I gather data on a quarterly basis on the major cable, satellite, and telecoms companies in the US and their reported numbers for pay TV subscribers (as well as broadband and voice subscribers). I package this up into a slide deck for subscribers to the Jackdaw Research Quarterly Decks Service, but it’s also available as a one-off standalone purchase. This post analyzes the data on pay TV subscriptions for Q1 2016.

Cord cutting continues to accelerate

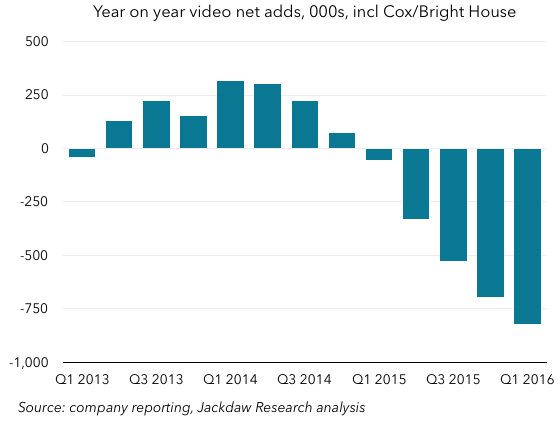

The headline here is that cord cutting continues to accelerate, a trend we’ve seen now for several quarters. As a reminder, in order to really gauge this trend, you can’t look at quarterly adds, because those are highly cyclical, and you have to look at the full set of players in the market, and not just largest, and certainly not just one type of player, such as cable or satellite companies. I’ll provide some more insight into this later in the post. On that basis, then, the chart below shows the year on year growth numbers for the industry, based on all the major public companies in the US and estimates for Cox and Bright House, two of the larger private companies.  As you can see, the year on year declines that began a year ago in the first quarter of 2015 have grown every quarter since, and are now at over 800k. There’s no doubt at all based on these numbers that cord cutting is happening, and that it’s accelerating. More people are canceling pay TV service from these players than are signing up for service, and the gap between those two numbers is growing every quarter. The rest of this piece talks through additional detail around this trend, in several areas:

As you can see, the year on year declines that began a year ago in the first quarter of 2015 have grown every quarter since, and are now at over 800k. There’s no doubt at all based on these numbers that cord cutting is happening, and that it’s accelerating. More people are canceling pay TV service from these players than are signing up for service, and the gap between those two numbers is growing every quarter. The rest of this piece talks through additional detail around this trend, in several areas:

- The additional impact on cable networks of the rise of skinny bundles and over-the-top services

- The resurgence of cable and the decline in telco TV

- The huge difference between trends facing larger and smaller pay TV providers.

Skinny bundles and OTT

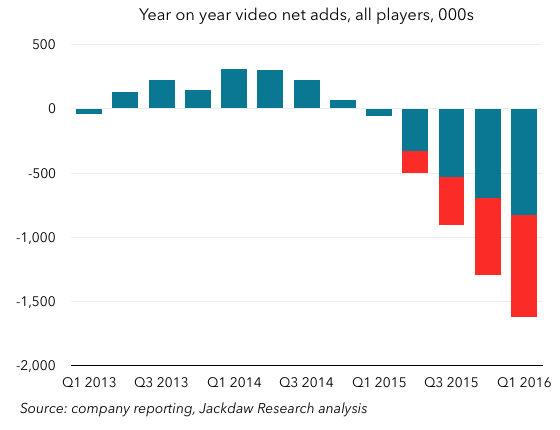

Of course, cord cutting isn’t the only behavior that’s affecting how many customers subscribe to these services. Two particularly additional trends are the move to “skinny bundles” and the rise of over-the-top alternatives to traditional pay TV. Skinny bundles are a trimmed-down version of pay TV services from traditional providers. Verizon has Custom TV, which is one of the more extreme forms of this trend, while many other pay TV companies have also been providing similar packages with fewer channels. On its quarterly earnings call, Verizon reported that 38% of its new FiOS TV customers in the first quarter signed up for Custom TV packages, which it characterized as lower-revenue but higher margin than its traditional offerings. On the OTT side, perhaps the biggest player is Sling, from DISH. The issue from a reporting perspective is that DISH reports Sling subscribers along with its traditional satellite TV subscribers in its overall totals, without breaking them out. As such, the numbers in the chart above include several hundred thousand Sling subscribers that are generating far less revenue monthly and taking far fewer channels than the traditional pay TV subscriber. If you strip those out of the reporting (as shown by the red bars), the numbers start to look even worse: As you can see, you’re now talking about an annual decline that’s about twice as big, at over 1.6 million rather than 800 thousand. Why is this important? Well, if you’re a cable network, you could be affected just as much by skinny bundles and these smaller OTT bundles as you are by outright cord cutting. This is evident in the numbers reported at least annually by the major cable networks, almost all of which have declined by 2-3 million subscribers year on year in recent quarters. The only exceptions have tended to be newer networks that are still growing from smaller bases, and some of the premium networks like HBO and to a lesser extent Starz.

As you can see, you’re now talking about an annual decline that’s about twice as big, at over 1.6 million rather than 800 thousand. Why is this important? Well, if you’re a cable network, you could be affected just as much by skinny bundles and these smaller OTT bundles as you are by outright cord cutting. This is evident in the numbers reported at least annually by the major cable networks, almost all of which have declined by 2-3 million subscribers year on year in recent quarters. The only exceptions have tended to be newer networks that are still growing from smaller bases, and some of the premium networks like HBO and to a lesser extent Starz.

