of that is profit. That’s a really great business to be in, and it helps to fund and offset the other parts of Netflix’s business.

Netflix generates a very predictable $10 or so per month from these subscribers, and half of that is profit. That’s a really great business to be in, and it helps to fund and offset the other parts of Netflix’s business.

International streaming: tantalizingly close to profitability

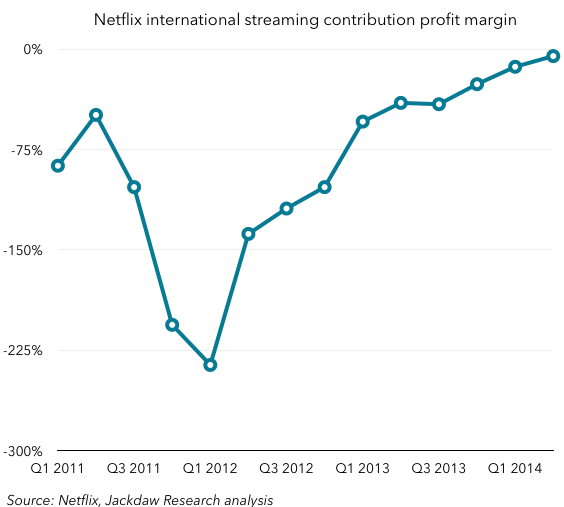

On the other side of the equation is the international streaming business, which has been consistently unprofitable for quite some time. However, it came tantalizingly close to profitability this past quarter:

Just as it begins to approach profitability, though, Netflix is going to push hard to expand into other markets where it doesn’t yet have a presence. That’s not a coincidence either – the company said on earlier earnings calls that it saw itself achieving profitability in its existing international markets later this year, and it’s that result that’s given it the confidence to launch in additional markets.

Just as it begins to approach profitability, though, Netflix is going to push hard to expand into other markets where it doesn’t yet have a presence. That’s not a coincidence either – the company said on earlier earnings calls that it saw itself achieving profitability in its existing international markets later this year, and it’s that result that’s given it the confidence to launch in additional markets.

Interestingly, these two businesses are essentially replacing each other in Netflix’s overall customer base:

From Q3 2011 to Q3 2013 these two subscriber bases – domestic DVD and international streaming – essentially canceled each other out, with total subs between those two categories at about 15 million at the beginning and end of that period. But over the last few quarters, international streaming has been growing significantly faster than domestic DVD is shrinking.

Domestic streaming: becoming increasingly profitable

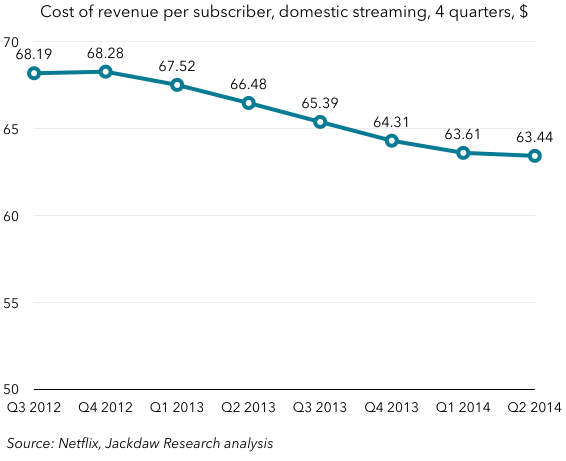

At the same time, domestic streaming has been growing fast, and has actually been getting more profitable over time. Part of the reason is that there are certain fixed costs being spread over more and more subscribers, and as such the cost of revenue per subscriber for domestic streaming has been falling (note that the axis starts at $50, not zero, so as to make the trend clearer):

That’s still a pretty significant cost per subscriber per year, and it’s flattened out lately. Think about it in the context of Amazon Prime Instant Video, which is a similar business with a slightly smaller content library but also far fewer subscribers. Amazon is likely carrying a pretty similar cost per subscriber but having to fund it out of a product (Prime) that also has to cover free shipping, the Kindle Lending Library and now Prime Music too. No wonder it increased prices for Prime recently (as I talked about back when the news was announced).

That’s still a pretty significant cost per subscriber per year, and it’s flattened out lately. Think about it in the context of Amazon Prime Instant Video, which is a similar business with a slightly smaller content library but also far fewer subscribers. Amazon is likely carrying a pretty similar cost per subscriber but having to fund it out of a product (Prime) that also has to cover free shipping, the Kindle Lending Library and now Prime Music too. No wonder it increased prices for Prime recently (as I talked about back when the news was announced).

