On Tuesday, Apple is due to report its results for the March 2016 quarter (Q1 2016 according to the consistent calendar labeling I use for these things on this blog). A major focal point in the earnings report will be iPhone sales, which Apple has already guided will be down year on year. I’ve been contacted by quite a few reporters to ask – in various ways – whether this is bad news for Apple. The thought I’ve tried to articulate in response is that the current quarter is best seen in the context of what you might call the iPhone 6 blip.

What I mean by this is that, if you look at iPhone sales growth over the several years before the introduction of the iPhone 6, there was a fairly clear pattern emerging – one of slowing year on year growth. Growth declined from an average of around 100% in 2011 to around 50% in 2012 to just 15% in 2013, and over the three quarters before the iPhone 6 was introduced, growth rates slowed by roughly 1 to 1.5% quarter on quarter, for an average of 15%. All of this was a sign of the increasing maturity of both the overall smartphone market and the iPhone in particular. Following a rapid expansion into new markets over the years from 2007-2011, Apple was approaching saturation of the available distribution channels, and many of those already in the smartphone market who could afford to buy an iPhone had one or one of its high-end Android competitors. Absent significant switching from Android to iPhone driven by a major change in the addressable market, that’s how things would have likely progressed.

Of course, what happened in late 2014 was that Apple introduced the iPhone 6 and 6 Plus, which did dramatically increase the addressable market for iPhones and drive significant Android switching. The result? A massive increase in the iPhone growth rate, to 46% in Q4 2014, 40% in Q1 2015, and 35% in Q2 2015. For some, this was the new normal for Apple, driving sky-high growth rates in a product that had appeared headed for only modest growth in a saturating smartphone market. Now that the iPhone 6 year is past, however, we’ve seen the first flat year-on-year quarter for the iPhone, and are about to witness the first year on year decline. Hence all the calls from reporters about whether we’re witnessing some sort of crisis.

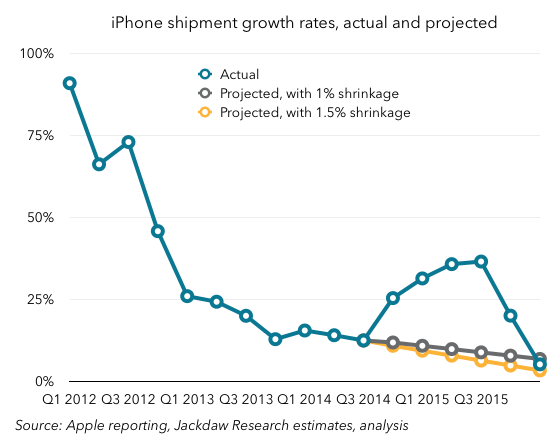

The reality is that the iPhone 6 line really just caused a blip in the long-term trajectory of the iPhone. It’s impossible to know what iPhone sales would have done absent the introduction of the iPhone 6, but we can at least have a go at projecting sales on the basis of the prior trajectory. Given that growth rates were slowing by roughly 1-1.5% per quarter before the iPhone 6 launch, that provides a good starting point for such an exercise. The chart below shows the actual year on year growth rate (using 51m as a consensus from the professional Apple analysts) and the two projected rates based on 1% and 1.5% quarter on quarter slowing in growth. You can see the blip extremely clearly here: Now, if you apply those growth rates to iPhone sales to project what would have happened if Apple had continued as before without the massive bump from the larger iPhone 6 phones, you get this second chart. It shows actual sales (in blue), as well as projected sales using those slowing growth rates in gray and yellow:

