Note: this is part of a series on major tech companies’ earnings in Q4 2014 (click here for previous posts). In this post as elsewhere, I’m using calendar quarters (e.g. Q4 2014) to designate reporting periods, even though Lenovo and certain other companies have fiscal years which use different designations. Q4 2014 in this post and elsewhere refers to the quarter ending December 2014.

Lenovo reported its results yesterday, and although I have not traditionally covered Lenovo in depth here, I wanted to examine something specific: that is, the impact of the Motorola acquisition on Lenovo’s reported numbers. As such, I’m going to highlight a handful of charts here, but I’m also sending a deck on Lenovo with quite a few more charts to subscribers (if you’d like more information or to sign up, click here).

One quick note: the acquisition of Motorola closed in October, but Lenovo also acquired IBM’s server business around the same time. As such, not all the impacts described below are entirely due to the Motorola acquisition, though several are, and I’d estimate the Motorola acquisition had a significantly greater impact than the server business did. Lenovo reported a full quarter of System X (server) results in its reporting, and two months of Motorola results.

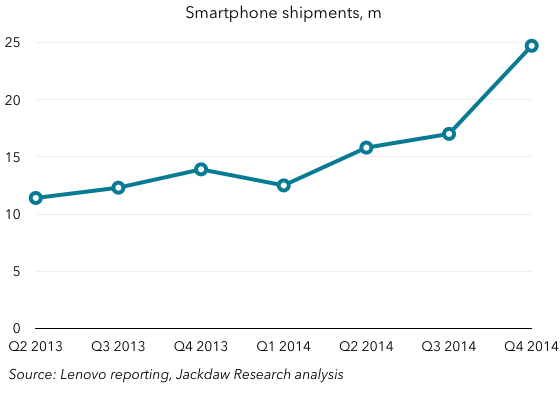

Smartphone shipments

The most obvious impact of the Motorola acquisition was a dramatic rise in smartphone shipments reported by Motorola. The chart below shows the trend line, with a very clear bump in Q4:

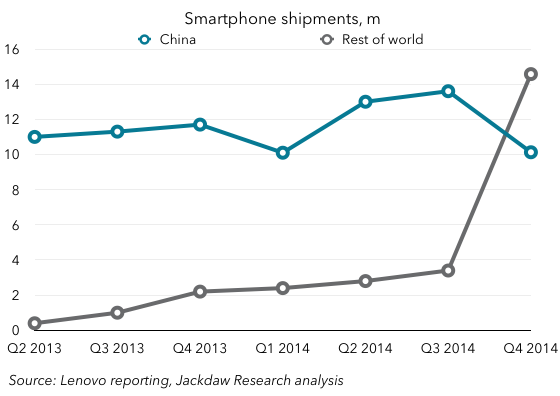

It’s worth noting, however, that shipments have been growing at Lenovo even before the Motorola acquisition. In my mind, the company has been one of the more successful and stable players in this space over recent years. However, that success has come largely in China, which has dominated shipments in the past. So another impact from the Motorola acquisition is the change in that mix:

It’s worth noting, however, that shipments have been growing at Lenovo even before the Motorola acquisition. In my mind, the company has been one of the more successful and stable players in this space over recent years. However, that success has come largely in China, which has dominated shipments in the past. So another impact from the Motorola acquisition is the change in that mix:

Hopefully you’ll notice two things here. First, and perhaps most obvious, is the spike in rest-of-world shipments in Q4, which rose from under 4 million a quarter to over 14 million. Motorola shipped 10.6 million devices in Q4 alone, so it accounts for the majority of those rest of world shipments. Secondly, you may notice that China shipments actually fell year on year and quarter on quarter. Shipments rose from Q3 to Q4 in 2013, and this dip is fairly significant. It’s quite likely that Lenovo, like Xiaomi, suffered from the impact of Apple’s new iPhones in China in Q4. What’s worth watching is whether this recovers in Q1.

Hopefully you’ll notice two things here. First, and perhaps most obvious, is the spike in rest-of-world shipments in Q4, which rose from under 4 million a quarter to over 14 million. Motorola shipped 10.6 million devices in Q4 alone, so it accounts for the majority of those rest of world shipments. Secondly, you may notice that China shipments actually fell year on year and quarter on quarter. Shipments rose from Q3 to Q4 in 2013, and this dip is fairly significant. It’s quite likely that Lenovo, like Xiaomi, suffered from the impact of Apple’s new iPhones in China in Q4. What’s worth watching is whether this recovers in Q1.