Growth prospects are uncertain

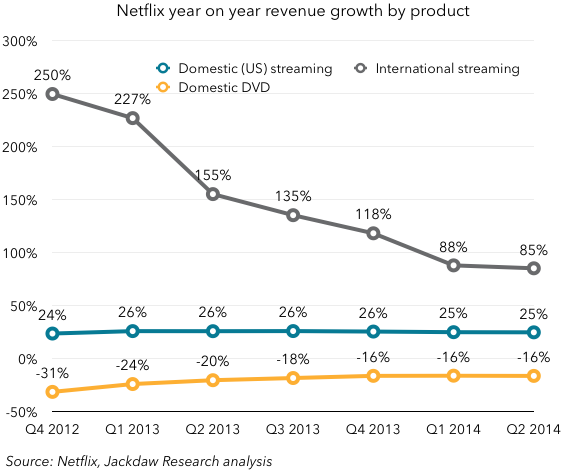

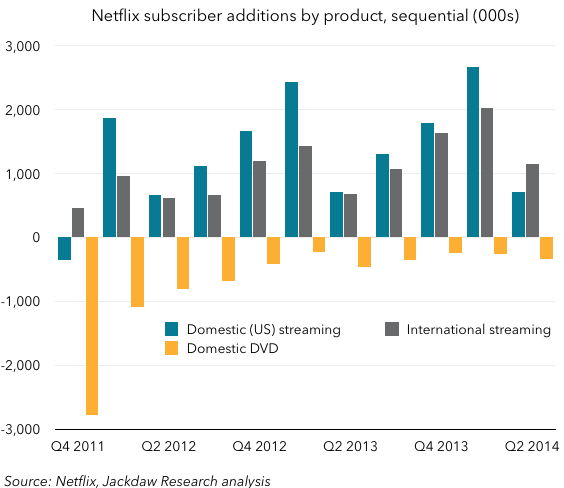

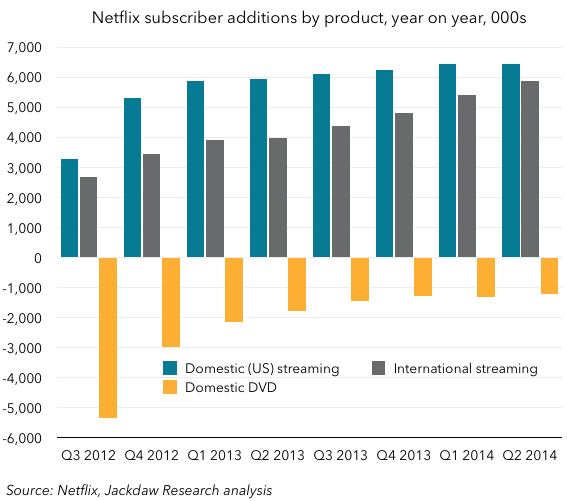

Growth rates at present are very strong in both of the businesses Netflix is investing in, as shown in the charts below: Revenue growth has actually been improving for all three products, although it is of course still negative for the DVD business. The domestic streaming business grows very consistently at 25% or so year on year, while the international streaming business is starting to face the reality of the law of large numbers and is slowing in percentage terms. The charts below show the number of new subscribers added sequentially and year on year:

Revenue growth has actually been improving for all three products, although it is of course still negative for the DVD business. The domestic streaming business grows very consistently at 25% or so year on year, while the international streaming business is starting to face the reality of the law of large numbers and is slowing in percentage terms. The charts below show the number of new subscribers added sequentially and year on year:

What you can see is that the international streaming business added more subscribers than the domestic streaming business for the first time in Q2, and on a yearly basis it’s just about to catch up with the domestic streaming business. That makes sense, given that Netflix already has about 120 million broadband households to target outside the US, about 50% more than in the US, and it will expand that number to 180 million by the end of the year.

What you can see is that the international streaming business added more subscribers than the domestic streaming business for the first time in Q2, and on a yearly basis it’s just about to catch up with the domestic streaming business. That makes sense, given that Netflix already has about 120 million broadband households to target outside the US, about 50% more than in the US, and it will expand that number to 180 million by the end of the year.

But of course there’s a ceiling to growth in each market where Netflix operates, especially with an essentially fixed revenue per member. In the US, its 35 million paid streaming subscribers already represent almost half of US broadband households. And overseas, the average spend on pay TV services is significantly lower than in the US. Though that isn’t a perfect indicator for the propensity to spend on Netflix, it likely will be a factor in capping Netflix’s appeal. The expansion in the number of countries where Netflix operates is critical to keeping international growth going, and so it should continue to see good overall growth for several more years. But eventually Netflix will see the same challenge as every single-product business: revenue growth requires expansion into new products. But there’s no sign that Netflix’s management is even thinking about this yet. That’s fair enough given its current growth rates, but it would be a good question for financial analysts to raise on the next earnings call.

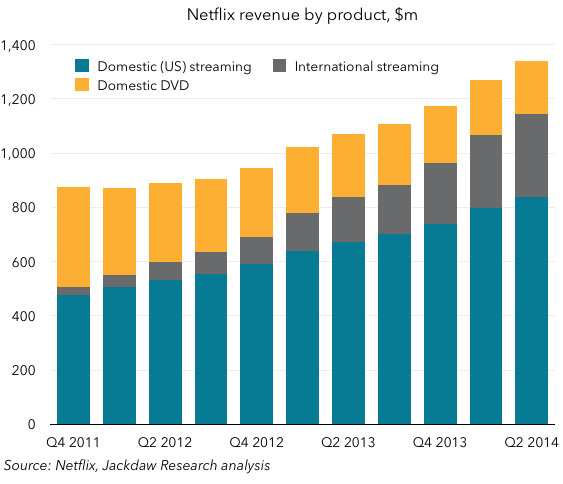

Overall revenues and margins

Just to round things out, below are a few charts that show how overall revenues, profits and margins shake out, given the foregoing analysis: