This will probably be the last in my series of posts about big tech companies’ Q1 2014 earnings. There was lots of press coverage of Sony’s earnings over the last several weeks, most of it for the wrong reasons – guidance revised downward, forecasting a loss for the next financial year and so on. There are plenty of pundits saying that if Sony was an American company, there would have been calls for Kaz Hirai’s resignation by now. But I wanted to take a minute and review some of the latest numbers, and highlight some of the positive trends in Sony’s business.

Sony has a reputation as a dysfunctional company (and I’ve said as much myself), with a combination of assets that seem like they could be really powerful but with cultural, structural and political divisions between business units that have so far prevented that enormous potential from turning into real achievement. Its glory days are long since behind it, and it’s struggled both to generate a profit and to demonstrate that it can again become the powerhouse it once was.

One quick note: Sony’s financials as reported have benefited from the weakness of the Yen relative to other currencies, and so some of the revenue growth it’s seen is unrelated to the performance of its own business, so I’ll try to use other metrics in addition to revenue growth wherever possible below.

A business in many parts

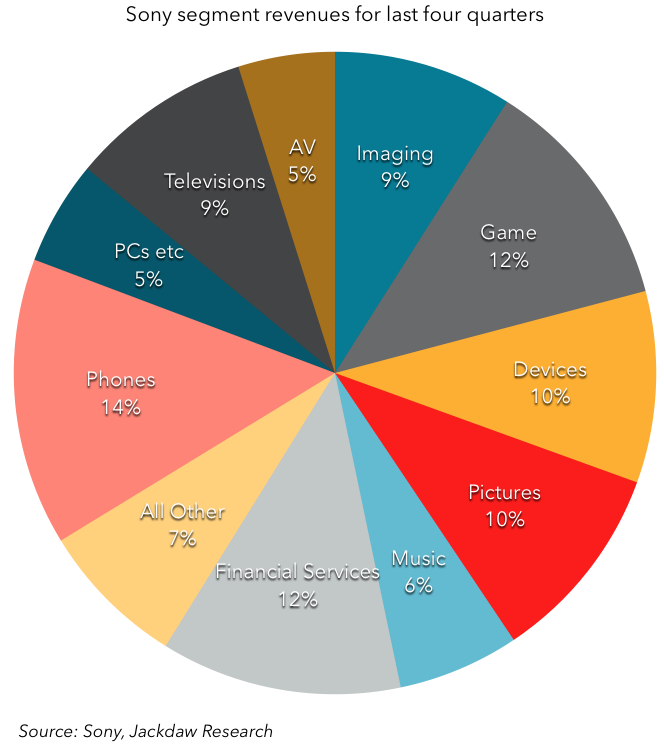

The most striking thing about Sony’s business is that it has so many parts to it – this is a company with its fingers in a lot of pies. Just look at the split of revenues shown in the pie chart below (I’ve taken some of the top-level segments and further divided them into their constituent parts because some of the sub-segments are actually quite different as well):