A cable resurgence

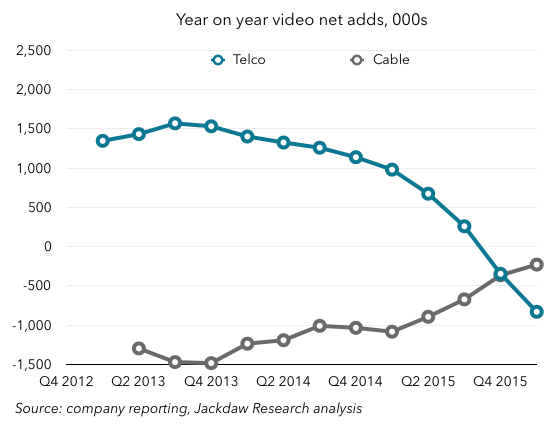

Another important trend we’ve seen over the last year or so is a dramatic change in the trajectories of two major groups of companies within the overall base of pay TV providers in the US. The cable companies have had a resurgence of sorts, while the telcos have faded dramatically in their ability to grow TV subscribers. The chart below compares year on year growth in subs for just these two groups: As you can see, the telcos regularly added over a million subs a year in 2012 and 2013, but since 2014 things have been heading rapidly downhill and have been increasingly negative for the last two quarters, while the cable companies have been returning closer to flat growth. Hence all those stories you’ve been seeing around earnings time for the last few quarters about the cable companies doing so well in TV sub growth, despite the overall cord cutting trend.

As you can see, the telcos regularly added over a million subs a year in 2012 and 2013, but since 2014 things have been heading rapidly downhill and have been increasingly negative for the last two quarters, while the cable companies have been returning closer to flat growth. Hence all those stories you’ve been seeing around earnings time for the last few quarters about the cable companies doing so well in TV sub growth, despite the overall cord cutting trend.

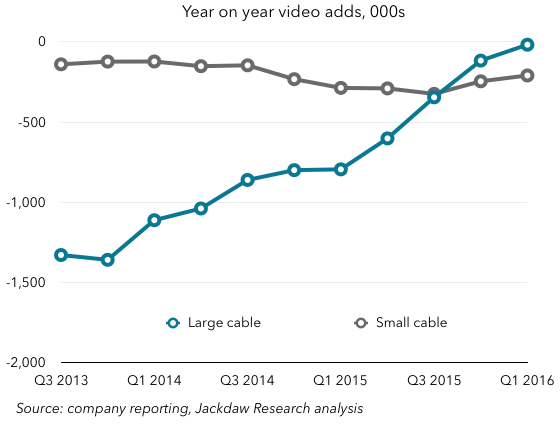

It’s really about large cable companies

In fact, it’s not even just about the cable companies versus the telcos, but about a division even among the cable companies. If you split cable company results by large and small companies, you see quite a disparity again: Here, you can see that the gains have been made almost entirely by the large cable companies, and that the small cable companies (which are even collectively much smaller) have been seeing worsening trends if anything. So it’s really that the large cable companies are making gains, while smaller cable companies and telcos are losing subscribers. The satellite providers are the last group here, and they’ve been seeing a more mixed bag of trends, with AT&T driving a resurgence at DirecTV thanks to bundling and heavy promotional activity, while DISH’s performance has been more mixed, especially if you strip out the Sling results.

Here, you can see that the gains have been made almost entirely by the large cable companies, and that the small cable companies (which are even collectively much smaller) have been seeing worsening trends if anything. So it’s really that the large cable companies are making gains, while smaller cable companies and telcos are losing subscribers. The satellite providers are the last group here, and they’ve been seeing a more mixed bag of trends, with AT&T driving a resurgence at DirecTV thanks to bundling and heavy promotional activity, while DISH’s performance has been more mixed, especially if you strip out the Sling results.

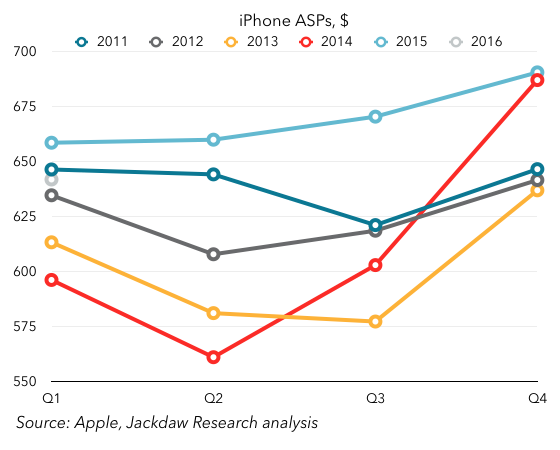

As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.

As you can see, at the end of 2014 ASPs dramatically increased as a result of larger, more expensive phones, and higher storage tiers. The 2015 ASPs were above 2014 ASPs for the entire year, but Q1 2016 saw ASPs dip, below the previous year’s number (and below even 2011, which was next highest for Q1). All of this suggests a combination of mix shift toward lower-tier and older iPhones, as well as possible discounting in some markets. Since ASPs have a direct impact on margins, that’s not good news. Worse still, Apple is projecting even lower ASPs in Q2 driven by a combination of inventory changes and sales of the iPhone SE.