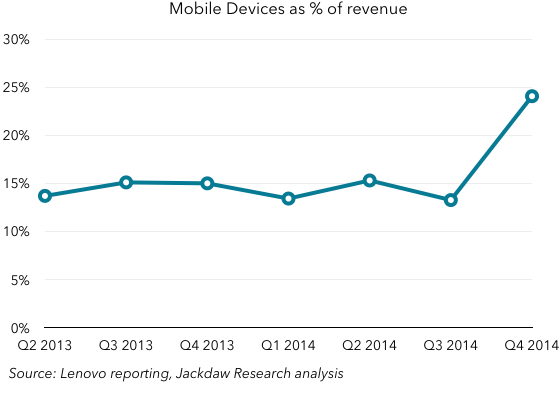

Mobile as a contribution to revenues

Until Q3 2014, Lenovo’s business was dominated by revenues from PCs. PCs contributed nearly 90% of Lenovo’s revenues two years ago, and it’s always stayed above 75%. That business, too, has performed well over recent years, despite the difficulties in the overall market, and so this dominance happened despite the growth in Lenovo’s smartphone and tablet businesses. But with the acquisition of Motorola, Mobile Devices suddenly went from around 15% of its revenues to almost a quarter: This is helpful for Lenovo particularly because of the overall headwinds in the PC space. PCs have continued to grow for Lenovo, but lessening its dependence on this business while exposing itself to the upside in smartphones is critical for Lenovo’s future growth, and the Motorola acquisition helps significantly with the balance of these two businesses.

This is helpful for Lenovo particularly because of the overall headwinds in the PC space. PCs have continued to grow for Lenovo, but lessening its dependence on this business while exposing itself to the upside in smartphones is critical for Lenovo’s future growth, and the Motorola acquisition helps significantly with the balance of these two businesses.

Regional impact

We’ve already looked at the impact of Motorola on smartphone shipments outside the US, but the other big impact from this is the share of revenues from different regions. Motorola’s revenue contribution is essentially recorded in the Americas segment, and you can see the impact in this next chart:

Note the dramatic growth in the size of that Americas block in Q4 2014 (again, the Motorola acquisition wasn’t the only contributor, as the IBM server business is also US-based). EMEA also grew a little, while China and AP remained fairly steady.

Note the dramatic growth in the size of that Americas block in Q4 2014 (again, the Motorola acquisition wasn’t the only contributor, as the IBM server business is also US-based). EMEA also grew a little, while China and AP remained fairly steady.

Margin impact

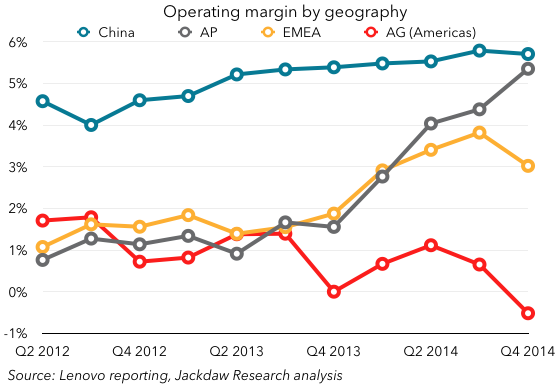

The impact of the two acquisitions can perhaps be most clearly seen in the regional segment margins Lenovo reports. The chart below shows these:

Margins in China and AP were essentially unaffected by the acquisitions, with AP rapidly catching up with China’s margin levels. But Americas margins dipped into the red for the first time in a long time in Q4, and EMEA margins also dipped somewhat. This is the downside to adding both the new businesses: neither was profitable under its previous owner. With the significant growth in smartphones year on year at Motorola, and efforts to get the Motorola brand back into China, together with various synergies, Lenovo expects Motorola to become profitable within about 18 months of the close of the deal. But in the meantime, Motorola’s results will be something of a drag on overall results.

Margins in China and AP were essentially unaffected by the acquisitions, with AP rapidly catching up with China’s margin levels. But Americas margins dipped into the red for the first time in a long time in Q4, and EMEA margins also dipped somewhat. This is the downside to adding both the new businesses: neither was profitable under its previous owner. With the significant growth in smartphones year on year at Motorola, and efforts to get the Motorola brand back into China, together with various synergies, Lenovo expects Motorola to become profitable within about 18 months of the close of the deal. But in the meantime, Motorola’s results will be something of a drag on overall results.

I’m generally very bullish on Lenovo and the Motorola acquisition. I wrote more about it on Techpinions recently.

Below, I’ve pasted a screenshot of the Lenovo deck which will be going to subscribers shortly.