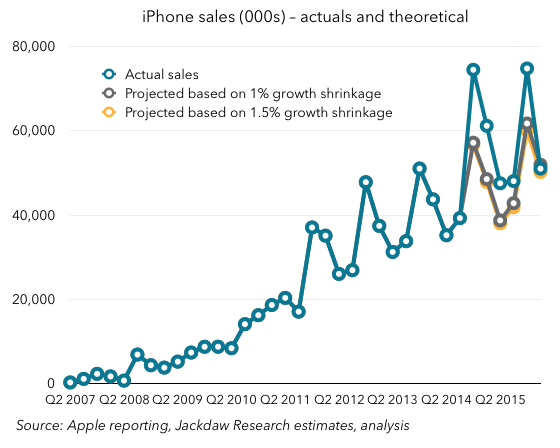

Now, if you apply those growth rates to iPhone sales to project what would have happened if Apple had continued as before without the massive bump from the larger iPhone 6 phones, you get this second chart. It shows actual sales (in blue), as well as projected sales using those slowing growth rates in gray and yellow: It’s a bit hard to tell exactly what’s going on in a chart with so much history, but I’ll zoom in a little bit in the next version, so you can see the last few quarters better:

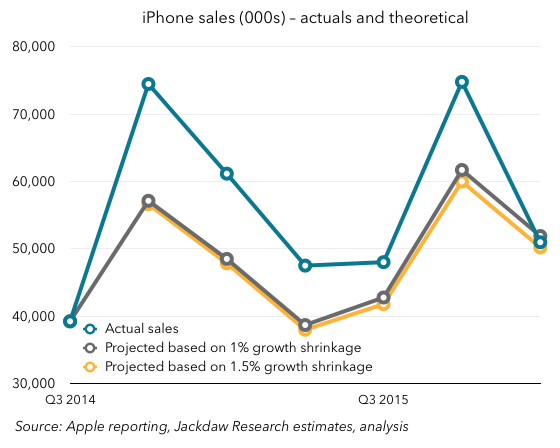

It’s a bit hard to tell exactly what’s going on in a chart with so much history, but I’ll zoom in a little bit in the next version, so you can see the last few quarters better: In this chart, you can hopefully see that that consensus point of 51 million falls right between the two projected data points for Q1 2016. In other words, it’s very much in keeping with the long-term trajectory in iPhone sales. The iPhone 6 blip is over, but if iPhone sales land roughly where the analysts expect them to, they’ll be right back on track with where they were headed before the iPhone 6 launched. That’s a big “if” – sales could come in above or below that number, which would suggest either that underlying growth had slowed more dramatically in the past, or that Apple has successfully pushed to a slightly higher long-term growth rate off the back of the iPhone 6 and 6S.

In this chart, you can hopefully see that that consensus point of 51 million falls right between the two projected data points for Q1 2016. In other words, it’s very much in keeping with the long-term trajectory in iPhone sales. The iPhone 6 blip is over, but if iPhone sales land roughly where the analysts expect them to, they’ll be right back on track with where they were headed before the iPhone 6 launched. That’s a big “if” – sales could come in above or below that number, which would suggest either that underlying growth had slowed more dramatically in the past, or that Apple has successfully pushed to a slightly higher long-term growth rate off the back of the iPhone 6 and 6S.

The other big question is what happens in the next few quarters, and whether Apple is able to stay on or above that long-term trend line. Remember that the trend line calls for a 1-1.5% reduction in year on year growth per quarter – on that basis, growth would slow to 6%, 5%, and 4% over the remaining quarters of 2016 with 1% shrinkage, or drop as low as a 1% decline by the end of the year. This is obviously far too precise for a real-world projection, but it gives you some sense of that trajectory if it does continue. It’ll be very interesting to see Apple’s guidance for the June quarter – on the basis of the trajectory, Apple would sell between 39 and 41 million iPhones next quarter. But of course, it’s just launched the iPhone SE, which could change things. Anything below 40 million iPhones (or $40 billion in revenue guidance) is a sign that Apple is dropping below its long-term trajectory, and would be bad news. Anything above that is cause for optimism, at least in the short term.

This, then, is the real answer to the question those reporters have been asking, in the form of another question: Does iPhone growth revert to its long-term trajectory, dip below it, or bounce back above it, in the reported numbers for Q1 and guidance for Q2? The answer to that question tells you what you need to know – at least in the short term – about how you should feel about iPhone sales.